For years the advice was simple: if you pay rent and have a few investments, the old tax regime is better. Budget 2025 broke that rule of thumb. The new regime now gives nil tax up to Rs 12,00,000 of taxable income and lower rates above it, which means a lot of people who “obviously” belonged in the old regime are now better off in the new one, even with HRA.

That does not make the new regime always right. For higher earners with a home loan and a full set of deductions, the old regime can still win by a comfortable margin. The point is that you can no longer guess. This guide lays out both regimes for FY 2025-26 (AY 2026-27), shows exactly where each one wins, and walks through worked numbers so you can see which side of the line you fall on.

One thing to hold onto before we start: the new regime is the default. If you file without choosing, you are taxed under it, and every old-regime deduction quietly disappears.

The two regimes, side by side

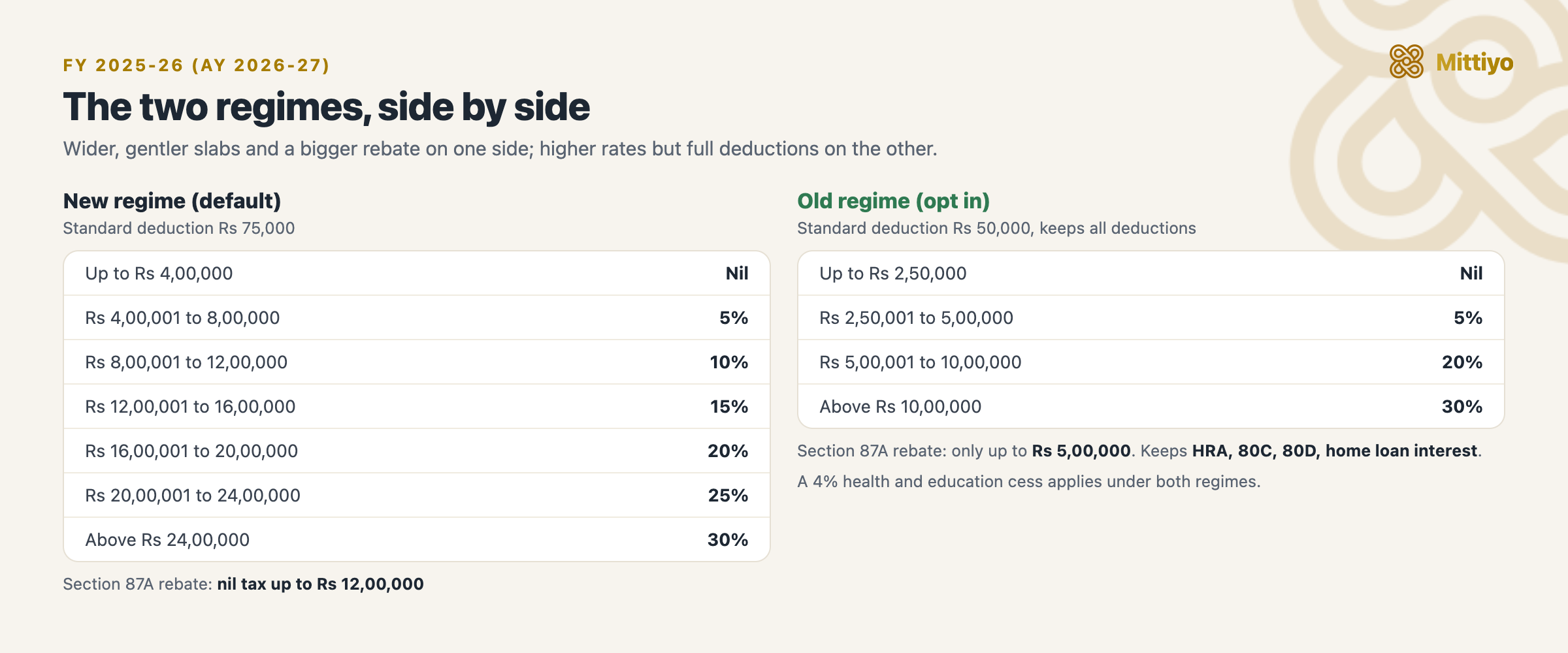

The new regime has wider, gentler slabs and a much bigger rebate; the old regime has higher rates but keeps the deductions.

The new regime has wider, gentler slabs and a much bigger rebate; the old regime has higher rates but keeps the deductions.

New regime (default), FY 2025-26:

| Taxable income | Rate |

|---|---|

| Up to Rs 4,00,000 | Nil |

| Rs 4,00,001 to Rs 8,00,000 | 5% |

| Rs 8,00,001 to Rs 12,00,000 | 10% |

| Rs 12,00,001 to Rs 16,00,000 | 15% |

| Rs 16,00,001 to Rs 20,00,000 | 20% |

| Rs 20,00,001 to Rs 24,00,000 | 25% |

| Above Rs 24,00,000 | 30% |

Standard deduction Rs 75,000. Section 87A rebate makes tax nil up to Rs 12,00,000 of taxable income.

Old regime, FY 2025-26:

| Taxable income | Rate |

|---|---|

| Up to Rs 2,50,000 | Nil |

| Rs 2,50,001 to Rs 5,00,000 | 5% |

| Rs 5,00,001 to Rs 10,00,000 | 20% |

| Above Rs 10,00,000 | 30% |

Standard deduction Rs 50,000. Section 87A rebate only up to Rs 5,00,000 of taxable income. A 4% health and education cess applies under both regimes.

What you give up, and what you keep

The new regime’s lower rates come at a price: almost every deduction goes away.

Available only in the old regime:

- HRA exemption (Section 10(13A)) and leave travel allowance

- Section 80C (EPF, PPF, ELSS, life insurance, principal repayment, tuition fees), up to Rs 1,50,000

- Section 80D health insurance

- Section 80GG (rent paid when you get no HRA)

- The extra Rs 50,000 NPS deduction under Section 80CCD(1B)

- Self-occupied home loan interest under Section 24(b), up to Rs 2,00,000

- Section 80E education loan interest, 80G donations, 80TTA/80TTB, and the rest

Still available in the new regime:

- The Rs 75,000 standard deduction on salary

- The employer’s NPS contribution under Section 80CCD(2), up to 14% of basic salary

- Interest on a let-out property under Section 24(b)

That short “kept” list is the whole trade. The new regime says: forget the paperwork, take lower rates and a big rebate. The old regime says: keep your deductions, but pay higher rates.

The new regime’s trump card: nil tax up to Rs 12 lakh

This is what changed the maths. Under the new regime, if your taxable income is up to Rs 12,00,000, the Section 87A rebate (up to Rs 60,000) wipes your tax out entirely. Add the Rs 75,000 standard deduction and a salary of about Rs 12,75,000 pays nothing.

Two important caveats:

- The rebate applies only under the new regime. The old regime’s 87A rebate stops at Rs 5,00,000 of income.

- It covers ordinary income, not special-rate income. Capital gains taxed at their own rate (for example equity gains under Section 112A) are taxed regardless, so a Rs 11 lakh salary plus Rs 2 lakh of equity gains is not fully tax-free.

Just above Rs 12,00,000, marginal relief ensures the extra tax never exceeds the extra income, so there is no cliff where earning one rupee more costs you thousands.

When the old regime still wins: the break-even

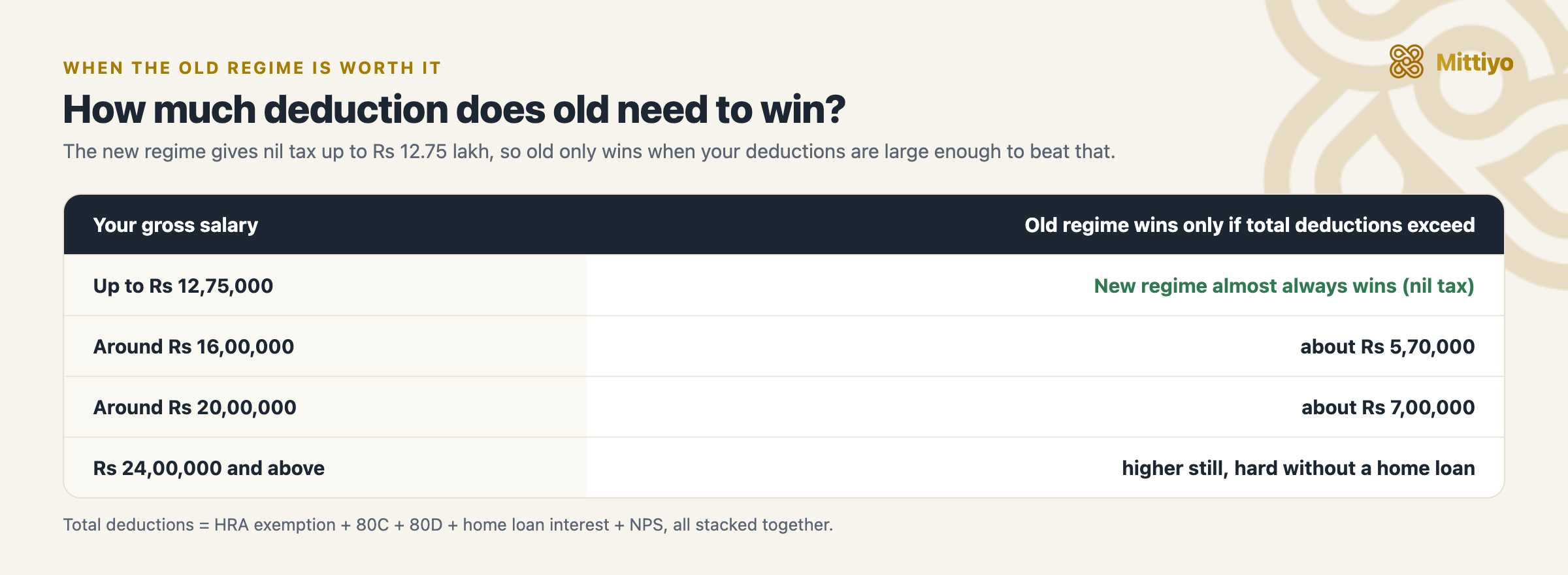

Because the new regime is so generous up to Rs 12,75,000, the old regime only beats it when your deductions are large enough to drag your old-regime taxable income down far below your new-regime one. The higher your income, the more deductions you need to make the old regime worthwhile.

The bar to clear rises with income. Most renters without a home loan never reach it.

The bar to clear rises with income. Most renters without a home loan never reach it.

| Gross salary | Old regime wins if total deductions exceed roughly |

|---|---|

| Up to Rs 12,75,000 | New regime almost always wins (nil tax) |

| Around Rs 16,00,000 | About Rs 5,70,000 of deductions |

| Around Rs 20,00,000 | About Rs 7,00,000 of deductions |

| Rs 24,00,000 and above | Higher still, hard without large home loan interest plus HRA |

“Total deductions” means everything stacked: HRA exemption, the full Rs 1,50,000 of 80C, Rs 25,000 to Rs 75,000 of 80D, up to Rs 2,00,000 of home loan interest, the Rs 50,000 NPS top-up, and so on. A salaried renter without a home loan usually cannot reach these thresholds, so the new regime tends to win. A renter with a home loan, full 80C, and health insurance, at a higher income, often clears the bar and should choose the old regime.

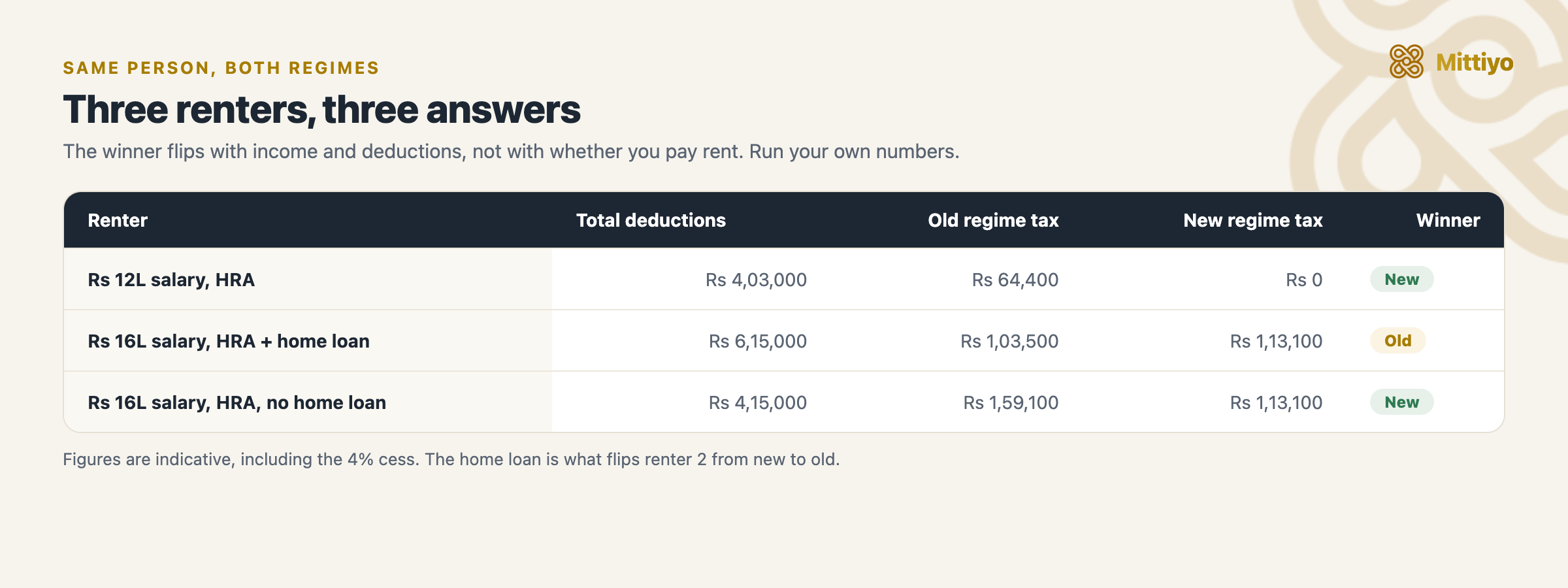

Worked examples

Same person, both regimes, at three incomes. The winner flips as income and deductions grow.

Same person, both regimes, at three incomes. The winner flips as income and deductions grow.

Example 1: Rs 12,00,000 salary, renter with HRA. Deductions: HRA exempt Rs 2,28,000, 80C Rs 1,50,000, 80D Rs 25,000. Old-regime taxable income is about Rs 7,47,000, tax about Rs 64,400. New-regime taxable income is Rs 11,25,000, which falls within the rebate, so tax is Rs 0. The new regime wins outright.

Example 2: Rs 16,00,000 salary, renter with HRA and a home loan. Deductions: HRA Rs 2,40,000, 80C Rs 1,50,000, 80D Rs 25,000, home loan interest Rs 2,00,000, total Rs 6,15,000. Old-regime taxable income about Rs 9,35,000, tax about Rs 1,03,500. New-regime taxable income Rs 15,25,000, tax about Rs 1,13,100. Here the old regime wins (narrowly), because the deductions cross the break-even.

Example 3: Rs 16,00,000 salary, renter with HRA but no home loan. Deductions: HRA Rs 2,40,000, 80C Rs 1,50,000, 80D Rs 25,000, total Rs 4,15,000, below the roughly Rs 5,70,000 break-even at this income. The new regime wins. The only difference from Example 2 is the home loan, and it is enough to flip the answer.

The lesson from the three: the result turns on how much you can deduct, not on whether you pay rent. Run your own numbers.

How to choose, and how to switch

- Salaried, no business income: choose the old regime directly in your return (ITR-1 or ITR-2). No special form is needed, and you can switch every year.

- Business or professional income: you must file Form 10-IEA before the return due date to opt for the old regime, and you can switch back to the new regime only once.

- Either way, the new regime is the default, so opting for the old regime is an active choice you make at filing. You can tell your employer your choice for TDS during the year, but the final regime is locked when you file your return by the due date.

Use the official calculator on the income-tax portal to compute both before you commit.

The mistake to avoid

The headline “income up to Rs 12 lakh is tax-free” has created two traps. First, that rebate is a new-regime benefit; people assume it applies in the old regime too, and it does not. Second, it covers ordinary income only, so taxpayers with capital gains wrongly expect those to be covered by the rebate. They are taxed at their special rate regardless.

The deeper mistake is treating “old regime keeps my HRA” as if it settles the question. Keeping a deduction is not the same as paying less tax. The only way to know is to compute both.

Key takeaways

- The new regime is the default and gives nil tax up to Rs 12,00,000 (about Rs 12,75,000 of salary), so it now wins for most people, including many renters with HRA.

- The old regime keeps HRA, 80C, 80D, NPS, and self-occupied home loan interest, and wins only when those deductions are large, roughly above Rs 5,70,000 at Rs 16 lakh income and Rs 7,00,000 at Rs 20 lakh.

- The Rs 12 lakh rebate does not apply in the old regime, nor to special-rate capital gains.

- Salaried filers switch freely each year; those with business income need Form 10-IEA and get one switch back.

- Do not guess. Compute both regimes on the official portal before you file.

Renting, and weighing your HRA claim?

Whether the old regime is worth it often hinges on your rent and HRA. Before you sign your next place, see what residents say a building actually rents for, the deposit, and the society, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: HRA exemption for salaried tenants · HRA and home loan in the same year · ITR filing checklist for salaried tenants · Section 80GG

References

- Income tax e-filing portal, slabs for AY 2026-27 (new and old regime rates, standard deduction, Section 87A rebate)

- Old regime vs new regime FAQs, Income Tax Department (choosing and switching, Form 10-IEA)

- Income-tax Act, 1961, Sections 115BAC (new regime), 87A (rebate), 10(13A) (HRA), 24(b), 80C, 80D, 80GG

- Union Budget 2025 income-tax changes, Press Information Bureau