Owning property in India while living abroad creates a unique set of legal, tax, and operational challenges. For Non-Resident Indians (NRIs), renting out Indian property generates income and ensures upkeep during their absence, but the regulatory framework is substantially more complex than what resident landlords face. This guide covers every significant aspect, from the tax structure and TDS mechanics to FEMA compliance, Power of Attorney requirements, rental agreement drafting, and the practicalities of managing property from thousands of kilometers away.

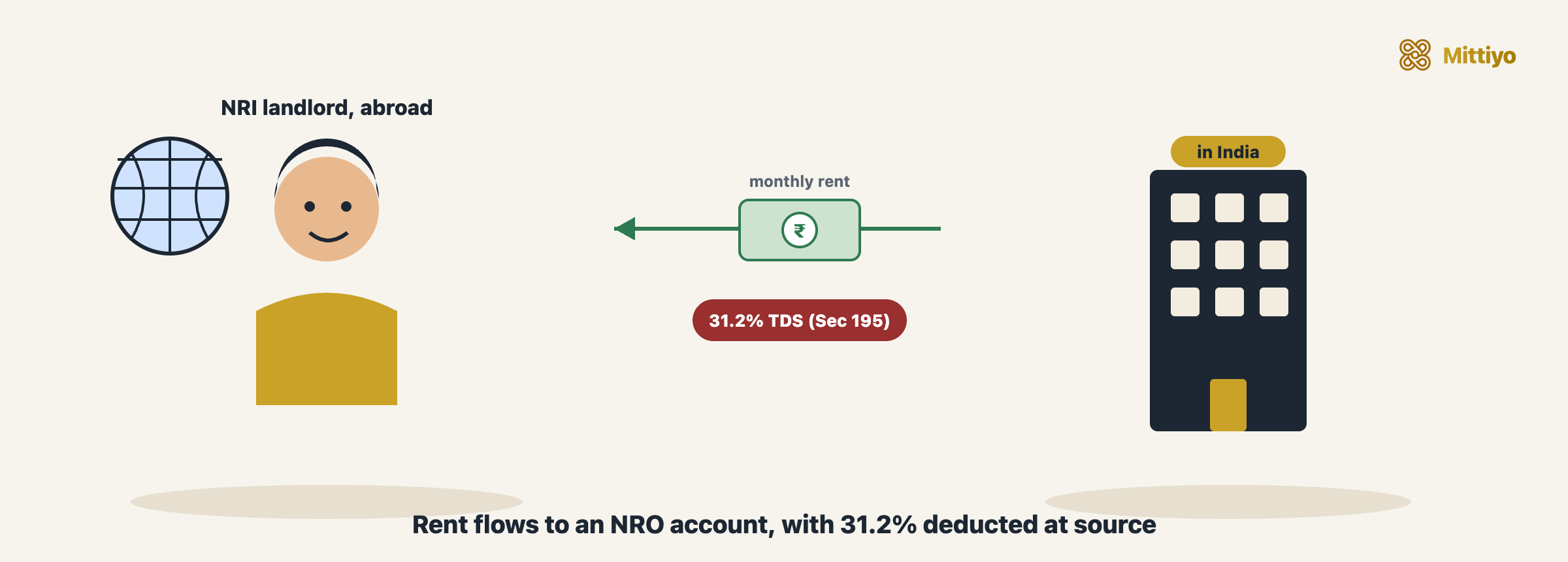

The one fact that surprises almost everyone: rent paid to an NRI attracts TDS of about 31.2% from the very first rupee, with no Rs 50,000 threshold, and the legal burden to deduct and deposit it sits on the tenant. Get that one mechanism right (ideally with a Section 197 lower-TDS certificate) and most of the friction disappears. The rest of this guide builds out from there.

Defining NRI Status: Why It Matters for Property Rental

Before examining the specific rules, it is important to understand who qualifies as an NRI, because NRI status triggers a fundamentally different tax and regulatory regime.

Income Tax Act Definition

Under Section 6 of the Income Tax Act, 1961, an individual is a “resident” in India if they satisfy either of two conditions:

- They are in India for 182 days or more during the relevant financial year, or

- They are in India for 60 days or more during the relevant financial year AND 365 days or more during the four years preceding the relevant financial year

Any individual who does not satisfy either condition is a “non-resident” for income tax purposes.

FEMA Definition

Under the Foreign Exchange Management Act, 1999, a “person resident outside India” is defined separately (Section 2(w)). The FEMA definition is based on intention and purpose of stay, not a mechanical day count. For practical purposes, most NRIs are non-resident under both the Income Tax Act and FEMA, but the definitions can diverge in edge cases, particularly for individuals who travel frequently between India and abroad.

Why the Distinction Matters

NRI status affects:

- The TDS rate on rental income (31.2% vs. 2% for residents)

- The obligation to file Indian income tax returns

- The type of bank accounts that can receive rental income

- The ability to repatriate rental income abroad

- The requirement for FEMA compliance in cross-border financial flows

Tax Framework for NRI Rental Income

How Rental Income Is Computed

NRI rental income from property in India is taxable under the head “Income from House Property” in the Indian income tax return. The computation follows the same structure as for resident landlords:

| Component | Calculation |

|---|---|

| Gross Annual Value (GAV) | Higher of actual rent received/receivable or fair market rent |

| Less: Municipal taxes | Actual municipal taxes paid by the NRI landlord during the year |

| = Net Annual Value (NAV) | GAV minus municipal taxes |

| Less: Standard deduction | 30% of NAV (flat deduction, no proof of expenses needed) |

| Less: Interest on housing loan | Actual interest paid during the year (no cap for let-out property) |

| = Taxable income from house property | Added to NRI’s total Indian income |

The 30% standard deduction is a significant benefit. It is available regardless of actual repair and maintenance expenses. An NRI landlord receiving Rs 40,000 per month in rent (Rs 4,80,000 annually) would receive a standard deduction of Rs 1,44,000, reducing taxable rental income to Rs 3,36,000 (before interest deduction, if any).

Tax Rates for NRIs (FY 2025-26)

NRIs can choose between the old and new tax regimes. Under the new regime (which is the default unless the NRI opts out):

| Taxable Income Slab | Tax Rate |

|---|---|

| Up to Rs 4,00,000 | Nil |

| Rs 4,00,001, Rs 8,00,000 | 5% |

| Rs 8,00,001, Rs 12,00,000 | 10% |

| Rs 12,00,001, Rs 16,00,000 | 15% |

| Rs 16,00,001, Rs 20,00,000 | 20% |

| Rs 20,00,001, Rs 24,00,000 | 25% |

| Above Rs 24,00,000 | 30% |

Plus surcharge (if applicable) and 4% health and education cess on total tax.

Under the old regime, tax rates are higher (up to 30% above Rs 10,00,000) but various deductions under Chapter VI-A (80C, 80D, etc.) are available. NRIs whose only Indian income is rental income often find the new regime more beneficial, particularly if rental income is modest.

Important Distinction: NRIs Cannot Claim Section 87A Rebate

The Section 87A rebate (which effectively makes income up to Rs 12,00,000 tax-free for residents under the new regime) is not available to NRIs. This is a frequently misunderstood point. Even if an NRI’s total Indian income (including rental income) is below Rs 12,00,000, they will still owe tax at the applicable slab rates without the rebate.

TDS on Rent Paid to NRI Landlords: Section 195

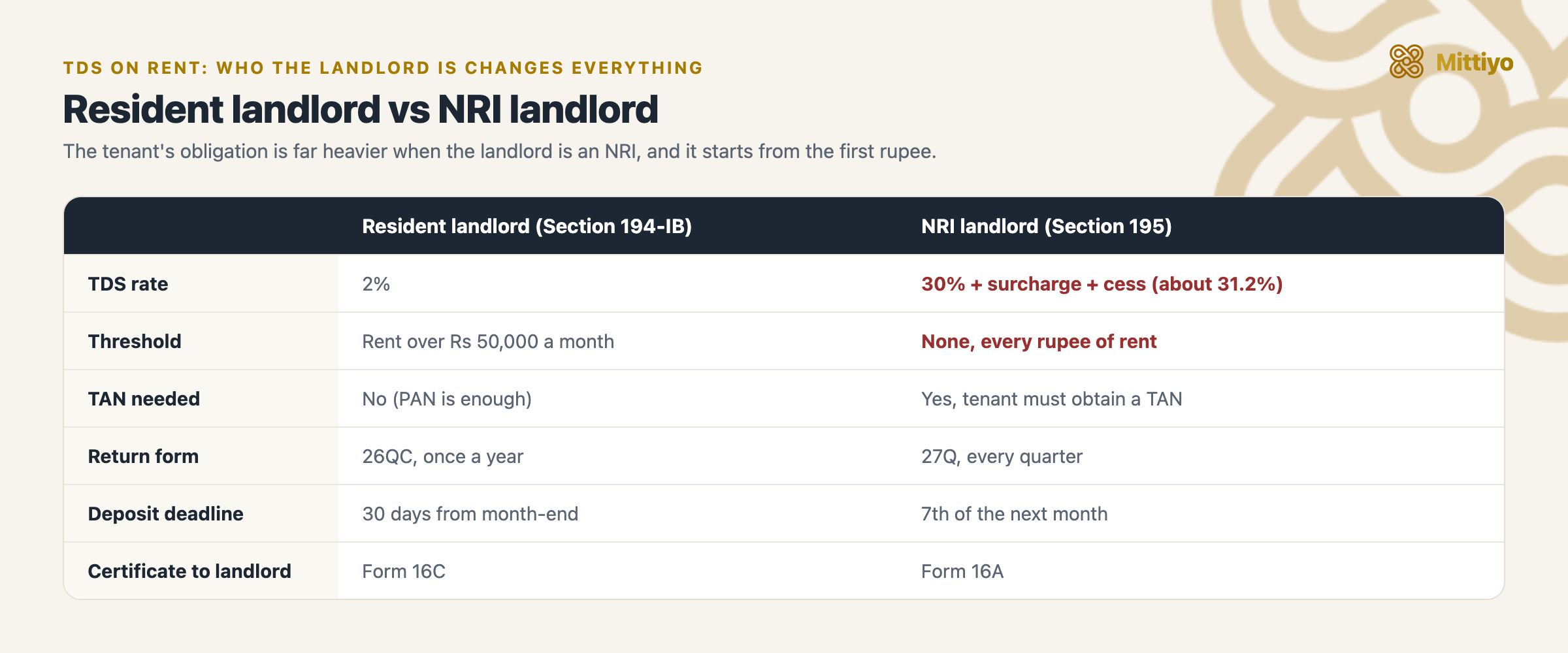

The TDS regime for NRI landlords is fundamentally different from, and significantly more onerous than, the regime for resident landlords. This section is critical for both NRI landlords and their tenants to understand.

The Core Difference

The tenant’s TDS burden is far heavier, and threshold-free, when the landlord is an NRI.

The tenant’s TDS burden is far heavier, and threshold-free, when the landlord is an NRI.

| Aspect | Resident Landlord (Section 194-IB) | NRI Landlord (Section 195) |

|---|---|---|

| TDS rate | 2% | 30% + surcharge + cess (~31.2%) |

| Threshold | Rs 50,000/month rent | No threshold, all amounts |

| TAN required | No (tenant uses PAN) | Yes (tenant must obtain TAN) |

| Return form | Form 26QC (quarterly) | Form 27Q (quarterly) |

| TDS certificate | Form 16C | Form 16A |

| Deposit deadline | 30 days from month-end | 7th of the following month |

The Practical Impact

Consider a tenant paying Rs 40,000 per month to an NRI landlord. Under Section 195:

- TDS at 31.2%: Rs 12,480 per month

- Net rent received by NRI: Rs 27,520 per month

- Annual TDS: Rs 1,49,760

The same rent paid to a resident landlord would attract no TDS at all (since it is below the Rs 50,000/month threshold under Section 194-IB).

This dramatic difference often surprises tenants. Many are unaware of their TDS obligations when renting from an NRI, and NRI landlords frequently fail to inform tenants of their non-resident status. Non-compliance exposes the tenant to interest (at 1% per month under Section 201(1A)) and penalties.

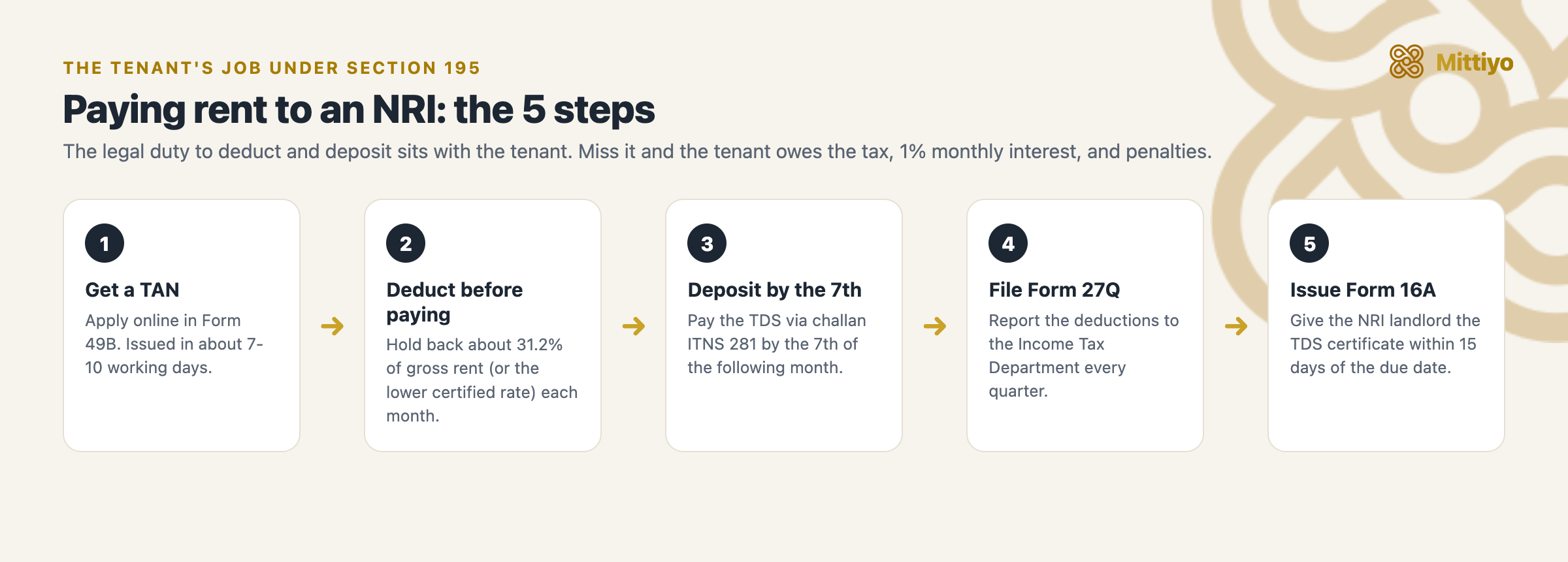

Tenant’s Compliance Process

The tenant’s Section 195 compliance, from TAN to TDS certificate.

The tenant’s Section 195 compliance, from TAN to TDS certificate.

A tenant renting from an NRI landlord must follow this process:

Step 1: Obtain TAN. Apply for a Tax Deduction and Collection Account Number online through the NSDL/Protean portal (Form 49B). TAN is typically issued within 7-10 working days.

Step 2: Deduct TDS before paying rent. Each month, deduct 31.2% (or the rate specified in the lower TDS certificate, if obtained) from the gross rent before transferring the balance to the NRI’s account.

Step 3: Deposit TDS with the government. Using challan ITNS 281, deposit the TDS amount by the 7th of the month following the month in which TDS was deducted. For March, the deadline is April 30.

Step 4: File quarterly returns. File Form 27Q with the Income Tax Department each quarter, reporting all TDS deductions made during the quarter.

Step 5: Issue TDS certificate. Issue Form 16A to the NRI landlord within 15 days of the due date for filing Form 27Q.

Lower TDS Certificate: Section 197

The 31.2% TDS rate often results in excess tax deduction, particularly when the NRI’s total Indian income falls within lower tax slabs. To avoid this, the NRI landlord can apply to the Assessing Officer (the Income Tax Officer having jurisdiction over the property) under Section 197 for a certificate authorizing TDS at a lower rate or nil rate.

When to apply: If the NRI’s total Indian income (after deductions) would result in a tax liability significantly lower than 31.2% of rental income. For example, if annual rental income is Rs 6,00,000 and the NRI has no other Indian income, the taxable income after the 30% standard deduction is about Rs 4,20,000, on which new-regime tax works out to roughly Rs 1,000 plus cess. TDS at 31.2% on the gross rent, however, would be Rs 1,87,200, vastly more than the actual liability.

How to apply: File Form 13 with the Assessing Officer, along with:

- Estimated income statement for the financial year

- Details of tax already paid or deducted

- Copy of the rental agreement

- Previous year’s income tax return

Timeline: The certificate is typically issued within 30 days. It is valid for the financial year specified and must be furnished to the tenant, who then deducts TDS at the certified lower rate.

What the certificate saves, in numbers

Suppose an NRI’s only Indian income is rent of Rs 6,00,000 a year. After the 30% standard deduction, taxable income is about Rs 4,20,000, on which new-regime tax is roughly Rs 1,000 plus cess. Without a lower certificate, the tenant must still deduct 31.2% of the gross rent, that is Rs 1,87,200, and deposit it. The NRI then files a return and claims a refund of almost the whole amount, money locked with the government for months. With a Section 197 certificate, the tenant deducts close to the real liability instead, and the cash stays with the landlord. For an NRI managing property from abroad, that cash-flow difference is the single biggest reason to apply.

Power of Attorney: Managing Property from Abroad

Since NRI landlords cannot be physically present to manage day-to-day property matters, a Power of Attorney (POA) is an essential legal instrument.

Types of POA

| Type | Scope | Risk Level | Recommended |

|---|---|---|---|

| General Power of Attorney (GPA) | Broad authority over all financial and legal matters | High | No |

| Special Power of Attorney (SPA) | Limited to specific acts related to a specific property | Low | Yes |

A Special Power of Attorney is strongly recommended. It should be drafted to authorize only the specific acts necessary for property management, limiting the POA holder’s authority and reducing the risk of misuse.

What the POA Should Authorize

A well-drafted SPA for rental property management should specifically authorize:

- Tenant management: Finding, screening, and selecting tenants; executing rental agreements; collecting rent and issuing receipts; initiating eviction proceedings if necessary

- Financial management: Collecting rent and depositing into the NRI’s NRO account; paying property taxes, utility bills, and maintenance charges; managing the security deposit

- Property maintenance: Arranging routine maintenance and emergency repairs within a specified budget limit; engaging contractors and service providers

- Legal and administrative matters: Appearing before the Sub-Registrar for agreement registration; representing the NRI before the apartment association, BBMP, BESCOM, BWSSB, and other authorities; filing police complaints if necessary

- Dispute handling: Representing the NRI in rent controller proceedings, mediation, and minor disputes (major litigation should typically require separate authorization or the NRI’s direct involvement)

Execution of POA Abroad

The process for executing a POA outside India involves several steps:

Step 1: Drafting. Engage an Indian lawyer to draft the POA document. The language must be precise about the powers granted and the property to which they relate. Include the property’s complete address, survey number, and registration details.

Step 2: Notarization. Sign the POA before a Notary Public in the country of residence. The notary verifies the identity of the person signing.

Step 3: Apostille or Authentication.

- If the country is a member of the Hague Apostille Convention (most Western countries, Japan, Australia, etc.), get the POA apostilled by the designated competent authority

- If the country is not a Hague Convention member, get the POA authenticated by the Indian embassy or consulate

Step 4: Send to India. Send the original POA document to the POA holder in India via secure courier.

Step 5: Adjudication in India. The POA holder may need to present the POA before the Sub-Registrar’s office in India and pay the applicable stamp duty. Stamp duty on a POA varies by state. It is governed by the relevant State Stamp Act, or by the Indian Stamp Act, 1899 where the state has not enacted its own schedule, so confirm the current rate for the state where the property is located.

Step 6: Registration (if required). If the POA authorizes acts related to immovable property (which rental management does), registration under the Registration Act, 1908 may be advisable, though registration of POA is not mandatory in all cases for rental management activities.

Important Limitations

- A POA holder cannot sell the property unless the POA specifically and explicitly authorizes sale (and even then, sale by POA is viewed with scrutiny by courts and registrars)

- A POA can be revoked by the NRI at any time by executing a revocation deed

- The POA becomes invalid upon the death of the NRI (principal)

- A POA does not transfer ownership, the NRI remains the legal owner

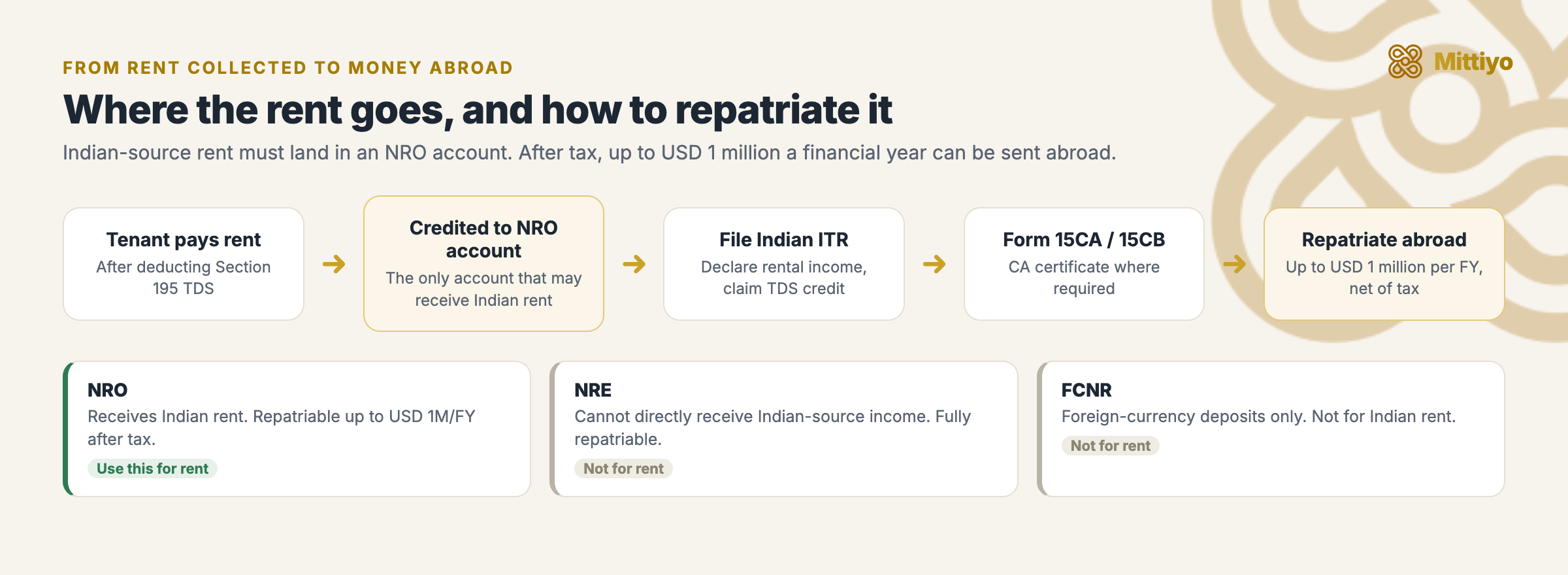

FEMA Compliance and Income Repatriation

The Foreign Exchange Management Act, 1999 governs cross-border financial flows. NRI landlords must ensure FEMA compliance when receiving rental income in India and repatriating it abroad.

Rent must land in an NRO account; up to USD 1 million a financial year can be repatriated after tax.

Rent must land in an NRO account; up to USD 1 million a financial year can be repatriated after tax.

Bank Account Structure

| Account Type | Can Receive Rent | Repatriation | Currency |

|---|---|---|---|

| NRO (Non-Resident Ordinary) | Yes | Up to USD 1 million per FY (after tax) | INR |

| NRE (Non-Resident External) | No (cannot receive Indian-source income directly) | Fully repatriable | INR (freely convertible) |

| FCNR (Foreign Currency Non-Resident) | No | Fully repatriable | Foreign currency |

Rental income must be credited to the NRI’s NRO account in India. It cannot be directly credited to an NRE or FCNR account.

Repatriation Process

After paying taxes on rental income, the NRI can repatriate funds from the NRO account to their foreign account. The repatriation limit is USD 1 million per financial year (net of applicable taxes). The process requires:

Step 1: Tax compliance. File the Indian income tax return declaring rental income and all other Indian-source income.

Step 2: Form 15CA/15CB certification.

- Form 15CB: A certificate from a practicing Chartered Accountant (CA) in India certifying that the remittance is in compliance with the Income Tax Act and that applicable taxes have been paid. The CA verifies the source of funds, tax liability, and TDS credit.

- Form 15CA: An online undertaking filed by the remitter (NRI) on the Income Tax Department’s e-filing portal before making the remittance. Part A of Form 15CA (for remittances up to Rs 5 lakh per transaction) does not require a CA certificate. Part C (for remittances covered by a CA certificate) must be accompanied by Form 15CB.

Step 3: Bank processing. Submit the Form 15CA acknowledgment and Form 15CB certificate (if applicable) to the bank. The bank processes the outward remittance after verifying compliance.

FEMA Penalties

Non-compliance with FEMA provisions can result in penalties up to three times the amount involved in the contravention, or Rs 2,00,000 where the amount is not quantifiable, with continuing penalties of Rs 5,000 per day beyond the first day of contravention. The Enforcement Directorate (ED) is the enforcement authority.

Rental Agreement: Special Considerations for NRI Landlords

Essential Clauses for NRI Rental Agreements

Beyond the standard clauses in any rental agreement, NRI landlords should include:

POA holder identification: Full name, address, and contact details of the POA holder, with explicit statement that the POA holder is authorized to execute and manage the agreement on behalf of the NRI landlord.

NRI status disclosure: A clause disclosing the landlord’s NRI status and the tenant’s corresponding TDS obligations under Section 195. This protects the landlord from a tenant’s claim of ignorance about the higher TDS rate.

Rent payment mechanics: Specify that rent is to be paid via bank transfer to the NRI’s NRO account (provide account details). State that the tenant must deduct TDS at the applicable rate before payment.

TDS compliance clause: The tenant’s obligation to obtain TAN, deduct TDS at 31.2% (or the rate in the lower TDS certificate), deposit TDS within the prescribed timeline, file Form 27Q quarterly, and issue Form 16A. Include a provision that the landlord will provide the lower TDS certificate (if obtained) to the tenant.

Communication protocol: Primary contact (POA holder in India, with phone number and email). Secondary contact (NRI landlord, with international phone number, email, and preferred communication times given the time zone difference).

Emergency maintenance authorization: Authorize the POA holder to arrange emergency repairs up to a specified amount (e.g., Rs 25,000 per incident) without prior approval. For amounts above this threshold, the NRI landlord’s approval is required (with a reasonable response time, considering time zone differences).

Dispute resolution: Specify jurisdiction (typically the city where the property is located). Include a mediation clause. Designate the POA holder as the landlord’s representative for all proceedings in the first instance.

Registration Requirements

Under Section 17(1)(d) of the Registration Act, 1908, leases of immovable property for a term exceeding one year must be registered. Most residential rental agreements across India are structured as 11-month agreements to avoid mandatory registration. For NRI landlords, this is particularly relevant because:

- An unregistered agreement exceeding 12 months cannot be admitted as evidence in court (Section 49 of the Registration Act)

- The POA holder can register the agreement on behalf of the NRI at the Sub-Registrar’s office

- Registration provides stronger legal protection for the NRI landlord, who cannot easily appear in person for dispute resolution

Double Taxation Avoidance

India has signed Double Taxation Avoidance Agreements (DTAAs) with over 90 countries. DTAAs prevent the same income from being taxed twice, once in India (source country) and once in the country of residence.

How DTAAs Apply to Rental Income

Under most DTAAs, rental income from immovable property may be taxed in the country where the property is situated (India, in this case). The NRI’s country of residence typically provides relief by either:

Tax credit method: The country of residence allows the NRI to claim a credit for Indian taxes paid against their domestic tax liability on the same income. This is the more common approach (used by the US, UK, Australia, Canada, and most other countries with which India has DTAAs).

Exemption method: The country of residence exempts the Indian rental income from domestic taxation entirely. This is less common.

Practical Steps for DTAA Benefits

Step 1: Obtain a Tax Residency Certificate (TRC) from the tax authority of the country of residence. This proves that the NRI is a tax resident of that country and entitled to DTAA benefits.

Step 2: File Form 10F with the Indian Income Tax Department, providing details required under the DTAA (such as the NRI’s status, period of residential status, and the purpose and nature of income).

Step 3: Declare Indian rental income in the foreign tax return filed in the country of residence.

Step 4: Claim foreign tax credit for Indian taxes paid (TDS deducted and any additional tax paid on the Indian return). The mechanism for claiming foreign tax credit varies by country, in the US, it is Form 1116; in the UK, it is claimed through the self-assessment return.

Country-Specific Considerations

| Country | DTAA Provision for Rental Income | Relief Method |

|---|---|---|

| USA | Article 6, Income from immovable property taxable in India | Tax credit (Form 1116) |

| UK | Article 6, Income from immovable property taxable in India | Tax credit (self-assessment) |

| Canada | Article 6, Income from immovable property taxable in India | Tax credit |

| Australia | Article 6, Income from immovable property taxable in India | Tax credit |

| UAE | No income tax in UAE, DTAA prevents India from taxing at higher rates | N/A (no UAE tax) |

| Singapore | Article 6, Income from immovable property taxable in India | Tax credit/exemption |

For NRIs in the UAE and other zero-tax jurisdictions, DTAA benefits are limited because there is no foreign tax liability against which to claim credit. The Indian tax on rental income is the only tax payable.

Common Challenges and Practical Solutions

Challenge 1: Tenant Unaware of NRI TDS Obligations

Many tenants are unfamiliar with Section 195 TDS requirements. They may resist the higher TDS deduction or simply fail to comply.

Solution: Disclose NRI status explicitly in the rental agreement. Include a detailed TDS clause. If possible, apply for a lower TDS certificate under Section 197 to reduce the burden on the tenant. Provide the tenant with clear, step-by-step instructions for TAN application and TDS deposit.

Challenge 2: Finding Reliable Tenants from Abroad

Screening tenants without being physically present is difficult. Reference checks, employment verification, and personal assessment are harder to conduct remotely.

Solution: Delegate tenant screening to the POA holder or a professional property management company. Establish clear screening criteria (employment verification, previous landlord references, police verification). Some property management firms offer comprehensive tenant screening and management packages.

Challenge 3: Maintenance Emergencies

Plumbing failures, electrical faults, and other emergencies require immediate response. Time zone differences can delay communication with the NRI landlord.

Solution: Authorize the POA holder with a maintenance budget and pre-approved vendor list. The rental agreement should empower the POA holder to arrange emergency repairs up to a specified amount. Establish a maintenance fund (e.g., Rs 50,000-1,00,000) held by the POA holder for immediate deployment.

Challenge 4: Rent Collection and Monitoring

Ensuring regular rent collection, TDS compliance, and proper accounting from abroad requires reliable systems.

Solution: Set up automated rent collection via standing instructions or NACH (National Automated Clearing House) mandates. The POA holder or a CA should monitor TDS deposits and file quarterly returns. Many NRIs engage a CA on a retainer basis for this purpose.

Challenge 5: Property Insurance

Properties left in the care of tenants and POA holders face risks, fire, water damage, natural disasters, tenant damage, that the NRI cannot monitor directly.

Solution: Obtain comprehensive property insurance covering fire, natural disasters, and structural damage. Some insurers offer specific products for rented properties. Ensure the insurance policy does not exclude coverage for tenant-occupied properties.

Challenge 6: Dispute Resolution from Abroad

If disputes arise with tenants, rent default, property damage, unauthorized subletting, the NRI cannot easily appear in person before the Rent Controller or civil court.

Solution: The POA holder can represent the NRI in rent controller proceedings and minor disputes. For significant litigation, engage a local lawyer. Include a detailed dispute resolution clause in the rental agreement, including arbitration provisions that can be conducted without the NRI’s physical presence.

Checklist for NRI Landlords

Before renting out property from abroad, ensure the following are in place:

| Item | Status |

|---|---|

| NRO account opened and operational | Required |

| TAN obtained (or tenant instructed to obtain TAN) | Required |

| Special Power of Attorney executed, apostilled/authenticated, and sent to India | Required |

| POA holder identified, briefed, and authorized | Required |

| Rental agreement drafted with NRI-specific clauses | Required |

| Chartered Accountant engaged for tax filing and TDS monitoring | Recommended |

| Lower TDS certificate (Section 197) application filed | Recommended |

| Property insurance obtained | Recommended |

| Maintenance fund established with POA holder | Recommended |

| DTAA compliance (TRC, Form 10F) arranged | Required (for claiming credit abroad) |

Renting out your Indian property from abroad?

Distance makes it harder to know what your building actually commands and how tenants rate the society, the water, and the upkeep you cannot see in person. know.place is a map of honest, building-level rental reviews across India, useful for pricing the rent right and keeping a remote read on your property.

Explore know.placeThis guide is general information, not personalised tax, legal, or FEMA advice; an NRI’s position depends on their country of residence and the applicable treaty, so confirm yours with a qualified chartered accountant or cross-border tax adviser.

Related guides: Rental income tax for landlords · TDS on rent (Section 194-IB) · Rent receipts for tax

References

- Income-tax Act, 1961, Sections 6, 194-IB, 195 and 197 (residence, TDS on rent, TDS on payments to non-residents, lower-TDS certificate)

- Foreign Exchange Management Act, 1999, Section 2(w), person resident outside India

- RBI Master Direction, Remittance of Assets (FED Master Direction No. 15/2015-16), repatriation from NRO accounts

- Registration Act, 1908, Sections 17 and 49, compulsory registration and effect of non-registration

- Powers-of-Attorney Act, 1882

- Indian Stamp Act, 1899 (POA stamp duty, read with the relevant State Stamp Act)

- India’s DTAA network, Income Tax Department, International Taxation

- Statutory forms (Form 15CA, 15CB, 10F, 13, 27Q) on the Income Tax e-filing portal, read with Rule 37BB, Income-tax Rules, 1962

- TAN application (Form 49B) and TDS certificates (TRACES)