For a salaried tenant, the income tax return is where two things you have been doing all year, paying rent and earning a salary, finally meet the tax department. Get the order right and it takes an evening. Get it wrong, usually by leaving the regime on default, and you can quietly forfeit your House Rent Allowance and pay thousands more than you needed to.

This is a practical, step-by-step checklist for filing your return for AY 2026-27 (the financial year 2025-26). The deadline for most salaried filers is 31 July 2026. The one thing to internalise before you start: the new tax regime is the default, and it removes HRA. If your tax planning relies on rent, you must actively choose the old regime. Everything below builds around that.

The deadline, and the cost of missing it

The due date to file for AY 2026-27, for individuals who do not need a tax audit, is 31 July 2026. You can still file after that as a belated return, but it costs you:

- a late fee under Section 234F: Rs 1,000 if your total income is up to Rs 5,00,000, otherwise Rs 5,000,

- interest under Section 234A on any unpaid tax, and

- the loss of certain carry-forward benefits.

File on time and none of this applies. Now the steps.

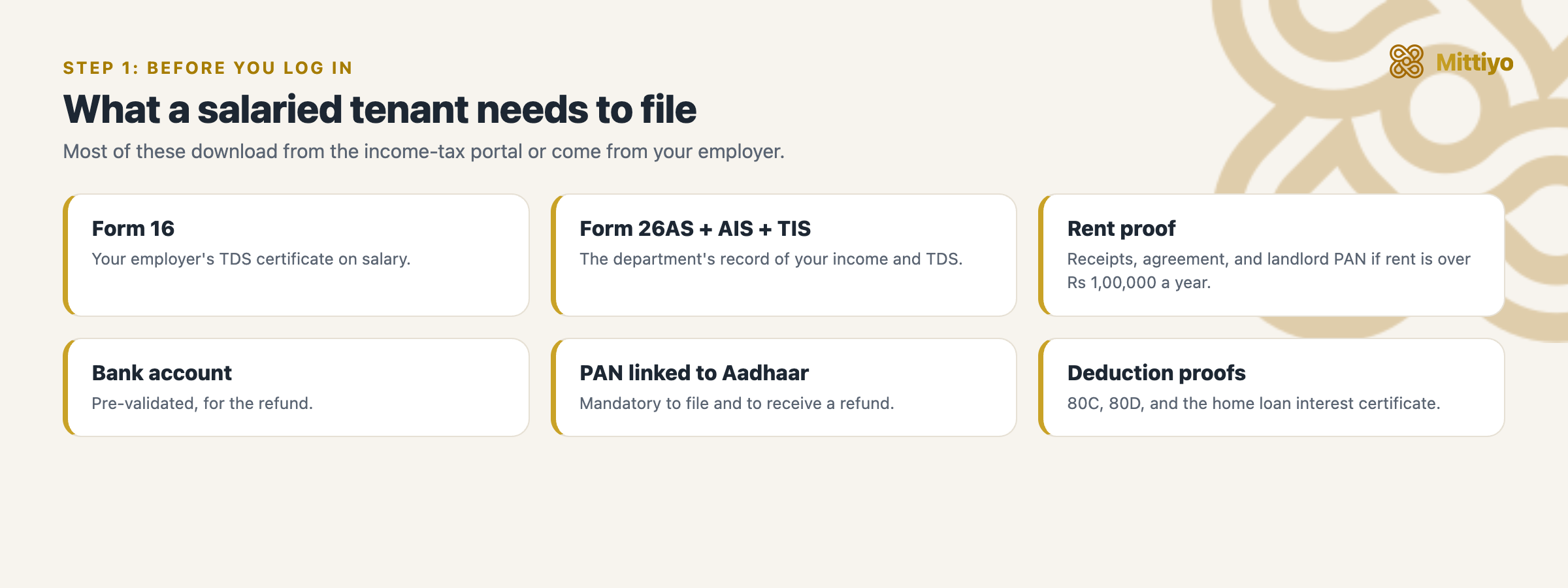

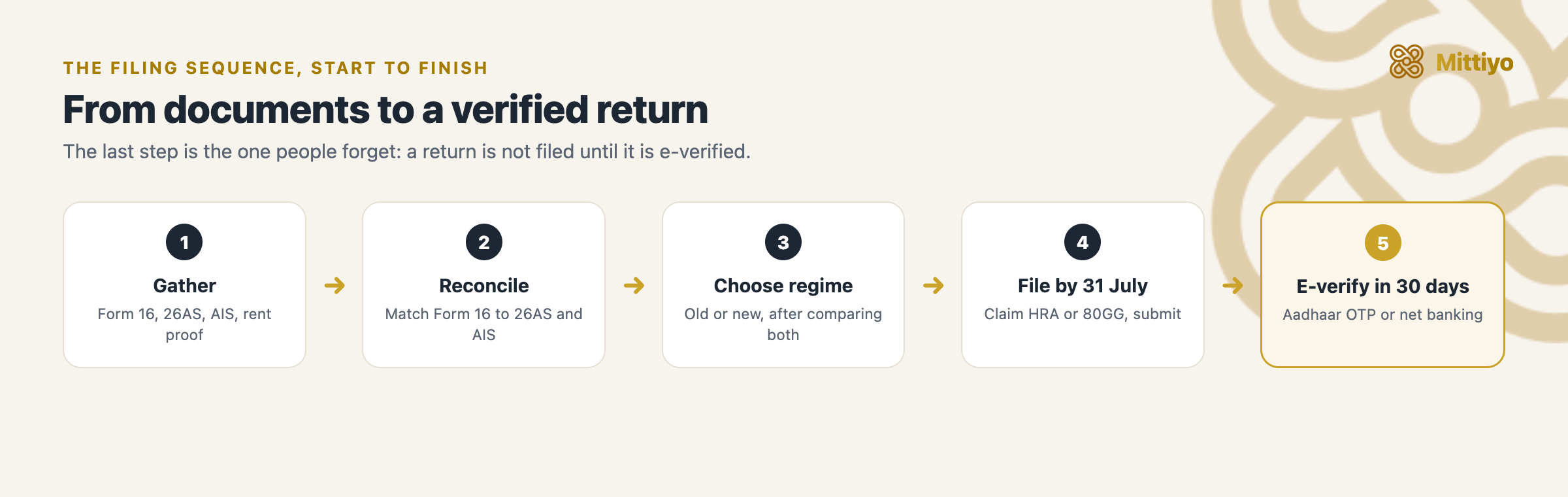

Step 1: Gather your documents

Collect these before you log in. Most are downloadable from the income-tax portal or your employer.

Collect these before you log in. Most are downloadable from the income-tax portal or your employer.

- Form 16 from your employer (the TDS certificate on your salary).

- Form 26AS and the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS), all from the income-tax e-filing portal.

- Rent proof if you claim HRA: rent receipts, the rent agreement, and the landlord’s PAN if your annual rent exceeds Rs 1,00,000.

- Bank account details (pre-validated, for the refund).

- PAN linked with Aadhaar.

- Deduction proofs: 80C investments, 80D health insurance, home loan interest certificate, and so on.

Step 2: Reconcile Form 16 with 26AS and AIS

Before you enter a single figure, compare your Form 16 against Form 26AS and the AIS. These are the department’s own record of your income and the tax deducted on it. If your return does not match, the mismatch can trigger an automated notice or stall your refund.

Check that your salary, the TDS on it, your bank interest, and any other income line up across all three. If the AIS shows something that is wrong or does not belong to you, submit feedback on the portal rather than ignoring it.

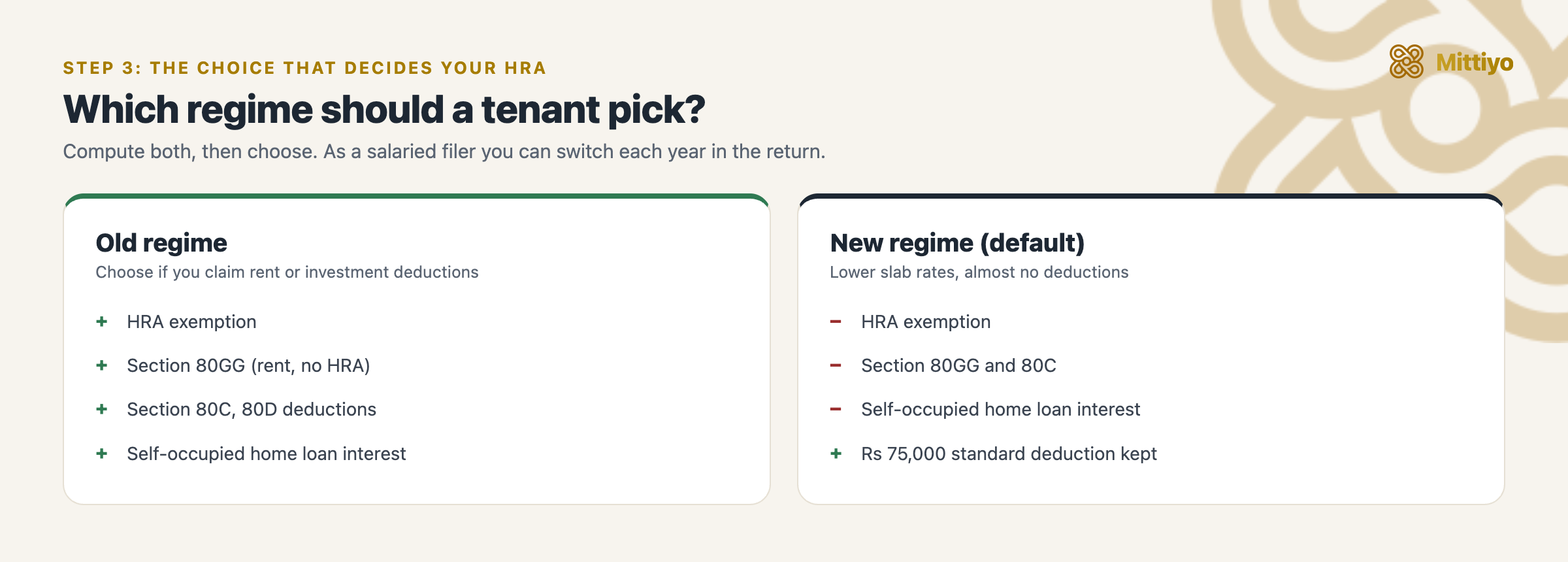

Step 3: Choose your regime (this is where HRA is won or lost)

The new regime is the default. For a tenant claiming HRA, that default is usually the wrong choice.

The new regime is the default. For a tenant claiming HRA, that default is usually the wrong choice.

This is the step that matters most for a tenant. The new regime is the default, and under it you cannot claim HRA, Section 80C, Section 80GG, or self-occupied home loan interest. The old regime keeps all of them but has higher slab rates.

As a salaried taxpayer you can choose the old regime directly in your return, and you can switch each year. The right move is to compute your tax both ways, old regime with your rent and investment deductions versus new regime with its lower rates and Rs 75,000 standard deduction, and pick whichever leaves you paying less. Do not let the default decide for you.

Why “old regime keeps HRA” does not always mean “old regime is cheaper”

This is the part that trips people up. Keeping a deduction is not the same as paying less tax. Because the new regime now gives a Section 87A rebate up to Rs 12,00,000 of income, plus a Rs 75,000 standard deduction, it often beats the old regime even for someone claiming HRA.

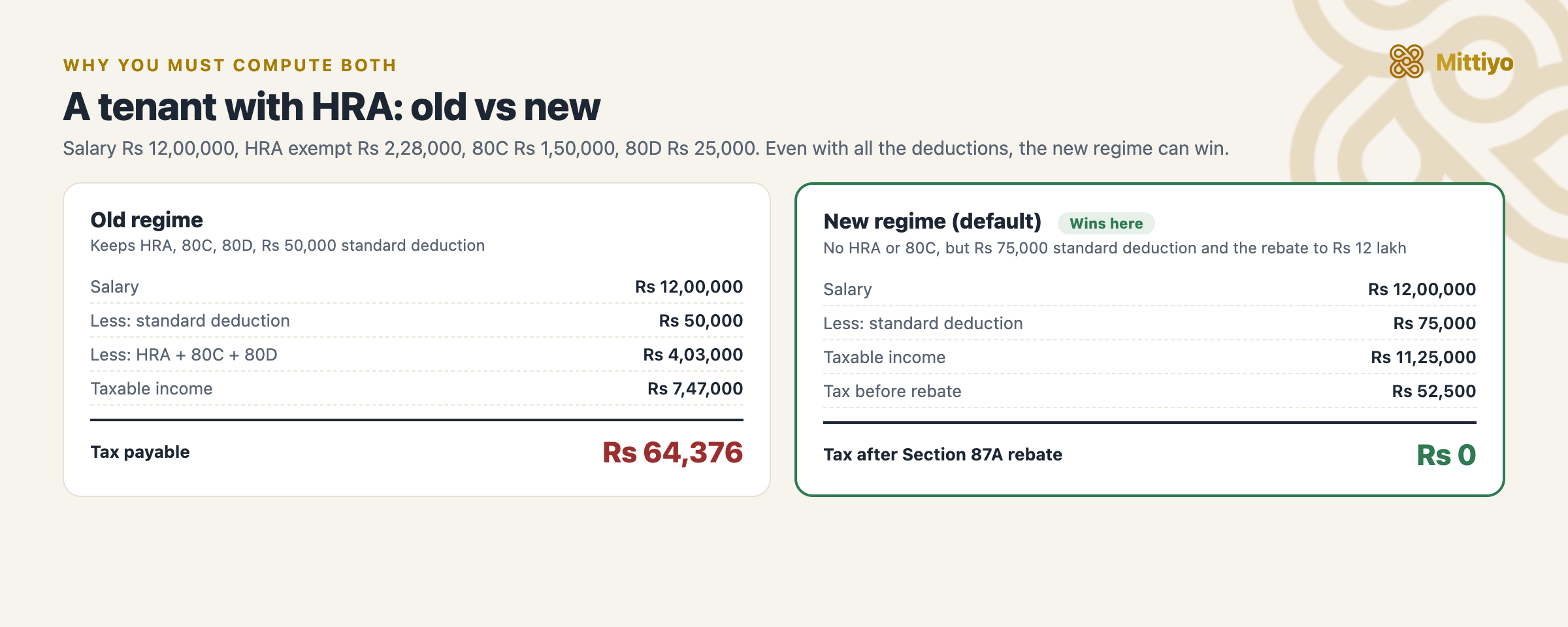

Same person, both regimes. The deductions survive under the old regime, but the new regime still wins here.

Same person, both regimes. The deductions survive under the old regime, but the new regime still wins here.

Take a tenant earning Rs 12,00,000 with Rs 2,28,000 of HRA exempt, Rs 1,50,000 of 80C, and Rs 25,000 of 80D. Under the old regime their taxable income works out to about Rs 7,47,000 and the tax to roughly Rs 64,400. Under the new regime the taxable income is Rs 11,25,000, which falls within the Section 87A rebate ceiling, so the tax is Rs 0. Despite losing every rent deduction, the new regime is cheaper here by about Rs 64,000.

The lesson is not “always pick new”. At higher incomes, or with very large deductions, the old regime can pull ahead. The lesson is that you cannot tell which wins by intuition: run both and compare before you choose.

Step 4: Claim your rent-related benefits

If you go with the old regime, make sure you actually claim what you are entitled to:

- HRA exemption if your salary includes an HRA component, backed by rent receipts.

- Section 80GG if you pay rent but your salary has no HRA component.

- If you also have a home loan, see HRA and home loan in the same year and the Section 24(b) interest deduction.

Only one of HRA and 80GG applies to you: HRA if you receive it, 80GG if you do not.

Step 5: Pick the right ITR form

For most salaried tenants, ITR-1 (Sahaj) is the right form: a resident individual with total income up to Rs 50,00,000 from salary or pension, one house property, and ordinary other-source income such as interest.

Use ITR-2 instead if you have more than one house property, capital gains beyond the small permitted limit, foreign income or assets, or you are a company director. The portal will often pre-fill and suggest the form, but the responsibility to pick correctly is yours.

Step 6: File, then e-verify within 30 days

Filing is not complete until you e-verify. You have 30 days.

Filing is not complete until you e-verify. You have 30 days.

Submit the return on the portal, then e-verify within 30 days. Until you verify, the return is treated as not filed, which can mean a late fee and lost benefits even though you hit submit on time. The fastest verification methods are Aadhaar OTP, net banking, or a pre-validated bank account. Once verified, your filing is done and the refund (if any) is processed.

After you file: refunds, and fixing mistakes

Refunds. Once your return is filed and e-verified, the department processes it and credits any refund to your pre-validated bank account, usually within a few weeks, though it can take longer in some cases. Track it under “View Filed Returns” or the refund-status tool on the portal. The most common cause of a stuck refund is a bank account that is not pre-validated, or whose name does not match your PAN.

Made a mistake? If you spot an error after filing, you do not start over. You file a revised return under Section 139(5), allowed until the end of the assessment year (or before your return is assessed, whichever comes first). The revised return simply replaces the original.

Missed the deadline? You can still file a belated return under Section 139(4), with the Section 234F late fee, up to the same year-end cut-off. And if you later realise you under-reported income, an updated return (ITR-U) under Section 139(8A) lets you correct it within an extended window, on payment of additional tax. None of these is as good as filing correctly and on time, but none is a dead end either.

The one-glance checklist

- Form 16, Form 26AS, AIS, and TIS downloaded

- Form 16 reconciled with 26AS and AIS (no mismatches)

- Rent receipts, agreement, and landlord PAN (if rent over Rs 1,00,000) ready

- Tax computed under both regimes; lower one chosen

- HRA or 80GG claimed correctly (whichever applies)

- Correct ITR form (ITR-1 for most salaried tenants)

- Bank account pre-validated for the refund

- Return filed by 31 July 2026

- Return e-verified within 30 days

Key takeaways

- The deadline for AY 2026-27 is 31 July 2026 for salaried filers; missing it means a Section 234F late fee and interest.

- Reconcile Form 16 with 26AS and AIS before filing to avoid notices.

- The new regime is the default and removes HRA. Choose the old regime if you need your rent deductions, after comparing both.

- Filing is not done until you e-verify within 30 days.

Moving to a new rental this year?

Your HRA claim and your peace of mind both start with the right home. Before you sign, see what residents say a building actually rents for, the deposit, the society, and the water and power reality, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: HRA exemption for salaried tenants · Section 80GG · Rent receipts for tax · HRA and home loan together

References

- Income tax e-filing portal (filing the return, AIS, Form 26AS, and e-verification)

- Income-tax Act, 1961, Section 139 (return of income and due dates), Section 234F (fee for default in filing), and Sections 234A to 234C (interest)

- Threshold limits under the Income-tax Act, Income Tax Department