India’s six major metropolitan rental markets - Bengaluru, Mumbai, Delhi-NCR, Hyderabad, Pune, and Chennai - each operate with distinct norms, legal frameworks, and market practices that have evolved from the interaction of local real estate economics, state-level legislation, and cultural conventions. For the millions of professionals who relocate between these cities each year - particularly in the technology sector - understanding these differences is essential for budgeting, negotiation, and avoiding expensive surprises.

This comparative analysis examines each metro’s rental market across six dimensions: rent levels, deposit norms, agreement practices, legal frameworks, brokerage conventions, and unique market characteristics. The goal is to provide a reference framework for anyone navigating inter-city relocation or evaluating rental market dynamics across India.

Rent Levels: A Controlled Comparison

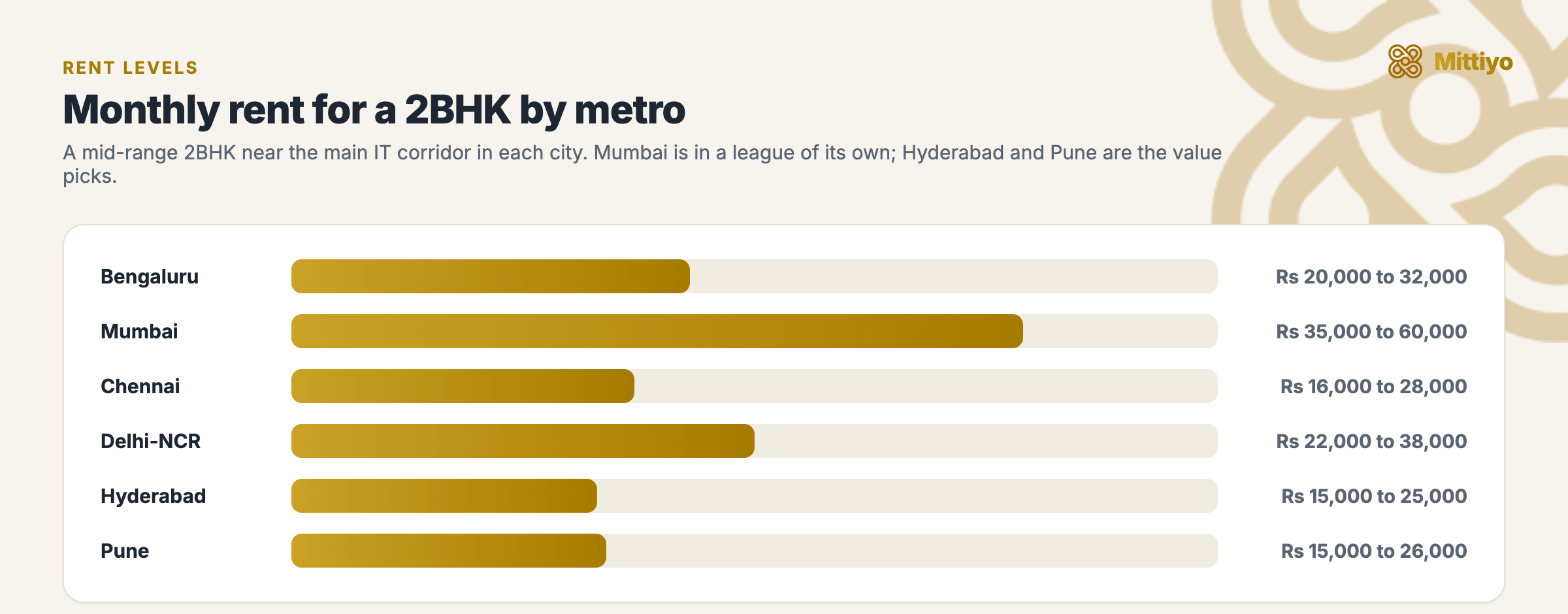

Comparing rents across cities requires controlling for property type, locality quality, and proximity to employment hubs. The following comparison uses a standard 2BHK (900-1,200 sq ft) in a mid-range apartment complex near each city’s primary IT employment corridor - the most common rental profile for technology professionals.

| City | Primary IT Corridor | Benchmark Localities | Monthly Rent Range (2BHK) | Rent per Sq Ft |

|---|---|---|---|---|

| Bengaluru | Outer Ring Road, Whitefield, Electronic City | Whitefield, Marathahalli, HSR Layout | Rs 20,000-32,000 | Rs 18-30 |

| Mumbai | BKC, Andheri-Powai corridor, Navi Mumbai | Andheri, Powai, Thane | Rs 35,000-60,000 | Rs 40-65 |

| Delhi-NCR | Gurugram Cyber City, Noida Expressway | Gurugram Sec 48-56, Noida Sec 62-135 | Rs 22,000-38,000 | Rs 20-35 |

| Hyderabad | HITEC City, Gachibowli-Nanakramguda | Gachibowli, Kondapur, Madhapur | Rs 15,000-25,000 | Rs 14-24 |

| Pune | Hinjewadi IT Park, Kharadi, Magarpatta | Hinjewadi, Wakad, Baner | Rs 15,000-26,000 | Rs 15-25 |

| Chennai | OMR (IT Expressway), Sholinganallur | OMR, Thoraipakkam, Perungudi | Rs 16,000-28,000 | Rs 15-27 |

Monthly rent for a comparable 2BHK near each city’s IT corridor.

Monthly rent for a comparable 2BHK near each city’s IT corridor.

Interpreting the Rent Data

Mumbai is structurally more expensive. Mumbai rents are 50-80% higher than the next most expensive metro (Delhi-NCR) for comparable properties. This reflects Mumbai’s fundamental constraint - the city is a narrow peninsula with severe land scarcity, and horizontal expansion is limited by geography (sea on three sides, salt marshes, and protected mangroves). Every other metro can expand outward; Mumbai cannot.

Hyderabad and Pune offer the best value. Both cities have abundant developable land around their IT corridors, resulting in newer construction at lower prices. For a technology professional earning a comparable salary across cities, Hyderabad and Pune offer the most favorable rent-to-income ratio.

Bengaluru occupies the middle ground on rent but an outlier on total cost. Monthly rents in Bengaluru are moderate - comparable to Delhi-NCR and 30-40% below Mumbai. However, when the 10-month deposit is factored in, the total upfront cost of renting in Bengaluru is the highest of any Indian metro.

Chennai is underpriced relative to its IT market size. Chennai has India’s second-largest IT workforce but rents remain lower than Bengaluru and Delhi-NCR. This reflects a combination of more affordable real estate, lower speculative premium, and a cultural preference for owned versus rented housing that moderates rental demand pressure.

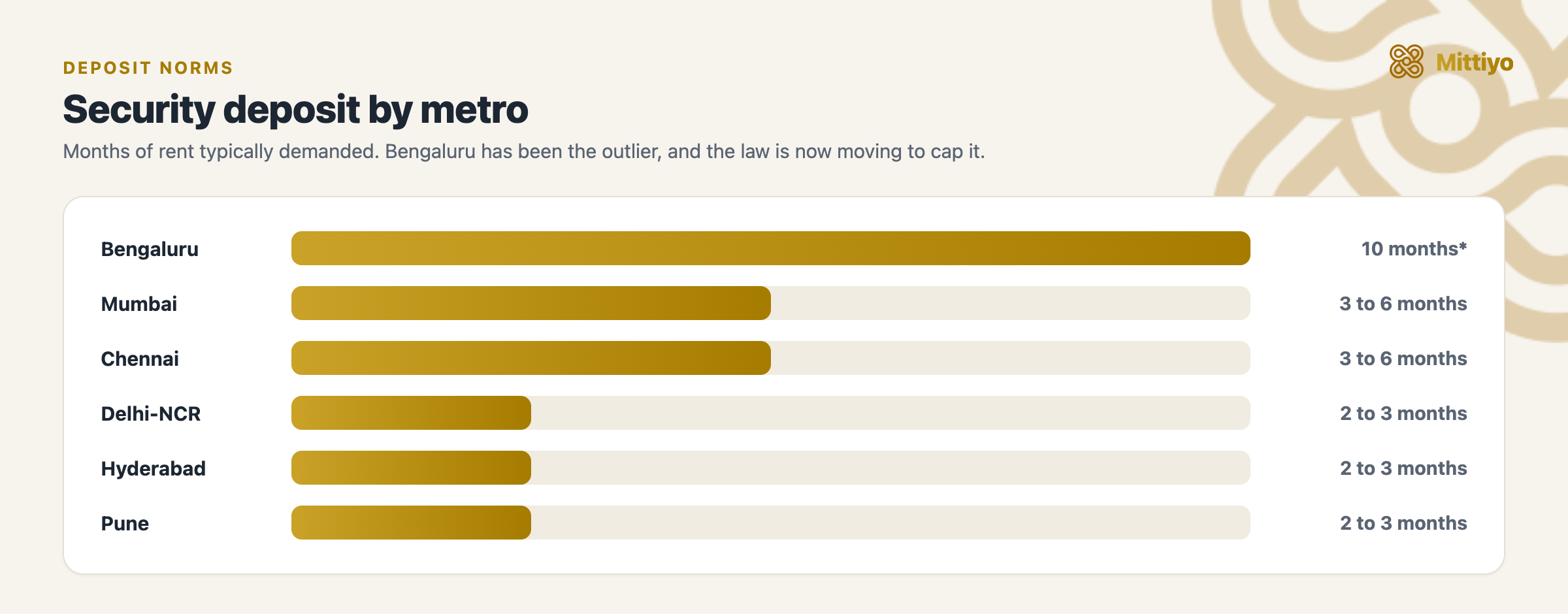

Deposit Norms: The Hidden Cost of Relocation

The security deposit - the lump sum paid upfront and refundable at tenancy end - varies dramatically across Indian metros and is often the largest financial consideration for inter-city relocation.

Security deposit norms across the major metros.

Security deposit norms across the major metros.

| City | Standard Deposit | Amount for Rs 25,000/month Apartment | Statutory Cap | Return Practice |

|---|---|---|---|---|

| Bengaluru | 10 months (historical) | Rs 2,50,000 | 2-month cap (2025 Act)* | 1-2 months after exit; deductions common |

| Mumbai | 3-6 months | Rs 75,000-1,50,000 | No statutory cap (MTA recommends 2 months) | 1-3 months; generally smoother |

| Delhi-NCR | 2-3 months | Rs 50,000-75,000 | No statutory cap | 1-2 months; negotiable |

| Hyderabad | 2-3 months | Rs 50,000-75,000 | No statutory cap | 1-2 months |

| Pune | 2-3 months | Rs 50,000-75,000 | No statutory cap | 1-2 months |

| Chennai | 3-6 months | Rs 75,000-1,50,000 | No statutory cap | 1-2 months; advance rent also common |

*The Karnataka Rent (Amendment) Act, 2025 (in force January 2026) is reported to cap residential deposits at two months and to require digital registration of agreements on the Kaveri 2.0 portal. How firmly this binds the standard 11-month leave-and-license agreement, and whether such agreements must now be registered, is still being worked out; in practice, 10-month demands have remained common.

Why Bengaluru’s Deposit Has Been So High

Bengaluru’s 10-month deposit norm grew up as a market convention rather than a legal rule, and that is exactly what the law is now trying to change. The Karnataka Rent (Amendment) Act, 2025, in force since January 2026, moves to cap residential security deposits (reported at two months’ rent), echoing the Model Tenancy Act, 2021’s long-standing recommendation. What remains genuinely unsettled is how the cap applies to the standard 11-month leave-and-license agreement that dominates Bengaluru, and whether those agreements must now be registered. Until that settles in practice, the 10-month convention is best treated as on its way out rather than as either a fixed rule or a freshly enforced ban.

Several factors explain the persistence of the 10-month norm:

1. Market equilibrium driven by demand. Bengaluru’s IT boom created massive rental demand from a mobile, well-paid workforce that could afford high deposits. Landlords found that high deposits attracted stable tenants who were less likely to default or vacate abruptly.

2. Landlord capital utilization. In practice, many landlords treat the deposit as an interest-free loan - investing it in fixed deposits, business, or further real estate. A Rs 3 lakh deposit earning 7% in a fixed deposit generates Rs 21,000 per year for the landlord - effectively a hidden discount on rent.

3. Insurance against damage and default. With 10 months’ rent as deposit, landlords have substantial protection against unpaid rent (a tenant defaulting on 2-3 months’ rent is still covered) and property damage. In cities with lower deposits, landlords bear more risk and may compensate through higher rent or stricter tenant screening.

4. Self-reinforcing convention. Market norms are sticky. Because landlords expect 10 months and tenants (especially those familiar with Bengaluru) accept it, the convention perpetuates. New entrants from other cities experience deposit shock but have limited negotiating power in a demand-heavy market.

Interest on Security Deposit

A frequently debated question is whether landlords should pay interest on security deposits. The legal position in Karnataka:

- There is no statutory requirement under the Karnataka Rent Act 1999 (as amended) for landlords to pay interest on security deposits.

- The Model Tenancy Act 2021 (advisory, not adopted) recommends interest-free deposits.

- Some state laws in other jurisdictions (e.g., certain consumer protection interpretations) have considered whether deposits should earn interest, but no binding precedent exists in Karnataka.

- Tenants can contractually negotiate interest on deposits, but this is rare in practice.

The economic reality is that a Rs 3 lakh deposit at zero interest for 11-24 months represents a significant opportunity cost for the tenant (Rs 15,000-45,000 in foregone interest) and a corresponding benefit to the landlord.

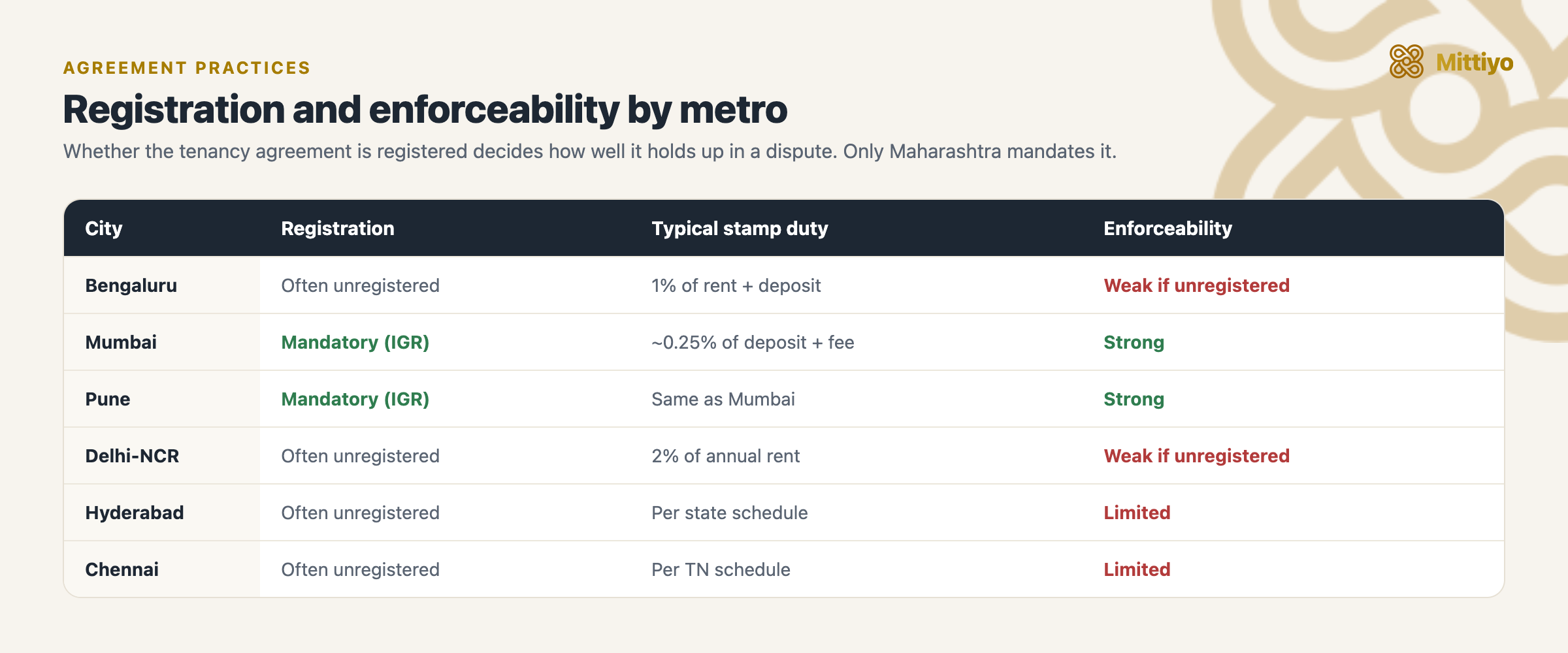

Agreement Practices: Registration, Documentation, and Enforcement

Rental agreement practices - the formality, registration, and enforceability of the tenancy document - vary significantly across metros, with major implications for dispute resolution and legal protection.

| City | Agreement Type | Typical Duration | Registration | Stamp Duty | Enforceability |

|---|---|---|---|---|---|

| Bengaluru | Leave and License / Rental Agreement | 11 months | Often unregistered (many are only notarized) | 1% of total rent + deposit for the period (Karnataka Stamp Act, as amended 2025) | Unregistered agreements are inadmissible as evidence in court under Section 49 of the Registration Act |

| Mumbai | Leave and License | 11 months | Mandatory (IGR Maharashtra online portal) | 0.25% of deposit + license fee for the period | Registered; strong enforceability; digital records |

| Delhi-NCR | Rent Agreement | 11 months | Often unregistered (notarized) | 2% of annual rent (if registered) | Similar enforcement challenges as Bengaluru for unregistered agreements |

| Hyderabad | Rent Agreement | 11 months | Often unregistered | Varies by stamp duty schedule | Limited enforceability for unregistered agreements |

| Pune | Leave and License | 11 months | Mandatory (IGR Maharashtra online portal) | Same as Mumbai | Same as Mumbai - strong enforceability |

| Chennai | Rent Agreement | 11 months | Often unregistered | Based on Tamil Nadu stamp duty schedule | Limited enforceability for unregistered agreements |

Registration drives enforceability; only Maharashtra makes it mandatory.

Registration drives enforceability; only Maharashtra makes it mandatory.

Maharashtra’s Mandatory Registration: A Model Practice

Maharashtra (governing both Mumbai and Pune) requires mandatory online registration of all leave and license agreements, regardless of duration. This is enforced through the IGR Maharashtra portal and has several advantages:

1. Evidentiary value. A registered agreement is admissible in court as primary evidence. Unregistered agreements (common in Bengaluru, Delhi, Hyderabad, Chennai) are inadmissible under Section 49 of the Registration Act 1908, severely weakening any party’s legal position in a dispute.

2. Government record. Registration creates an official record with the Sub-Registrar’s office, preventing disputes about the agreement’s existence, terms, or execution date.

3. Police verification. Maharashtra links agreement registration with police verification of the tenant - a valuable safety measure that also creates an official address record.

4. Standardized process. The online portal provides a template, calculates stamp duty automatically, and generates a digitally signed document - reducing the role of intermediaries and minimizing errors.

5. Low cost. Total registration cost in Maharashtra is typically Rs 1,000-3,000 for a standard rental agreement - a negligible amount relative to the legal protection it provides.

The Bengaluru Registration Problem

Most 11-month agreements in Bengaluru are unregistered - some are merely notarized (which provides no legal standing) or executed on plain paper. This creates a significant gap in legal protection:

- If a deposit dispute arises: An unregistered agreement cannot be produced as evidence in court under Section 49 of the Registration Act 1908. The tenant has no documentary proof of the deposit amount, the agreed rent, or the terms of the tenancy.

- If illegal eviction occurs: Without a registered agreement, proving the tenancy existed and its terms becomes a challenge.

- Tax implications: Unregistered agreements may not be accepted by income tax authorities for claiming HRA exemptions.

Under the Registration Act 1908, Section 17, any lease for a term exceeding one year must be compulsorily registered. The 11-month convention exists precisely to avoid this requirement. However, even for 11-month agreements, voluntary registration is advisable - and the Karnataka Stamp (Amendment) Act 2025 prescribes stamp duty on rental agreements.

Cost of registration in Karnataka: Stamp duty (1% of total consideration - rent + deposit for the agreement period) plus registration fee. For a typical Bengaluru rental (Rs 25,000/month, Rs 2,50,000 deposit), the total registration cost is approximately Rs 5,000-8,000.

Legal Frameworks: Rent Control and Tenant Protection

Each metro operates under a different state-level rent control law, creating significant variations in landlord and tenant rights.

Bengaluru: Karnataka Rent Act, 1999 (Amended 2025)

The Karnataka Rent (Amendment) Act 2025 updated the 1999 Act to address contemporary rental market realities.

Key provisions:

- Fair rent determination - The Rent Controller can determine fair rent based on property specifications, locality, amenities, and comparable market rates. Either landlord or tenant can apply for fair rent determination.

- Eviction grounds - Specified grounds include non-payment of rent, subletting without consent, causing nuisance, and landlord’s bona fide personal need. The landlord must prove the ground before the Rent Controller.

- Essential services protection - Landlords are prohibited from disconnecting water, electricity, or other essential services to force eviction. Violation is a punishable offense.

- Tenant’s right to receipt - Landlord must provide a rent receipt. If the landlord refuses to accept rent, the tenant can deposit it with the Rent Controller.

- No cap on market rent - For new tenancies, the Act does not cap the rent. Parties are free to agree on any amount. The fair rent mechanism operates as a dispute resolution tool, not a price control.

Mumbai and Pune: Maharashtra Rent Control Act, 1999

Key provisions:

- Dual regime - Premises constructed before 1.1.2000 are governed by the old (stringent) rent control provisions with capped rents. Post-1.1.2000 constructions have more balanced provisions.

- Old rent control - For pre-2000 buildings, standard rent is fixed and increases are strictly limited. This has created extreme rent disparity - tenants in old South Mumbai buildings pay Rs 500-2,000/month for apartments that would rent for Rs 50,000-1,00,000+ at market rates.

- Leave and license regime - For post-2000 constructions, the leave and license system (11-month agreements, renewable) operates with market-determined rents.

- Mandatory registration - All agreements must be registered online.

Delhi: Delhi Rent Control Act, 1958

Key provisions:

- Applies only to pre-1988 constructions - Properties built before 1.6.1988 with rent below Rs 3,500/month fall under rent control. This is an extremely narrow scope - most modern rentals in Delhi-NCR are outside rent control.

- NCR (Gurugram, Noida) - Different states, different laws. Gurugram (Haryana) has the Haryana Urban (Control of Rent and Eviction) Act, 1973. Noida (Uttar Pradesh) has the UP Urban Buildings (Regulation of Letting, Rent and Eviction) Act, 1972.

- Fragmented jurisdiction - This makes Delhi-NCR the most legally complex metro for rental matters, as the applicable law depends on whether the property is in Delhi, Gurugram, Noida, Faridabad, or Ghaziabad.

Hyderabad: Telangana Buildings (Lease, Rent and Eviction) Control Act

Key provisions:

- Fair rent fixation by Rent Controller

- Eviction protections - landlord must prove specified grounds

- No mandatory agreement registration

- Relatively balanced framework but enforcement is slow

Chennai: Tamil Nadu Buildings (Lease and Rent Control) Act, 1960

Key provisions:

- Fair rent determination by Rent Controller

- Strong tenant protections - eviction restricted to specified grounds

- Advance rent practice (6-12 months’ rent as advance, adjusted against monthly rent) is unique to Tamil Nadu

- No mandatory registration for 11-month agreements

Brokerage and Transaction Costs

| City | Standard Brokerage | Who Pays | How It’s Calculated | Market Practice |

|---|---|---|---|---|

| Bengaluru | 1 month’s rent | Tenant | One month’s rent for the broker; some charge 15 days each from landlord and tenant | Standardized; most transactions through brokers |

| Mumbai | 1 month’s rent | Split or tenant | 15 days’ rent from each party, or 1 month from tenant | More standardized; online platforms gaining share |

| Delhi-NCR | 1 month’s rent | Tenant | Full month from tenant; in Gurugram, some charge 15 days each | Aggressive negotiation culture; broker fees negotiable |

| Hyderabad | 1 month’s rent | Tenant | Typically 1 month from tenant | Less organized; many informal transactions |

| Pune | 1 month’s rent | Split | 15 days from each party (Maharashtra norm) | Standardized; same as Mumbai |

| Chennai | 15 days-1 month | Tenant | Lower brokerage than other metros; often 15 days | Some direct deals; broker network less dominant |

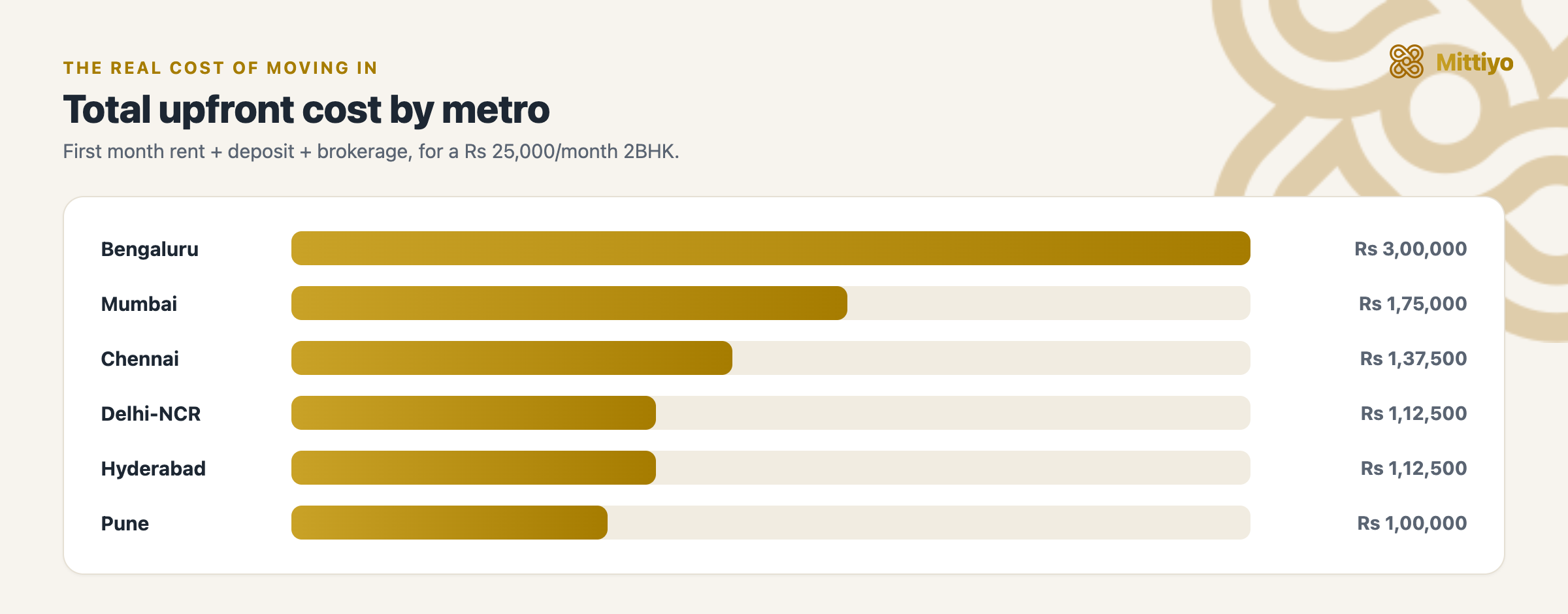

Total Upfront Cost Comparison

For a technology professional renting a 2BHK at Rs 25,000/month, the total upfront cost (first month rent + deposit + brokerage) across metros:

What it actually costs to move in, by city.

What it actually costs to move in, by city.

| City | First Month | Deposit | Brokerage | Total Upfront |

|---|---|---|---|---|

| Bengaluru | Rs 25,000 | Rs 2,50,000 (10 months) | Rs 25,000 | Rs 3,00,000 |

| Mumbai | Rs 25,000 | Rs 1,25,000 (5 months) | Rs 25,000 | Rs 1,75,000 |

| Delhi-NCR | Rs 25,000 | Rs 62,500 (2.5 months) | Rs 25,000 | Rs 1,12,500 |

| Hyderabad | Rs 25,000 | Rs 62,500 (2.5 months) | Rs 25,000 | Rs 1,12,500 |

| Pune | Rs 25,000 | Rs 62,500 (2.5 months) | Rs 12,500 | Rs 1,00,000 |

| Chennai | Rs 25,000 | Rs 1,00,000 (4 months) | Rs 12,500 | Rs 1,37,500 |

Bengaluru’s total upfront cost is 1.7x Mumbai’s and 3x Pune’s for the same monthly rent - entirely driven by the deposit differential. This is the single most important financial consideration for anyone relocating to Bengaluru.

Unique Market Characteristics by City

Bengaluru

Market driver: IT industry hiring and compensation cycles. Bengaluru has India’s largest concentration of technology companies, and rental demand tracks tech industry health closely. Hiring booms tighten the market; layoff cycles (as seen in 2023) soften it.

Water supply as a differentiator. Bengaluru’s water infrastructure is divided between Cauvery water supply (BWSSB pipeline, available in inner and some middle-ring areas) and borewell/tanker dependency (common in peripheral areas). Cauvery-connected properties command measurable rent premiums (5-10%) and experience lower vacancy. Water availability should be a primary due diligence item for any Bengaluru renter.

Metro impact. The Namma Metro (Purple and Green lines) is transforming rental dynamics along its corridors. Properties within walking distance of metro stations command premium rents, and the upcoming Yellow and Pink lines will extend this effect. Unlike Delhi or Mumbai, Bengaluru’s metro network is still developing, so connectivity premiums are concentrated rather than city-wide.

PG and co-living market. Bengaluru has India’s most mature paying guest (PG) and co-living market, driven by single IT professionals (22-30 age group) who want furnished accommodation near workplaces. Monthly costs range from Rs 8,000-20,000 including food, utilities, and housekeeping. This segment competes with the traditional 1BHK/2BHK rental market for younger professionals.

Mumbai

Space premium. Mumbai apartments are typically 20-30% smaller than equivalents in other cities for the same price point. A “2BHK” in Mumbai might be 550-700 sq ft carpet area, while a Bengaluru “2BHK” is typically 800-1,100 sq ft. Comparing rent per square foot is more meaningful than comparing headline rent.

Old rent control disparity. The Maharashtra Rent Control Act creates a two-tier market. Pre-1999 buildings in areas like South Mumbai, Dadar, and Girgaon have controlled tenants paying a fraction of market rent, while neighboring buildings lease at full market rates. This disparity distorts the market and creates complex tenancy dynamics.

Local train connectivity. Mumbai’s rental geography is organized around the Western, Central, and Harbour railway lines. Properties near railway stations command consistent demand. The metro network is expanding but the local train remains the primary transit backbone.

Redevelopment dynamics. Many old buildings in Mumbai are undergoing redevelopment (demolition and reconstruction under the Development Control Regulations). Existing tenants receive temporary alternative accommodation or hardship compensation, and returning tenants get modern apartments. This creates a unique rental sub-market of temporarily displaced tenants.

Delhi-NCR

Fragmented market across state lines. Delhi-NCR spans three states (Delhi, Haryana, Uttar Pradesh) with different rental laws, property tax regimes, stamp duty rates, and police verification requirements. Gurugram (Haryana) and Noida (UP) have very different market dynamics and legal frameworks from central Delhi.

Negotiation culture. Delhi-NCR has the most aggressive negotiation culture among Indian metros. Asking rent is a starting point, not a final price. Tenants routinely negotiate 10-20% discounts, whereas in Bengaluru and Mumbai, negotiation margins are typically 5-10%.

Furnishing variance. The degree of furnishing in Delhi-NCR rentals varies widely. Many apartments are offered completely unfurnished (no kitchen platform, no bathroom fittings, no wardrobes) - requiring the tenant to invest in basic fittings. In Bengaluru and Mumbai, semi-furnished (wardrobes, kitchen platform, bathroom fittings) is the baseline.

Power backup as essential infrastructure. Unlike Bengaluru (which has relatively stable power supply), Delhi-NCR experiences frequent power outages, especially in summer months. DG set backup and inverter availability are critical factors in rental decisions - and DG charges add Rs 2,000-5,000/month to the effective cost.

Hyderabad

Affordability leader. Hyderabad offers the lowest rents among major IT hubs, combined with low deposits (2-3 months). The HITEC City / Gachibowli corridor has modern infrastructure, new construction, and a growing IT ecosystem - at 20-40% lower cost than comparable Bengaluru localities.

Rapid infrastructure development. Hyderabad’s infrastructure (roads, metro, pharma/IT corridors) is developing rapidly, creating both opportunities (appreciating property values, improving connectivity) and risks (construction disruption, unproven localities) for renters.

Less organized market. Compared to Bengaluru and Mumbai, Hyderabad’s rental market is less organized. Online listing platforms have lower penetration, broker networks are more informal, and standardized agreement practices are less common. This can make apartment hunting more time-consuming but also creates space for better negotiation outcomes.

GHMC governance. The Greater Hyderabad Municipal Corporation (GHMC) covers a large area with relatively uniform governance. Property tax rates, building regulations, and civic infrastructure are more consistent across Hyderabad’s rental zones than across Bengaluru (where BBMP, BDA, and village panchayat jurisdictions create variance).

Pune

Maharashtra framework with smaller-city dynamics. Pune benefits from Maharashtra’s strong legal infrastructure (mandatory registration, standardized agreements) while maintaining the lower rents of a smaller city. For IT professionals, Pune’s Hinjewadi-Wakad-Baner corridor offers modern apartments at 25-40% below comparable Bengaluru rates.

Student and IT mix. Pune has a large student population (University of Pune, Symbiosis, and numerous engineering colleges) that creates a secondary rental market distinct from the IT professional segment. Student areas (Kothrud, Shivajinagar, FC Road) have different dynamics from IT corridors (Hinjewadi, Kharadi, Magarpatta).

Proximity to Mumbai. Pune’s rental market is increasingly influenced by Mumbai professionals working remotely or in hybrid arrangements. The Mumbai-Pune corridor (expressway and upcoming hyperloop/metro link) makes Pune a viable residential base for Mumbai professionals, adding to rental demand.

Chennai

Advance rent practice. Unique to Tamil Nadu, some landlords in Chennai charge 6-12 months’ rent as an advance, which is adjusted against monthly rent. For example, a landlord might charge Rs 1,80,000 as advance (12 months x Rs 15,000) and adjust Rs 15,000/month, with the tenant paying only the differential if rent is higher. This is distinct from a security deposit - it is prepaid rent. This practice reduces the landlord’s risk and the tenant’s monthly cash outflow but increases the upfront capital requirement.

Conservative market. Chennai’s rental market is more conservative and relationship-driven than other metros. Landlords tend to be more selective about tenants (food preferences, family status, cultural background are sometimes factors), and long-term tenancies are more common. The market has lower volatility - rents do not spike as sharply during hiring booms or fall as steeply during downturns.

OMR corridor development. The Old Mahabalipuram Road (OMR) / IT Expressway is Chennai’s equivalent of Bengaluru’s Outer Ring Road - a concentrated IT employment corridor with high rental demand. Infrastructure development along OMR (metro extension, road widening, commercial development) is creating new micro-markets with appreciating rental values.

Relocation Guide: Key Differences When Moving Between Cities

Moving TO Bengaluru

| From | Financial Impact | Practical Considerations |

|---|---|---|

| Mumbai | Rent decreases 20-40%, but deposit increases dramatically (3-6 months to 10 months). Net upfront cost may increase despite lower rent. | No mandatory registration (register voluntarily for protection). Water supply varies significantly by locality - verify Cauvery connection. |

| Delhi-NCR | Rent similar or slightly higher, but deposit increases from 2-3 to 10 months. Significant upfront capital needed. | Less negotiation room on rent and deposit. Furnishing level generally better (semi-furnished baseline). |

| Hyderabad | Rent increases 25-40%, deposit increases from 2-3 to 10 months. Substantial cost escalation. | More organized market (better online listings). Metro coverage expanding but not as comprehensive as Hyderabad metro. |

| Pune | Rent increases 15-30%, deposit increases from 2-3 to 10 months. Lose mandatory registration benefit. | Similar IT corridor dynamics. Co-living market much more mature in Bengaluru. |

| Chennai | Rent similar or slightly higher, deposit increases from 3-6 to 10 months. Lose advance rent adjustment practice. | Different cultural context. Food landscape is different. Weather is comparable (both South Indian, but Bengaluru is cooler). |

Moving FROM Bengaluru

| To | Financial Impact | Practical Considerations |

|---|---|---|

| Mumbai | Rent increases 40-80%, but deposit drops to 3-6 months. You recover most of your Bengaluru deposit. Apartments are 20-30% smaller. | Mandatory registration provides stronger legal protection. Local train commute is the norm - factor travel time into location choice. |

| Delhi-NCR | Rent similar, deposit drops to 2-3 months (recover Rs 1.5-2 lakh from Bengaluru deposit). | Negotiate harder - 10-20% discounts are normal. Check furnishing level carefully. Power backup (DG/inverter) is essential. |

| Hyderabad | Rent decreases 20-35%, deposit drops to 2-3 months. Significant monthly and upfront savings. | Less organized market - more legwork in apartment search. Growing IT infrastructure but less mature social infrastructure. |

| Pune | Rent decreases 15-25%, deposit drops to 2-3 months. Mandatory registration provides legal protection. | Maharashtra legal framework provides stronger tenant protections. Smaller city with less diverse amenity landscape. |

| Chennai | Rent similar or slightly lower, deposit drops to 3-6 months. Advance rent practice may apply. | More conservative landlord expectations. Food and cultural preferences may be factor in landlord selection. |

The Model Tenancy Act 2021: Potential Harmonization

The Model Tenancy Act (MTA) 2021 is a central government advisory framework designed to standardize rental practices across India. Key recommendations:

- Deposit cap of 2 months’ rent for residential properties

- Mandatory written agreement with registration

- Rent Authority for dispute resolution (separate from courts)

- Balanced eviction provisions - grounds specified, timeline mandated

- Subletting norms - allowed with written consent

Most states have not adopted the MTA wholesale, but several have moved in its direction through their own laws. Karnataka is a notable example: the Karnataka Rent (Amendment) Act, 2025 (in force January 2026) introduces a residential deposit cap (reported at two months) and a digital registration requirement, rather than waiting on the central model. If that two-month cap holds and is enforced for ordinary tenancies, it would sharply cut the upfront cost of renting in Bengaluru, from ten months toward two. The open questions are practical: how it applies to the standard 11-month leave-and-license agreement, whether such agreements must now be registered, and whether a demand-heavy market produces workarounds such as higher headline rent, non-refundable charges, or simple non-compliance.

The MTA represents a potential future harmonization of rental practices across India; in the meantime, state-specific frameworks (now including Karnataka’s 2025 amendment) continue to govern, and their on-the-ground application is still settling.

Dispute Resolution Across Metros

When rental disputes arise, the available mechanisms differ by city:

| City | Primary Forum | ADR Availability | Typical Resolution Time |

|---|---|---|---|

| Bengaluru | Rent Controller (Karnataka Rent Act); Civil Court | Mediation (Mediation Act 2023, Section 27 - enforceable settlements); Lok Adalat | Rent Controller: 6-18 months; Civil Court: 1-5 years; Mediation: 2-8 weeks |

| Mumbai | Small Causes Court (rent matters); Civil Court | Court-annexed mediation; Lok Adalat | Small Causes Court: 6-18 months; mediation: 2-8 weeks |

| Delhi-NCR | Rent Controller (Delhi); relevant state forum (Haryana/UP) | Mediation; Lok Adalat | Varies widely by jurisdiction |

| Hyderabad | Rent Controller; Civil Court | Mediation; Lok Adalat | Rent Controller: 6-18 months |

| Pune | Same as Mumbai (Maharashtra framework) | Same as Mumbai | Same as Mumbai |

| Chennai | Rent Controller (TN Rent Control Act); Civil Court | Mediation; Lok Adalat | Generally slow (1-3 years for court) |

The Mediation Act 2023 (Section 27) applies uniformly across India, making mediated settlement agreements enforceable as court decrees regardless of the city. This is particularly valuable for inter-city disputes - for example, a tenant who has moved from Bengaluru to Hyderabad but has a pending deposit refund dispute with a Bengaluru landlord can pursue mediation without being physically present in Bengaluru for repeated court hearings.

Moving to Bengaluru from another city?

The numbers vary building to building, not just city to city. Before you commit from afar, see what residents actually say about a specific Bengaluru building on know.place: the rent, the deposit, the water and power reality, and the society.

Explore know.placeKey Takeaways

- Bengaluru’s 10-month deposit norm has been the single largest financial differentiator across Indian metro rental markets, making the city’s total upfront rental cost roughly 1.7x Mumbai’s and 3x Pune’s despite moderate monthly rents; the Karnataka Rent (Amendment) Act, 2025 moves to cap residential deposits at two months, though its application to the standard 11-month leave-and-license agreement is still settling

- Mumbai is 40-80% more expensive in monthly rent but has lower deposits (3-6 months) and mandatory online agreement registration - a legally stronger framework for tenants

- Hyderabad offers the best overall value among IT hubs: lowest rents (20-35% below Bengaluru) combined with low deposits (2-3 months) and growing infrastructure

- Delhi-NCR has comparable rents to Bengaluru but much lower deposits (2-3 months); however, the fragmented legal framework across Delhi, Haryana, and UP creates complexity

- Maharashtra’s mandatory online registration of leave and license agreements (applicable to Mumbai and Pune) is a model practice that provides strong evidentiary protection and should be replicated in other states

- Chennai’s advance rent practice and conservative market dynamics create a distinct rental experience; the OMR IT corridor is the primary rental zone for technology professionals

- When comparing cities, look beyond monthly rent: factor in deposit, brokerage, registration costs, furnishing level, power/water reliability, and the legal enforceability of the agreement

- The Model Tenancy Act 2021 (recommending a 2-month deposit cap and mandatory registration) remains unadopted wholesale, but states are moving in its direction through their own laws; Karnataka’s 2025 amendment is one example, with its practical effect on ordinary 11-month agreements still being worked out

- The Mediation Act 2023 (Section 27) provides a uniform ADR mechanism across India - mediated settlements are enforceable as court decrees, useful for cross-city disputes

- For any inter-city move, verify: deposit norm, agreement registration requirement, applicable rent law, water and power reliability, furnishing baseline, and brokerage convention - these vary more than rent itself

This guide is part of the Bengaluru Renter’s Handbook, our complete set of guides for moving in and settling down.

References

- Karnataka Rent Act, 1999, as amended by the Karnataka Rent (Amendment) Act, 2025 - fair rent, eviction, deposit, registration

- Maharashtra Rent Control Act, 1999 - dual regime for pre- and post-2000 premises; mandatory registration

- Delhi Rent Control Act, 1958 - applicable to pre-1988 constructions; rent-ceiling provisions

- Telangana Buildings (Lease, Rent and Eviction) Control Act, 1960 - fair rent fixation, eviction protections

- Tamil Nadu Buildings (Lease and Rent Control) Act, 1960 - fair rent, advance-rent practice, tenant protections

- Haryana Urban (Control of Rent and Eviction) Act, 1973 - applicable to Gurugram rentals

- Registration Act, 1908 - Section 17 (compulsory registration), Section 49 (inadmissibility of unregistered documents)

- Karnataka Stamp Act, 1957, as updated by the Karnataka Stamp (Amendment) Act, 2025 (digital e-stamping) - stamp duty on rental and property agreements

- Model Tenancy Act, 2021 - central advisory framework recommending a 2-month deposit cap and mandatory registration

- Mediation Act, 2023 - Section 27 (enforceability of mediated settlement agreements as court decrees across India)

- Real Estate (Regulation and Development) Act, 2016 (RERA) - disclosure obligations

- IGR Maharashtra - online leave-and-license registration portal