Goods and Services Tax on residential rent is among the most frequently misunderstood areas of Indian indirect tax law. The rules underwent a significant change in July 2022, and confusion persists among landlords, tenants, and even tax professionals about when GST applies, who bears the liability, and what compliance obligations arise. This guide provides a thorough analysis of the current legal position, the historical context, and the practical implications for every category of landlord and tenant.

The quick answer

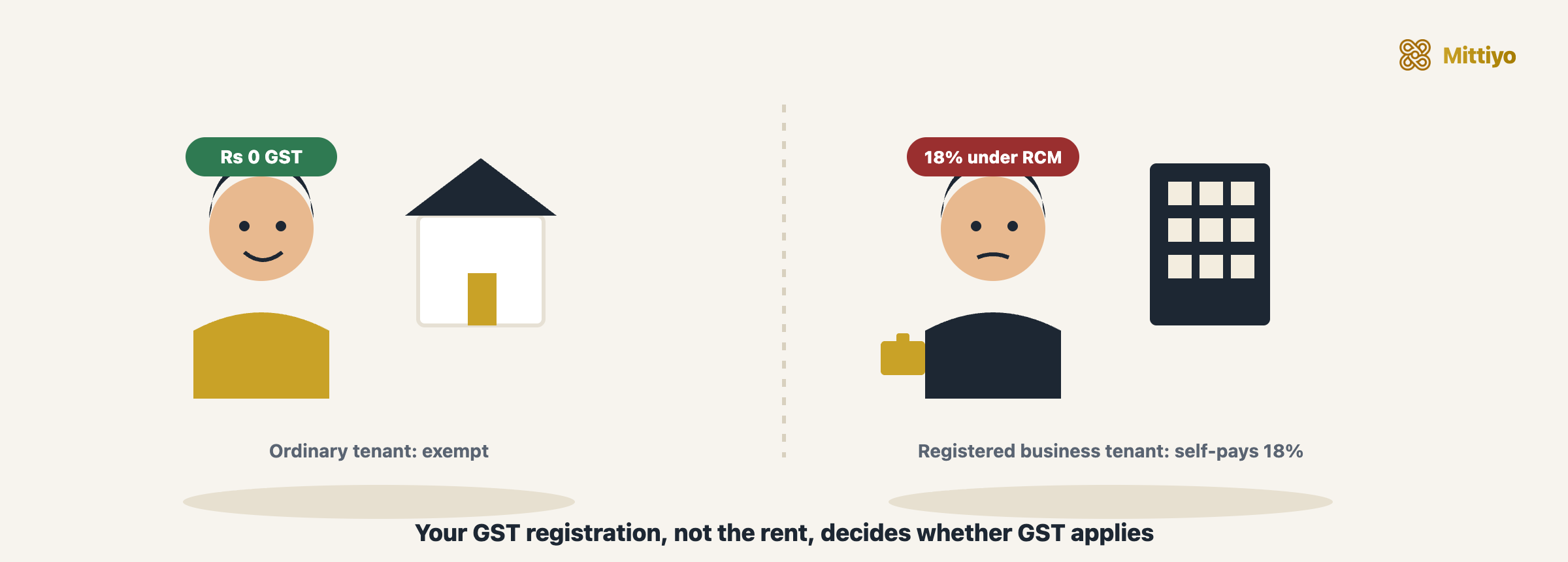

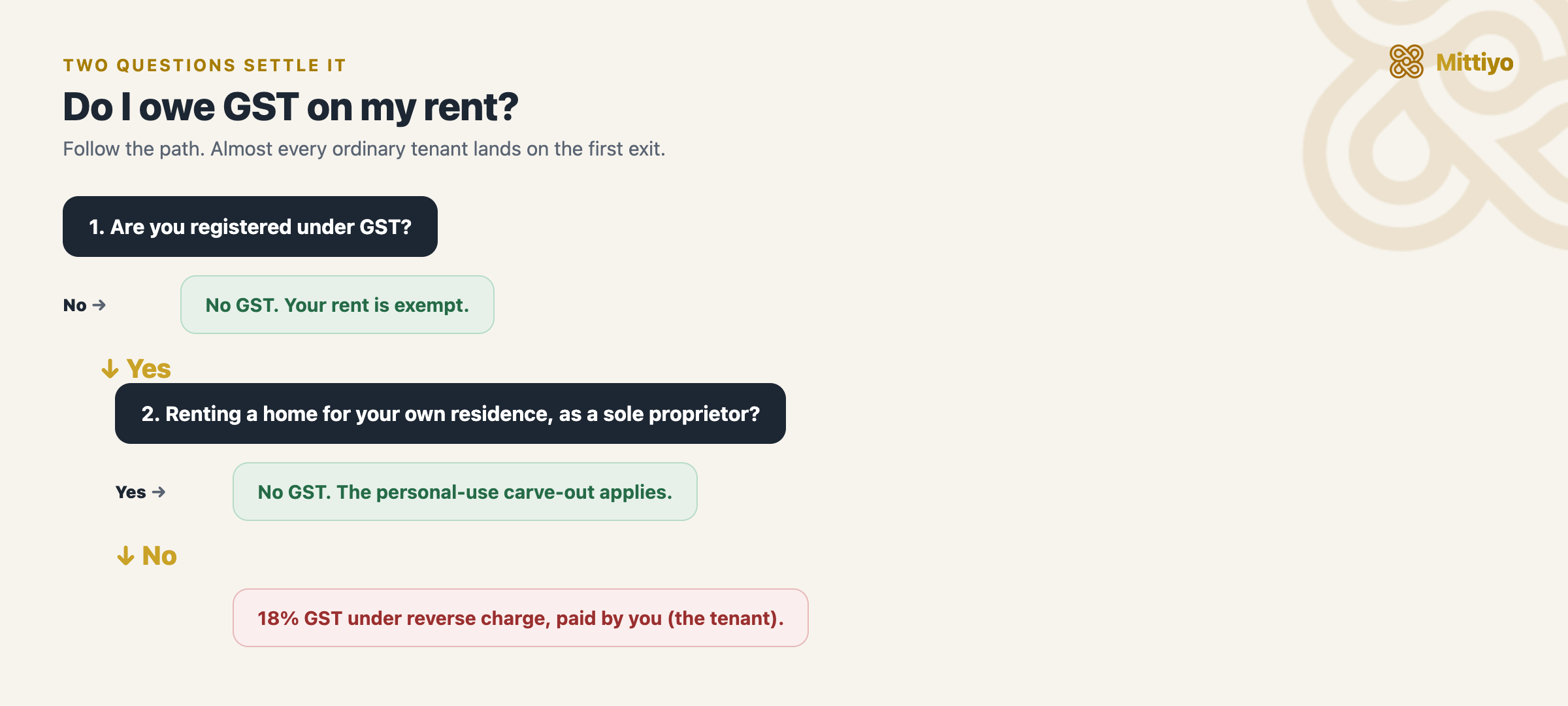

For almost everyone, the answer is short: if you are an ordinary tenant who is not registered under GST, you pay no GST on your home rent, whatever the amount. GST only enters the picture when the tenant is GST-registered.

Two questions settle almost every case.

Two questions settle almost every case.

The rest of this guide explains why: the July 2022 change that created the registered-tenant rule, the exceptions, and what compliance looks like if you are the one who has to pay.

Historical Context: GST and Rental Services Before July 2022

When the GST regime was introduced on July 1, 2017, residential rent received a blanket exemption. Entry 12 of Notification No. 12/2017-Central Tax (Rate), dated June 28, 2017, exempted “services by way of renting of residential dwelling for use as residence” from GST. This exemption was absolute, it applied regardless of who the landlord was, who the tenant was, and whether either party held a GST registration. The policy rationale was straightforward: housing is a basic necessity, and taxing residential rent would impose an additional burden on tenants without a clear policy benefit.

This meant that from 2017 to mid-2022, the position was uncomplicated. No residential landlord needed to worry about GST on rent, and no tenant had any GST obligation arising from their rental payment.

The Position Before GST (Service Tax Era)

Under the pre-GST service tax regime, renting of immovable property was a taxable service. However, renting of residential dwellings for use as residence was specifically excluded from the definition of “service” under Section 65B(44) of the Finance Act, 1994 (read with the negative list under Section 66D). Residential rent was therefore outside the scope of service tax entirely, not merely exempt, but excluded.

This distinction matters because an exemption can be withdrawn by notification, whereas an exclusion requires an amendment to the statute. The shift from exclusion (under service tax) to exemption (under GST) made residential rent potentially vulnerable to future changes, a vulnerability that materialized in 2022.

The July 2022 Change: What Happened and Why

The exemption for ordinary tenants survived every change; only registered persons were ever affected.

The exemption for ordinary tenants survived every change; only registered persons were ever affected.

The 47th GST Council Recommendation

The 47th meeting of the GST Council, held on June 28-29, 2022, recommended that the exemption for renting of residential dwellings should be modified. The Council’s concern was specific: GST-registered businesses and professionals were renting residential properties (often for employee accommodation or mixed use) and enjoying a tax advantage, no GST on the input side (rent), while claiming Input Tax Credit on other business inputs. This was seen as an anomaly that allowed tax leakage.

The Legal Implementation

The recommendation was implemented through Notification No. 04/2022-Central Tax (Rate), dated July 13, 2022, effective from July 18, 2022. The notification amended Entry 12 of the exemption notification to add a condition: the exemption for residential rent would no longer apply when the service is supplied to a registered person.

Simultaneously, Notification No. 05/2022-Central Tax (Rate) brought residential rent under the Reverse Charge Mechanism (RCM) when supplied to a registered person. This meant the tenant (being the registered person) would be responsible for paying GST, not the landlord.

What the Change Did NOT Do

It is equally important to understand the boundaries of this change:

- It did not impose GST on all residential rent. Rent paid by unregistered individuals remains fully exempt.

- It did not require landlords to register under GST. The RCM shifts the compliance burden entirely to the tenant.

- It did not change the treatment of commercial rent, which was already taxable at 18%.

- It did not affect service tax-era positions, which are governed by different legislation.

Current Legal Position: The Complete Framework

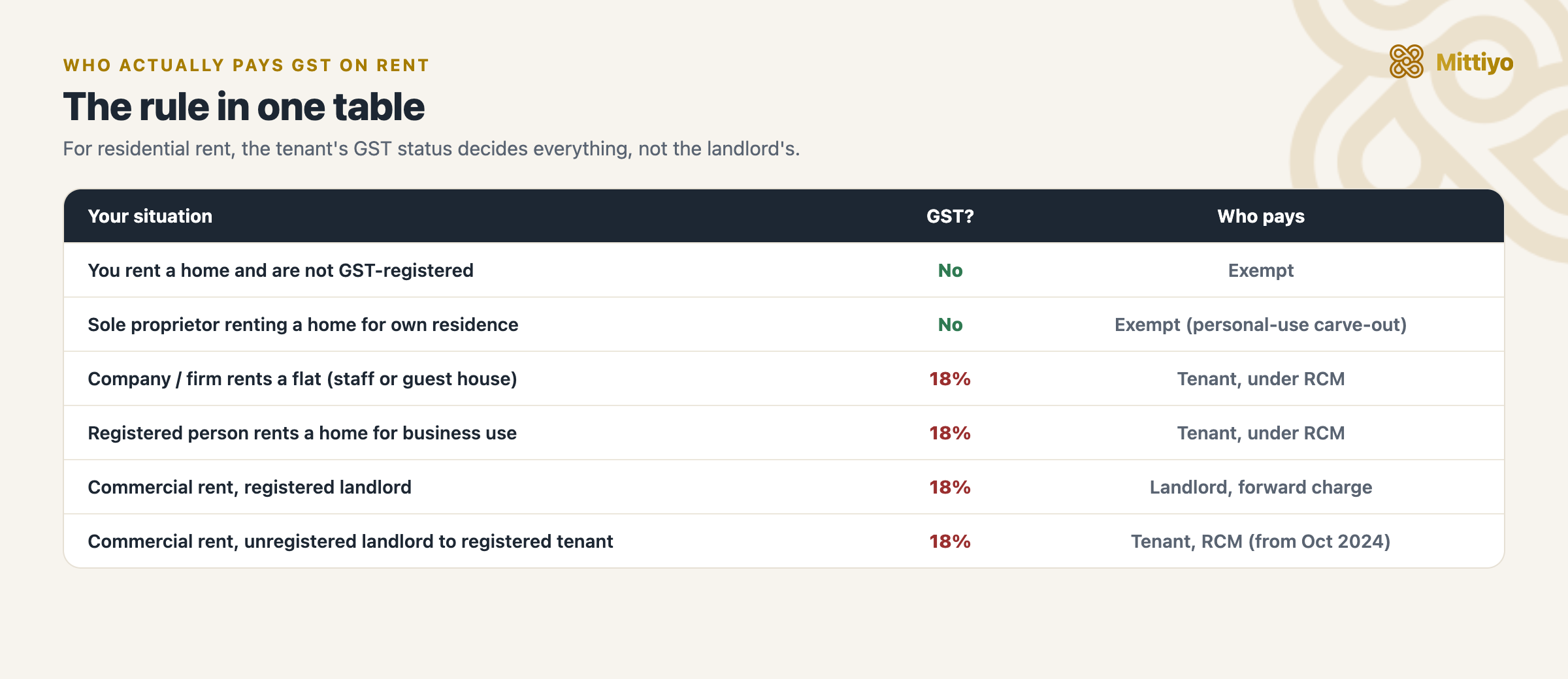

For residential rent, the tenant’s GST status decides everything, not the landlord’s.

For residential rent, the tenant’s GST status decides everything, not the landlord’s.

The following table captures every possible combination of landlord and tenant status and the resulting GST treatment as of 2026:

| Landlord GST Status | Tenant GST Status | Purpose of Use | GST Applicable? | Rate | Who Pays? | Mechanism |

|---|---|---|---|---|---|---|

| Unregistered | Unregistered | Residential | No | - | , | Exempt |

| Unregistered | Registered | Residential | Yes | 18% | Tenant | RCM |

| Registered | Unregistered | Residential | No | - | , | Exempt |

| Registered | Registered | Residential | Yes | 18% | Tenant | RCM |

| Registered (above Rs 20L) | Any | Commercial | Yes | 18% | Landlord | Forward charge |

| Unregistered (below Rs 20L) | Any | Commercial | No | - | , | Below threshold |

The critical determinant is the tenant’s GST registration status, not the landlord’s. If the tenant is registered under GST for any reason, whether as a company, LLP, partnership firm, or individual professional, GST at 18% applies on residential rent under RCM, subject to the important personal-use exception below.

The personal-use exception (from January 2023)

The July 2022 change created an obvious hardship: a GST-registered individual, say a sole proprietor, would owe 18% RCM even on the flat where their own family lives, with no genuine business use. The GST Council fixed this at its 48th meeting, and the carve-out took effect from 1 January 2023 through Notification No. 15/2022-Central Tax (Rate).

Under this exception, RCM does not apply where:

- the registered person is the proprietor of a proprietorship concern and rents the residential dwelling in their personal capacity for use as their own residence, and

- the renting is on their own account, not on the account of the proprietorship.

In plain terms: if you are GST-registered only because you run a proprietorship, and you rent a home purely to live in (not booked as a business expense, not used as an office), your home rent stays exempt, the same as for any ordinary tenant. The 18% RCM bites when the registered tenant is a company, firm, or LLP, or when an individual rents the dwelling for business use rather than as their own residence.

Understanding the Reverse Charge Mechanism for Rent

What Is RCM?

Under the normal GST mechanism (forward charge), the supplier of a service charges GST, collects it from the recipient, and remits it to the government. Under the Reverse Charge Mechanism, this flow is inverted: the recipient of the service is responsible for paying GST directly to the government.

RCM is not unique to rent. It applies across several categories of services specified in Section 9(3) and 9(4) of the CGST Act, 2017, and corresponding provisions of the respective SGST/UTGST Acts. Residential rent to registered persons was added to this list through the July 2022 notification.

How RCM Works for Residential Rent: Step by Step

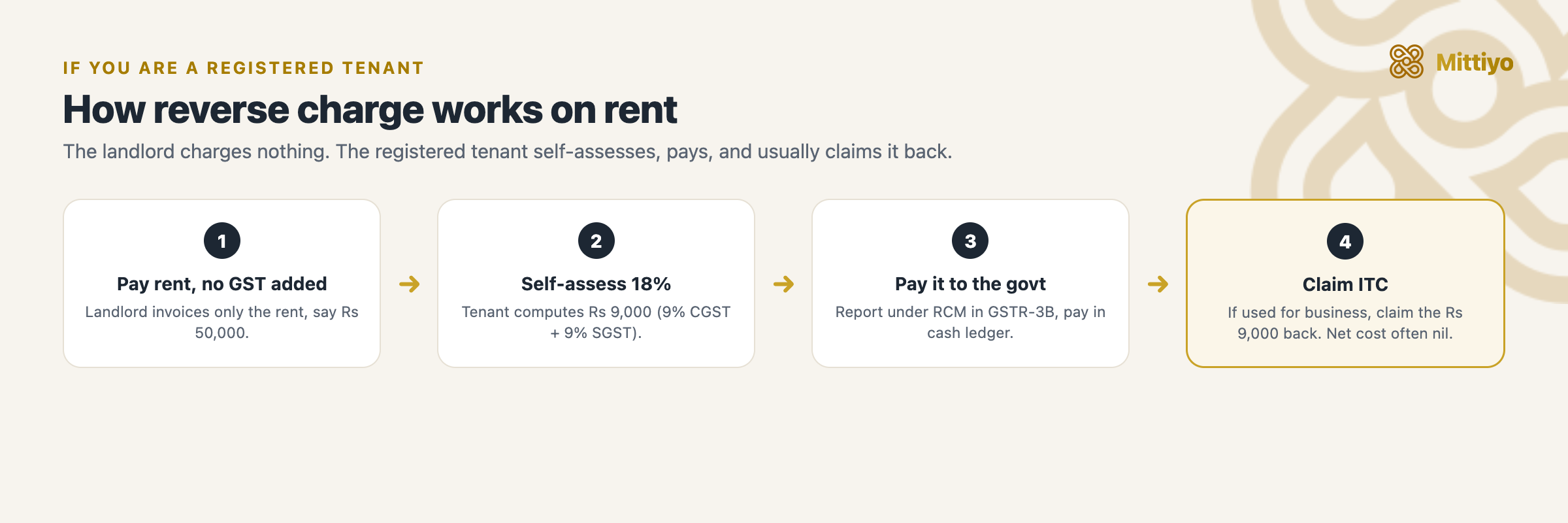

The landlord charges nothing; the registered tenant self-assesses, pays, and usually claims it back.

The landlord charges nothing; the registered tenant self-assesses, pays, and usually claims it back.

Consider a scenario where XYZ Pvt. Ltd. (a GST-registered company) rents a residential apartment from Mr. Mohan (an unregistered individual landlord) at Rs 50,000 per month for employee accommodation.

Step 1, Rent payment: XYZ pays Rs 50,000 rent to Mr. Mohan. No GST is added to this amount. Mr. Mohan’s invoice (or rent receipt) shows Rs 50,000.

Step 2, GST self-assessment: XYZ calculates GST at 18% on the rent: Rs 50,000 x 18% = Rs 9,000 (Rs 4,500 CGST + Rs 4,500 SGST/UTGST).

Step 3, GST payment: XYZ pays Rs 9,000 GST to the government through its regular GST return. This is paid from XYZ’s own funds, it is not deducted from Mr. Mohan’s rent.

Step 4, GSTR-3B reporting: XYZ reports the RCM liability in Table 3.1(d) of its GSTR-3B return for the relevant month.

Step 5, Input Tax Credit: XYZ can claim ITC of Rs 9,000 on the GST paid under RCM, subject to the conditions and restrictions under Section 16 and Section 17(5) of the CGST Act. If the apartment is used exclusively for the employee’s residence (and not for business purposes), the ITC eligibility depends on whether it qualifies under the “in the course or furtherance of business” test.

The ITC Question: Can It Be Claimed?

The availability of ITC on GST paid under RCM on residential rent is nuanced:

ITC is generally available because Section 16(1) of the CGST Act allows ITC on goods and services used in the course or furtherance of business. Employee accommodation provided as part of employment terms falls within this scope.

ITC restrictions under Section 17(5): This section lists specific categories where ITC is blocked. The relevant entries are:

- Section 17(5)(b)(i): Works contract services for construction of immovable property, not applicable to rent.

- Section 17(5)(g): Goods or services used for personal consumption, if the company rents an apartment for its director’s personal use (not as part of employment terms), ITC may be blocked.

- Section 17(5)(d): Goods or services received by a taxable person for construction of immovable property on his own account, not applicable to rent.

Practical position: In most cases where a company rents residential accommodation for employees as part of their employment terms, ITC on the RCM GST is available. The effective additional cost to the company is therefore nil, the Rs 9,000 paid as GST is recovered through ITC.

However, when a GST-registered individual (such as a freelance consultant) rents an apartment purely for personal residence, the ITC position is less clear. If the apartment is not used for business purposes at all, claiming ITC may not be defensible.

Detailed Scenarios and Analysis

Scenario 1: Salaried Individual Renting from an Individual Landlord

Profile: Ananya, a salaried software engineer (not GST-registered), rents a 2BHK apartment from Mr. Desai (retired, not GST-registered) at Rs 30,000 per month.

GST position: No GST applies. Both parties are unregistered. The exemption under Entry 12 of Notification 12/2017-CT(Rate), as amended, applies fully. Ananya pays Rs 30,000 rent; no GST compliance is required by either party.

What if Ananya’s rent exceeds Rs 50,000 per month? Still no GST. There is no rent threshold for GST applicability. The Rs 20 lakh turnover threshold applies to the landlord’s aggregate turnover for GST registration purposes, not to rent amounts.

Scenario 2: Company Renting for Employee Accommodation

Profile: TechStar Solutions Pvt. Ltd. (GST-registered) rents a 3BHK apartment from Mrs. Kulkarni (unregistered) at Rs 75,000 per month for its CTO’s residence.

GST position: GST at 18% applies under RCM. TechStar must self-assess and pay Rs 13,500 GST (Rs 6,750 CGST + Rs 6,750 SGST) per month. TechStar can claim ITC on this amount since the accommodation is provided as part of the CTO’s employment terms.

Mrs. Kulkarni’s obligations: None. She continues to receive Rs 75,000 rent. She does not need to register for GST or file any GST returns. The entire GST compliance burden is on TechStar.

Scenario 3: GST-Registered Professional Renting a Personal Residence

Profile: Dr. Ramesh runs his practice as a sole proprietorship and is GST-registered. He rents a residential apartment at Rs 40,000 per month purely for his family’s residence, with no part used for his practice.

GST position: No GST. Since the January 2023 carve-out, a proprietor who rents a home in their personal capacity for their own residence, on their own account and not the proprietorship’s, is exempt under Notification 15/2022-CT(Rate). Dr. Ramesh charges nothing extra and pays no RCM, exactly like an ordinary tenant.

The earlier position: Between July 2022 and December 2022, this same arrangement did attract 18% RCM, which was widely criticised as an unintended hardship. The carve-out fixed it. Note the limits: if Dr. Ramesh used part of the flat as a clinic or booked the rent as a business expense, RCM would apply on the business-use renting, and the exemption would not cover it.

Scenario 4: Proprietorship Using Residence Partly as Office

Profile: Meera operates a graphic design business as a sole proprietorship (GST-registered). She rents an apartment for Rs 25,000 per month and uses one room as her home office.

GST position: GST at 18% applies under RCM on the full rent amount (Rs 4,500 per month). For ITC purposes, Meera may need to apportion, claiming ITC only on the portion of rent attributable to business use. If one room out of four is used for business, the defensible ITC claim would be 25% of the GST paid (Rs 1,125 per month). The remaining Rs 3,375 is a genuine cost.

Scenario 5: Partnership Firm Renting for Partners

Profile: Sharma & Associates (a chartered accountancy firm, GST-registered) rents two apartments for its senior partners.

GST position: GST at 18% applies under RCM on both apartments. The firm pays GST and can claim ITC if the accommodation is part of the partnership deed’s terms for partner remuneration/benefits.

Scenario 6: NRI Landlord, Domestic Tenant

Profile: Priya (unregistered individual) rents an apartment from Mr. Iyer, an NRI who owns the property in India.

GST position: No GST. The tenant is unregistered, so the exemption applies. The landlord’s NRI status does not change the analysis, as the property is located in India and the service is consumed in India.

TDS on Rent Under Income Tax: A Related Obligation

While GST and income tax are separate systems, tenants often confuse GST on rent with TDS on rent. The distinction is important:

Section 194-IB of the Income Tax Act, 1961

Any individual or HUF (not subject to tax audit) paying rent exceeding Rs 50,000 per month is required to deduct TDS at 2% of the rent. This was introduced by the Finance Act, 2017 and has been applicable since June 1, 2017. The rate was revised to 2% effective October 1, 2024 (previously 5%).

Key differences from GST:

| Parameter | GST on Rent | TDS on Rent (Section 194-IB) |

|---|---|---|

| Trigger | Tenant’s GST registration status | Rent exceeding Rs 50,000/month |

| Rate | 18% | 2% |

| Who pays | Tenant (RCM) | Tenant deducts from rent, pays to IT department |

| Credit | ITC (if eligible) | Landlord claims TDS credit against income tax |

| Return | GSTR-3B | Form 26QC (within 30 days of financial year end or lease termination) |

Practical note: A salaried individual paying Rs 60,000 monthly rent to an unregistered landlord has no GST obligation but must deduct TDS at 2% (Rs 1,200 per month), pay it using Form 26QC, and issue Form 16C to the landlord.

GST Registration Threshold and Residential Rent

A common question from landlords: does rental income count toward the Rs 20 lakh GST registration threshold?

Answer: Residential rental income that is exempt from GST is not included in the computation of aggregate turnover for the purpose of determining whether the Rs 20 lakh threshold is crossed. Under Section 2(6) of the CGST Act, aggregate turnover includes exempt turnover, but a specific exclusion applies to the value of exempt supplies that are not leviable to tax. Since residential rent to unregistered tenants is an exempt supply, it does count toward aggregate turnover, but since the supply itself remains exempt, crossing the threshold does not change the GST treatment of the rent.

However, if the landlord also earns commercial rent or provides other taxable services, those amounts do count. If the aggregate turnover (including exempt residential rent) exceeds Rs 20 lakh, the landlord must register under GST, but the residential rent remains exempt as long as the tenant is unregistered.

Commercial property: a 2024 change for registered tenants

Residential rent is the focus of this guide, but a parallel change on the commercial side catches registered tenants out, so it is worth flagging. Renting of commercial or other non-residential immovable property attracts 18% GST, normally charged by a registered landlord under forward charge.

From 10 October 2024, a reverse-charge twist was added (Notification 09/2024-CT(Rate), following the 54th GST Council). Where an unregistered landlord rents commercial or other immovable property to a GST-registered tenant, the tenant must now pay 18% GST under RCM. This catches registered businesses that rent a shop or office from a small, unregistered owner and assume no GST arises. It does not affect residential rent used as a residence, which stays governed by the rules above.

Common Misconceptions Addressed

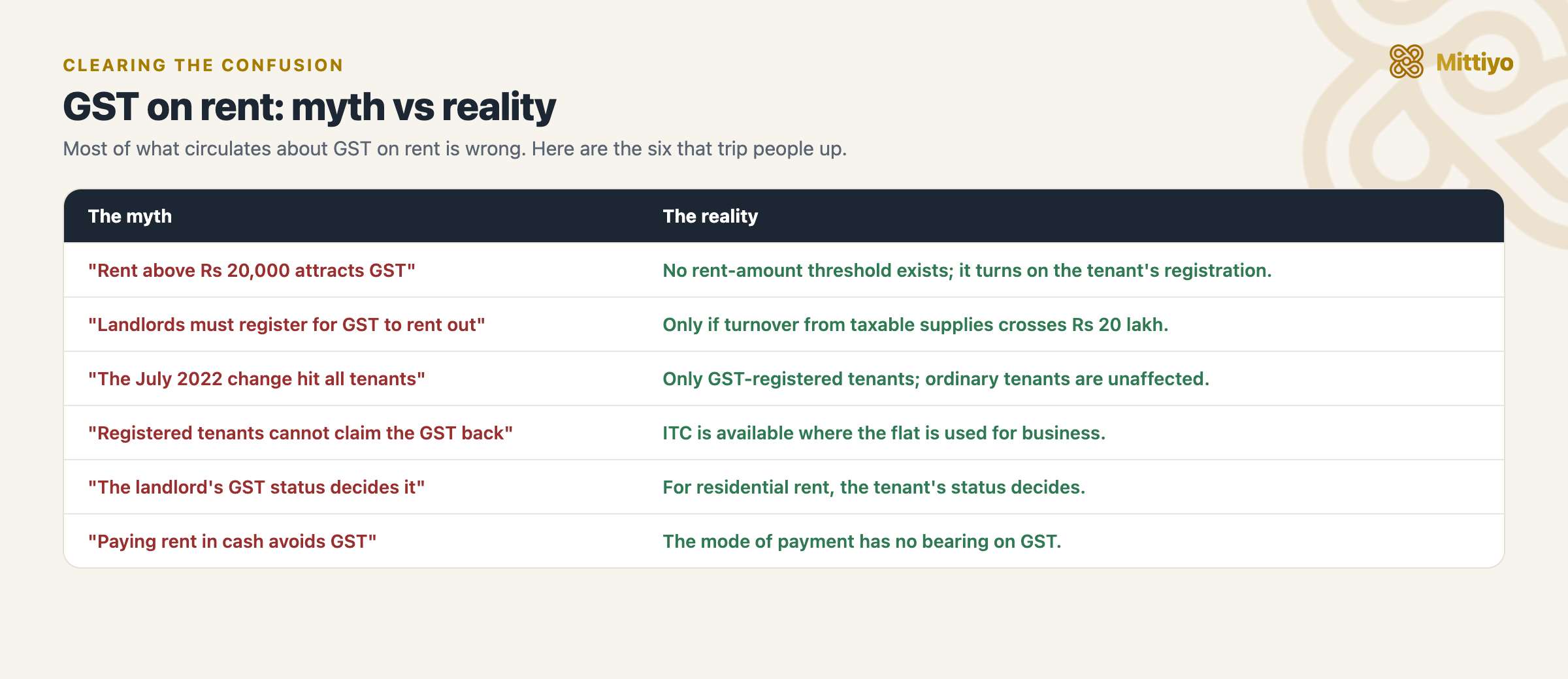

Most of what circulates about GST on rent is wrong. These six are the usual culprits.

Most of what circulates about GST on rent is wrong. These six are the usual culprits.

Misconception 1: All rent above Rs 20,000 per month attracts GST

Reality: There is no rent amount threshold for GST applicability. The Rs 20 lakh threshold is for the landlord’s aggregate annual turnover for GST registration purposes, not for individual rent amounts. A tenant paying Rs 2 lakh per month in residential rent has no GST obligation if the tenant is not GST-registered.

Misconception 2: Landlords must register for GST if they rent out property

Reality: A landlord earning only residential rental income does not need to register for GST, regardless of the rent amount. GST registration is required only if the landlord’s aggregate turnover from all taxable supplies exceeds Rs 20 lakh (Rs 10 lakh in special category states).

Misconception 3: The July 2022 change applies to all tenants

Reality: The change affects only GST-registered tenants. Unregistered individuals, which includes the vast majority of residential tenants in India, are completely unaffected. Their rent remains exempt.

Misconception 4: Tenants cannot claim ITC on rent GST

Reality: GST-registered tenants paying GST under RCM can claim Input Tax Credit, subject to the conditions under Sections 16 and 17(5) of the CGST Act. For companies providing employee accommodation, the ITC is typically fully available, making the net additional cost nil.

Misconception 5: The landlord’s GST status determines whether rent is taxable

Reality: For residential rent, the tenant’s registration status is the determining factor, not the landlord’s. Even if the landlord is GST-registered, residential rent to an unregistered tenant remains exempt.

Misconception 6: Paying rent in cash avoids GST

Reality: The mode of payment (cash, cheque, bank transfer) has no bearing on GST applicability. The tax treatment depends solely on the registration status of the parties and the purpose of use.

Compliance Checklist for GST-Registered Tenants

If you are a GST-registered person (company, firm, or individual) renting residential property, the following compliance steps apply:

- Self-assess GST at 18% on the monthly rent amount (calculate CGST at 9% and SGST/UTGST at 9% separately).

- Report in GSTR-3B under Table 3.1(d), liability payable under RCM.

- Pay GST through the electronic cash ledger (RCM liability cannot be discharged using ITC balance).

- Claim ITC in the same GSTR-3B return under Table 4A, provided the conditions for ITC eligibility are met.

- Report in GSTR-1, outward supply details are not required for RCM supplies.

- Maintain records of rent agreements, rent receipts, and GST payment challans.

- Reconcile the RCM liability monthly to ensure no shortfall in GST payment.

Impact on Rental Market Dynamics

The July 2022 change has had observable effects on certain segments of the rental market:

Corporate leasing: Companies that rent residential properties for employees now factor in the 18% GST as part of their accommodation cost. Since ITC is usually available, the net impact on companies is often neutral. However, the additional compliance burden (monthly RCM calculations, return filings) adds administrative costs.

Professional tenants: Individual professionals with GST registration (doctors, lawyers, chartered accountants, consultants) face a genuine 18% cost increase on residential rent if they cannot claim ITC. Some professionals have explored restructuring their arrangements, for example, renting through an unregistered family member, though the anti-avoidance implications of such arrangements should be carefully considered.

Co-living and PG accommodation: The GST position for co-living spaces and paying guest accommodations can differ depending on whether the arrangement is classified as “renting of residential dwelling” or as “hotel/inn accommodation.” The latter attracts GST at rates varying from exempt (below Rs 1,000 per day) to 18%, depending on the declared tariff.

Key Takeaways

- Individual, non-GST-registered tenants paying residential rent have no GST obligation. No action is required; the exemption applies fully.

- GST-registered tenants (companies, firms, professionals) renting residential property must self-assess and pay 18% GST under the Reverse Charge Mechanism.

- The landlord has no GST collection obligation on residential rent, regardless of the landlord’s own GST status.

- ITC on GST paid under RCM is available to tenants who use the accommodation in the course or furtherance of business, subject to Section 17(5) restrictions.

- The July 2022 change (Notification 04/2022-CT(Rate)) narrowed the residential rent exemption; it did not eliminate it for unregistered tenants.

- TDS under Section 194-IB (2% on rent exceeding Rs 50,000/month) is a separate income tax obligation and should not be confused with GST.

- Commercial rent follows standard forward charge GST rules at 18% if the landlord is registered.

- Landlords earning only exempt residential rental income are not required to register under GST.

Renting a home you will never owe GST on?

For an ordinary tenant, GST is a non-issue, but the building still is. Before you sign, see what residents say a building actually rents for, the deposit, the society, and the water and power reality, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; GST treatment can turn on specific facts, so confirm your own position with a qualified chartered accountant or GST practitioner.

Related guides: TDS on rent (Section 194-IB) · Rental income tax for landlords · NRI landlord guide

References

- Central Goods and Services Tax Act, 2017, Sections 2(6), 9(3), 9(4), 16, 17(5)

- GST Council, Central Tax (Rate) notifications (Notification 12/2017 exemption Entry 12; 04/2022 narrowing; 05/2022 RCM Entry 5AA; 15/2022 personal-use carve-out; 09/2024 commercial RCM Entry 5AB)

- CBIC Tax Information Portal (the official portal for GST notification and circular text, including Circular 172/04/2022-GST)

- 47th GST Council recommendations, Press Information Bureau (the July 2022 change)

- 48th GST Council recommendations, Press Information Bureau (the January 2023 personal-use carve-out)

- 54th GST Council recommendations, Press Information Bureau (the October 2024 commercial-property RCM)

- Income-tax Act, 1961, Section 194-IB (TDS on rent, a separate obligation)