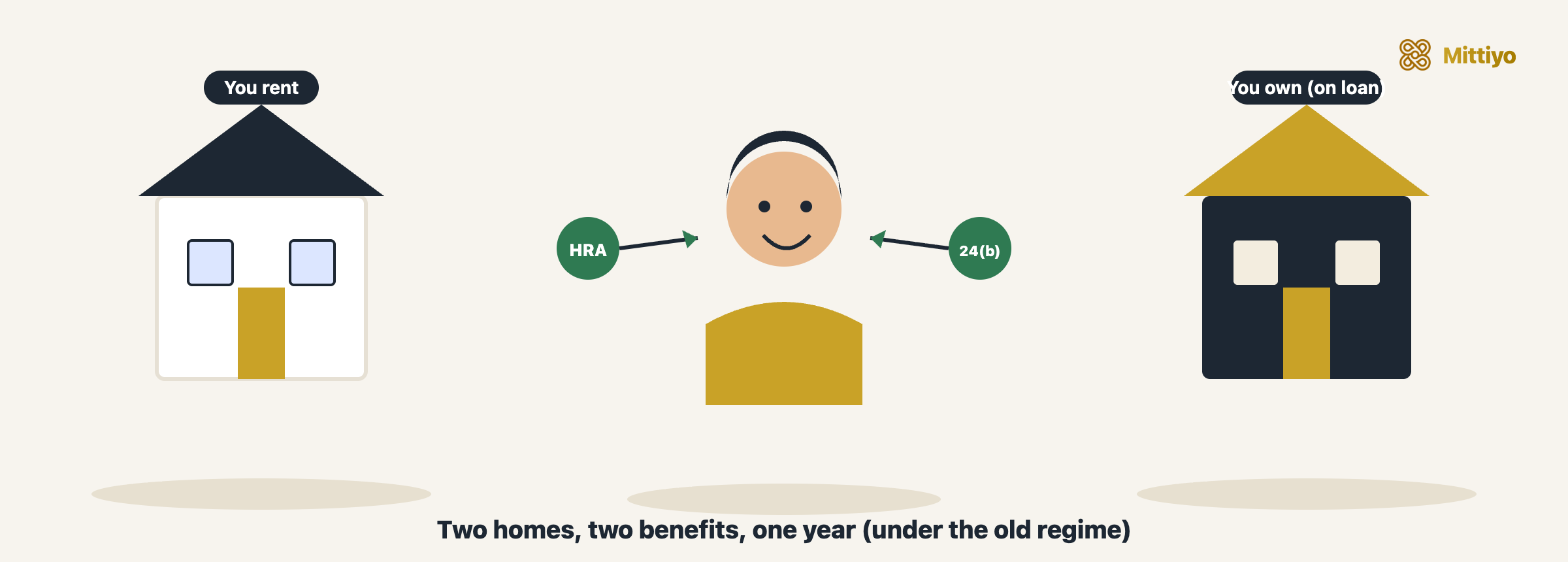

It is one of the most common questions at tax-filing time, and one of the most misunderstood: if you are paying rent and also repaying a home loan, can you claim the tax benefits for both in the same year? The short answer is yes. The Income-tax Act treats your rent and your home loan as two separate situations, and nothing stops you from claiming both at once, as long as each claim is genuine.

The real catch is not some hidden rule about the same city. It is the tax regime. Under the new regime, which is now the default, House Rent Allowance and self-occupied home loan interest both vanish. Most people who could claim both have to actively opt for the old regime to do so. Get the regime right and the rest is straightforward. This guide walks through when both apply, the much-debated same-city case, the exact limits, and the documentation that keeps your claim safe.

The short answer

There is no section in the Income-tax Act, 1961 that says you cannot claim HRA and home loan benefits together. They live in different parts of the Act:

- HRA exemption is under Section 10(13A), and it exists because you are paying rent for the place you actually live in.

- Home loan interest is under Section 24(b), and principal repayment under Section 80C, because you have borrowed to buy or build a house.

Owning a house and paying rent are not mutually exclusive. People own a flat in their hometown and rent near their job. People buy a flat as an investment, let it out, and rent the home they live in. People buy a house that is still under construction and rent in the meantime. In all of these, both claims are legitimate.

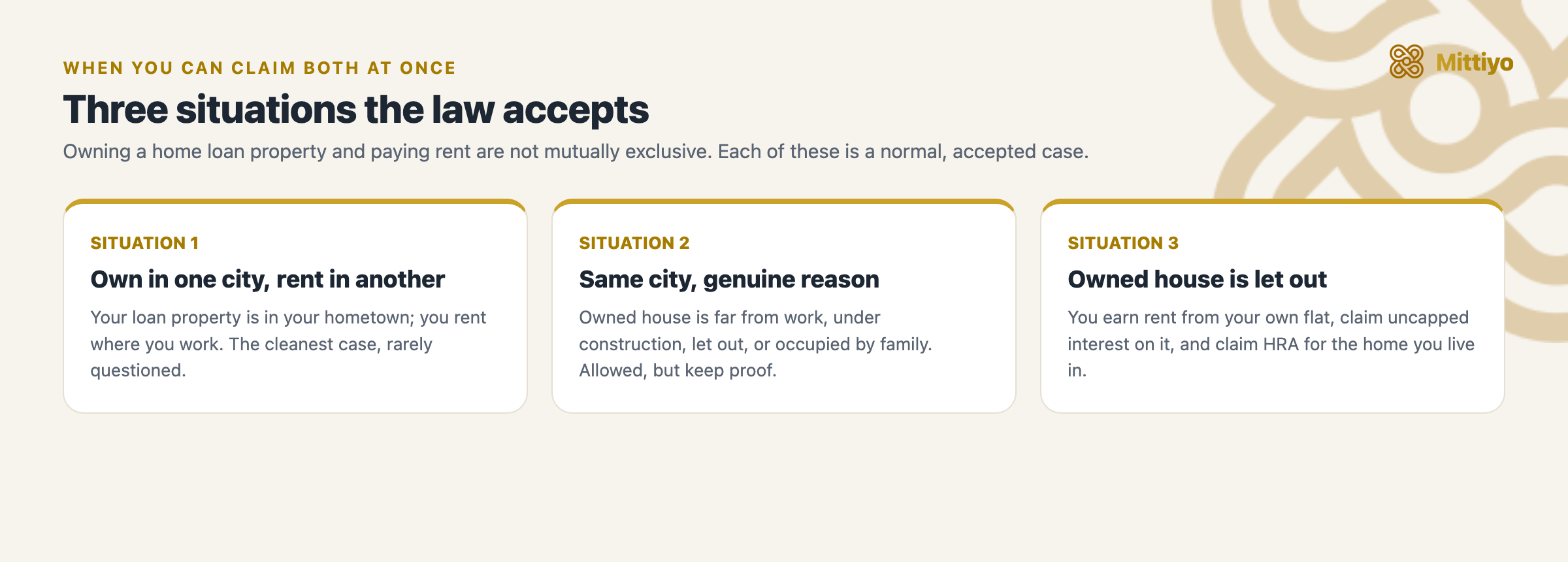

The three situations where both apply

Each of these is a normal, accepted reason to be paying rent while owning a home loan property.

Each of these is a normal, accepted reason to be paying rent while owning a home loan property.

1. You own in one city and rent in another. This is the cleanest case. Your home loan property is in, say, your hometown, and you live on rent in the city where you work. Claim HRA for the rented home and Section 24(b) interest for the owned one. No one questions this.

2. You own and rent in the same city, with a genuine reason. This is allowed too, but it is where claims get scrutinised. The law does not ban it. What it requires is a real reason you cannot live in your own house: it is too far from your workplace, it is under construction, it is let out, or your parents or family live in it. If your owned flat and rented flat are on the same street with no explanation, expect the exemption to be challenged.

3. Your owned house is let out, and you live on rent. Here you declare the rental income from your owned property, claim the (uncapped) interest against it under Section 24(b), and separately claim HRA for the home you rent. Common for investors and for people whose own flat is in an inconvenient location.

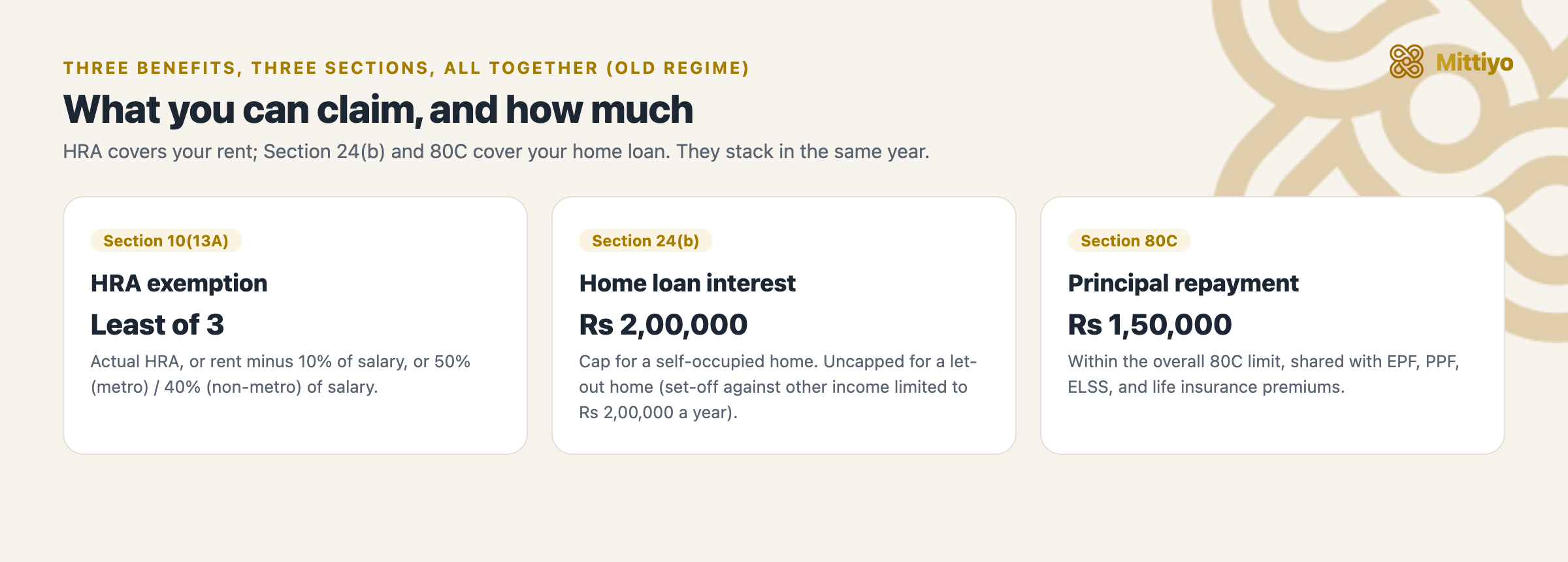

How much each benefit is worth

Three separate benefits, three separate sections, all available together under the old regime.

Three separate benefits, three separate sections, all available together under the old regime.

HRA exemption (Section 10(13A)) is the least of these three:

- the actual HRA component in your salary,

- rent paid minus 10% of salary, and

- 50% of salary if you live in a metro (Delhi, Mumbai, Kolkata, Chennai), or 40% if you do not.

Here “salary” means basic plus dearness allowance.

Home loan interest (Section 24(b)):

- Self-occupied property: deduction capped at Rs 2,00,000 a year.

- Let-out property: the actual interest, with no cap. But the loss from house property that you can set off against your other income (salary, etc.) in the same year is limited to Rs 2,00,000 under Section 71, and any excess is carried forward for up to eight years.

Principal repayment (Section 80C) qualifies within the overall Rs 1,50,000 Section 80C limit, shared with your other 80C investments like EPF, PPF, and life insurance.

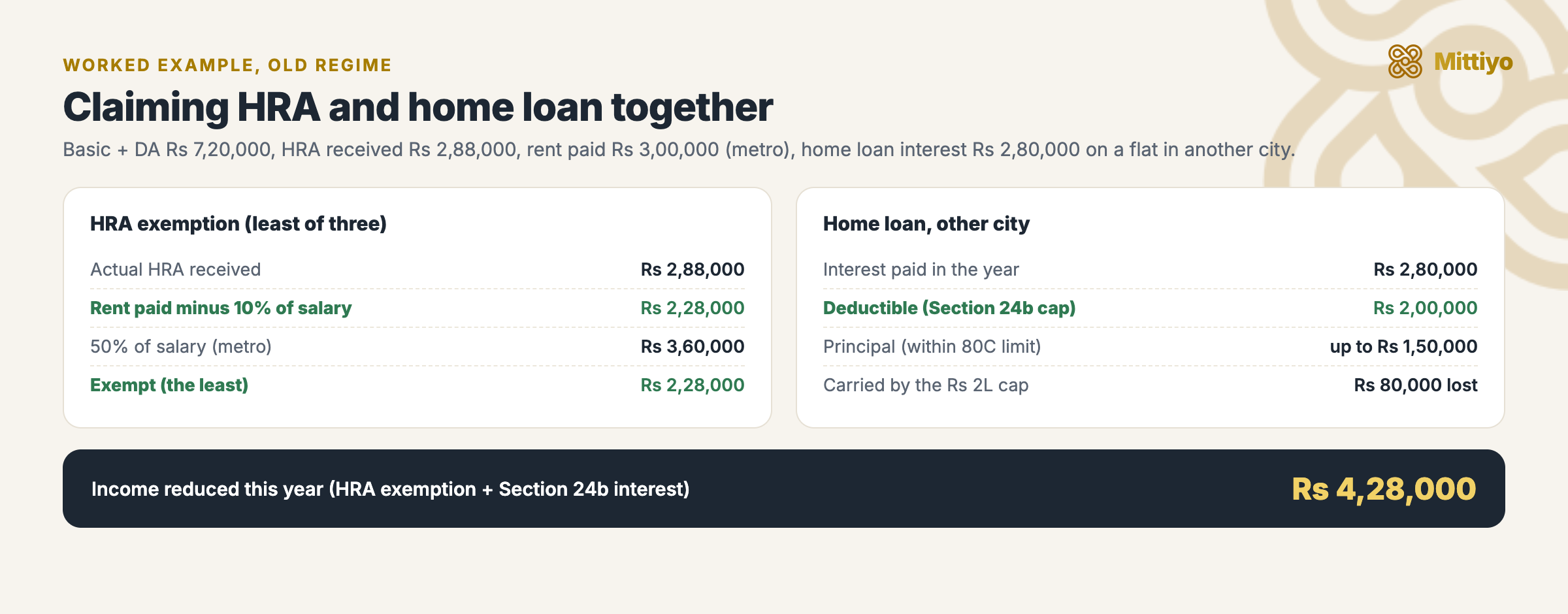

A worked example: claiming both

Numbers make this concrete. Take a salaried employee in a metro with basic plus dearness allowance of Rs 7,20,000 a year, an HRA component of Rs 2,88,000, paying rent of Rs 3,00,000 a year, and a home loan on a flat in another city on which the year’s interest comes to Rs 2,80,000.

One salary, two benefits: Rs 2,28,000 of HRA exempt plus Rs 2,00,000 of interest, claimed together.

One salary, two benefits: Rs 2,28,000 of HRA exempt plus Rs 2,00,000 of interest, claimed together.

HRA exemption is the least of three figures: the actual HRA (Rs 2,88,000), rent paid minus 10% of salary (Rs 3,00,000 minus Rs 72,000, that is Rs 2,28,000), and 50% of salary for a metro (Rs 3,60,000). The least is Rs 2,28,000, so that much of the HRA is exempt and the remaining Rs 60,000 is added to taxable salary.

Home loan interest under Section 24(b) is Rs 2,80,000, but for a self-occupied or deemed self-occupied property the deduction is capped at Rs 2,00,000 (the extra Rs 80,000 is simply not deductible this year). Principal repaid counts towards the Rs 1,50,000 Section 80C limit.

Together, this taxpayer reduces taxable income by Rs 4,28,000 (Rs 2,28,000 HRA exemption plus Rs 2,00,000 interest) in the same year, before even counting the 80C principal, and entirely legitimately. None of it is available if they stay on the new regime.

Joint home loans and co-owned property

If the loan is taken jointly and the property is co-owned, each co-owner who is also a co-borrower can claim the deductions in proportion to their share. So a couple who co-own a flat and are joint borrowers can each claim their share of the interest, each up to Rs 2,00,000 for a self-occupied property, and each up to Rs 1,50,000 of principal under 80C, effectively doubling the household benefit. Two conditions matter: you must be both a co-owner and a co-borrower to claim, and the split must follow the actual ownership share, not one assigned for convenience.

The same-city question, settled

This is the part people get wrong in both directions. Some believe you can never claim both in the same city. Others assume you always can. Neither is right.

The Income-tax Act has no same-city restriction. What it has is a genuineness test. HRA exemption is meant for rent you actually have to pay. If you own a perfectly usable house in the same city and choose to rent the flat next door purely to claim HRA, that is not a genuine reason, and the exemption can be disallowed.

But there are many genuine same-city reasons, and they are accepted:

- the owned house is far from your workplace and the commute is impractical,

- the owned house is under construction or not yet possession-ready,

- the owned house is let out to a tenant,

- the owned house is occupied by your parents or family,

- the owned house is too small for your current family needs.

If any of these is true, claim both. Just keep the reasoning and the paperwork ready: a rent agreement, rent paid by bank transfer, the landlord’s PAN where required, and a one-line explanation of the distance or occupancy. The claim is defensible; the documentation is what defends it.

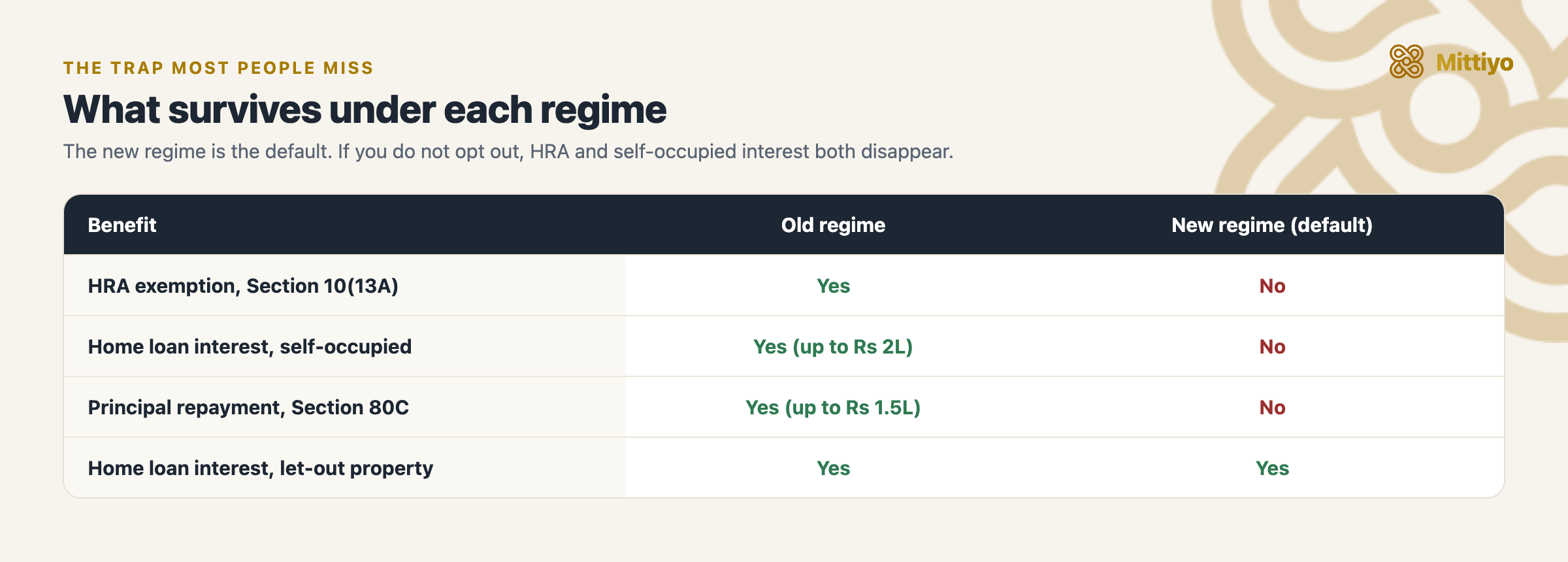

The new regime trap

Under the default new regime, the benefits that make this whole question worth asking mostly disappear.

Under the default new regime, the benefits that make this whole question worth asking mostly disappear.

Everything above assumes the old tax regime. Under the new regime, which is the default since FY 2023-24 (and the one you are taxed under unless you opt out):

- HRA exemption: not available.

- Self-occupied home loan interest: not available.

- Section 80C principal: not available.

- Let-out property interest: still available under Section 24(b).

So for most salaried people, the entire benefit of claiming HRA plus self-occupied home loan interest exists only if they choose the old regime. A salaried taxpayer can switch between regimes each year while filing the return, so the practical step is to compute your tax both ways: old regime with HRA and home loan deductions, versus new regime with its lower slab rates and the Rs 75,000 standard deduction, and then pick whichever leaves you paying less.

Documentation checklist

Keep these ready before you file:

- For HRA: rent agreement, rent receipts, rent paid through a traceable channel (bank transfer or UPI), and the landlord’s PAN if annual rent exceeds Rs 1,00,000.

- For the home loan: the lender’s annual interest certificate (showing the interest and principal split), and proof of ownership and possession.

- If owned and rented are in the same city: a short, honest note on why you cannot occupy your own house (distance, construction, tenancy, family).

Common mistakes to avoid

- Staying on the new regime by default and losing both benefits without realising it.

- Paying rent in cash with no agreement or bank trail, then being unable to substantiate the HRA claim.

- Claiming HRA with no genuine reason for renting next to your own usable house.

- Forgetting the landlord’s PAN when annual rent crosses Rs 1,00,000, which can lead to the exemption being denied.

- Treating the let-out interest as fully deductible against salary in one year, when the set-off against other income is capped at Rs 2,00,000 (the rest carries forward).

Key takeaways

- HRA and home loan tax benefits can be claimed in the same year. There is no statutory bar, including in the same city.

- The same-city case needs a genuine reason for not living in your own house, backed by documentation.

- Self-occupied interest is capped at Rs 2,00,000; let-out interest is uncapped but the annual set-off against other income is limited to Rs 2,00,000.

- Under the new (default) regime, HRA, self-occupied interest, and 80C are all gone; only let-out interest survives. Opt for the old regime if you need them, and compare both before filing.

About to sign a new rent agreement?

Your HRA claim is only as solid as the home and the rent behind it. Before you commit, see what residents say a building actually rents for, the deposit, the society, and the water and power reality, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: HRA exemption for salaried tenants · Section 80GG, if you do not receive HRA · Rent receipts for tax

References

- Income-tax Act, 1961, Section 10(13A) (House Rent Allowance), Section 24(b) (interest on borrowed capital), Section 71 (set-off of house-property loss), and Section 80C (principal repayment)

- Income tax e-filing portal (regime choice and return filing)

- Threshold limits under the Income-tax Act, Income Tax Department