Rent receipts are the primary documentary evidence required to claim House Rent Allowance (HRA) exemption under Section 10(13A) of the Income Tax Act, 1961. While generating a rent receipt may seem straightforward, the specific format requirements, revenue stamp rules, PAN obligations, and the interplay between physical and digital receipts create a landscape where small mistakes can jeopardize significant tax benefits.

For a tenant in Bengaluru paying Rs 25,000 per month, the HRA exemption can save Rs 37,000 to Rs 94,000 in annual income tax. An improperly documented rent receipt can cause this entire benefit to be disallowed during assessment.

One thing to confirm first: HRA exemption exists only under the old tax regime, and the new regime is now the default. If you have not actively opted for the old regime, rent receipts will not earn you an HRA exemption at all, so check your regime before you build the paper trail below.

The three numbers that trigger a compliance step. This guide covers every aspect of rent receipts - from the correct format through legal requirements, digital receipt validity, the relationship between receipts and bank records, employer submission processes, and the mistakes that most commonly trigger Income Tax department scrutiny.

The three numbers that trigger a compliance step. This guide covers every aspect of rent receipts - from the correct format through legal requirements, digital receipt validity, the relationship between receipts and bank records, employer submission processes, and the mistakes that most commonly trigger Income Tax department scrutiny.

The Legal Foundation: Why Rent Receipts Matter

Section 10(13A) and Rule 2A

HRA exemption under Section 10(13A) of the Income Tax Act, 1961, read with Rule 2A of the Income Tax Rules, 1962, requires the salaried individual to actually pay rent for residential accommodation. The rent receipt is the primary proof that rent was actually paid.

The Income Tax Act does not prescribe a specific format for rent receipts. However, CBDT (Central Board of Direct Taxes) circulars, employer practices, and assessment standards have established clear requirements for what a valid receipt must contain.

The Employer’s Role

Most employers act as the first checkpoint for HRA claims. Under Section 192 of the Income Tax Act, employers are required to deduct TDS on salary after accounting for exemptions and deductions claimed by the employee. The employer will allow the HRA exemption only if the employee submits satisfactory proof - and rent receipts are the cornerstone of this proof.

If the employer rejects the rent receipts (due to missing information, absent revenue stamps, or missing landlord PAN), the full HRA amount becomes taxable in that year. The employee would then need to claim the exemption when filing their income tax return, which invites closer scrutiny from the Assessing Officer.

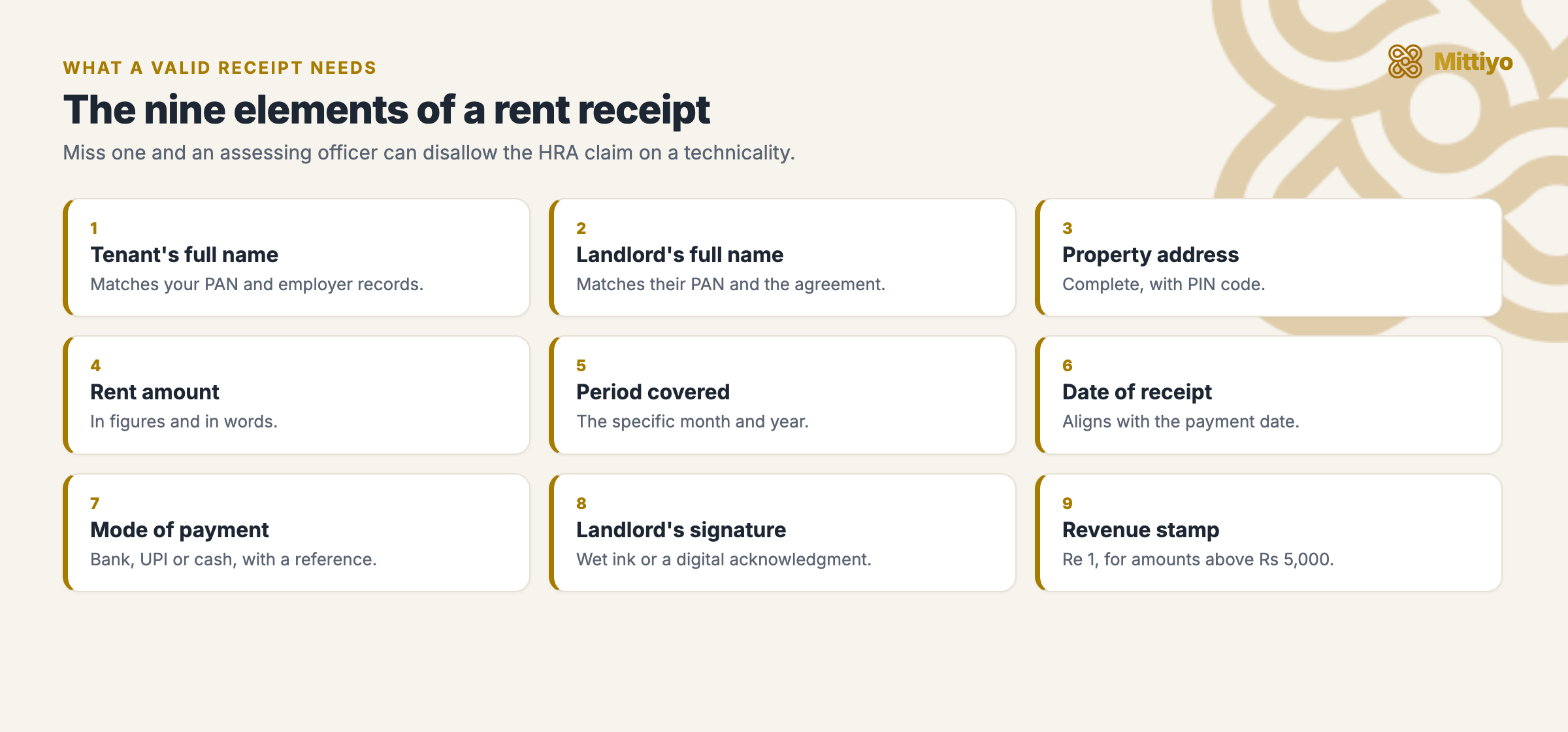

What a Valid Rent Receipt Must Contain

Every rent receipt - whether physical or digital - should include the following nine elements:

Everything a valid rent receipt must show.

Everything a valid rent receipt must show.

1. Tenant’s Full Name

The name must match your employer records and your PAN card. If your legal name differs from the name used at work (e.g., middle name included on PAN but not in employer records), clarify with your employer which name to use.

2. Landlord’s Full Name

The full legal name of the landlord - matching their PAN card and the rental agreement. If the property is jointly owned and the agreement is with multiple landlords, the receipt should be from the primary landlord (the one whose PAN is provided for HRA purposes).

3. Property Address

The complete address of the rented premises - including flat number, floor, building name, street, locality, city, and PIN code. This must match the address in the rental agreement and the address registered with your employer.

4. Rent Amount

Stated in both figures and words to prevent alteration. For example: “Rs. 25,000 (Rupees Twenty-Five Thousand only).” The amount must exactly match the rent specified in the rental agreement and the amount transferred via bank.

5. Period Covered

The specific month and year for which the receipt is issued. For example: “For the month of April 2025” or “For the period 1st April 2025 to 30th April 2025.” This establishes that the payment was for a specific rental period.

6. Date of Receipt

The date on which the landlord received the rent payment. This should align with the date of the bank transfer or payment.

7. Mode of Payment

Specify whether the payment was made by bank transfer (NEFT/IMPS/RTGS), UPI, cheque, demand draft, or cash. This detail links the receipt to the corresponding bank record.

8. Landlord’s Signature

The landlord must sign each receipt. For physical receipts, this is a wet signature. For digital receipts, a scanned signature, digital signature, or typed name with acknowledgment language (e.g., “I, [landlord name], acknowledge receipt of the above amount”) is accepted.

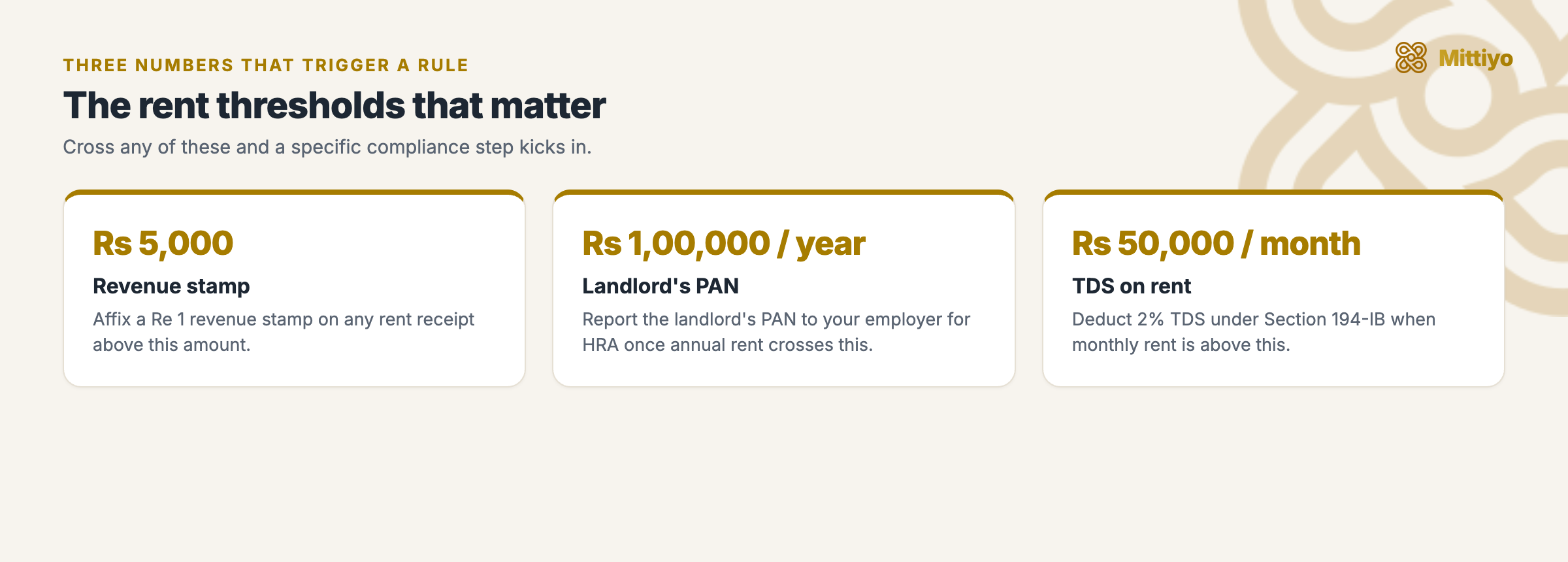

9. Revenue Stamp

For receipt amounts exceeding Rs 5,000, a revenue stamp of Re 1 must be affixed and cancelled. Discussed in detail below.

Revenue Stamp Rules: Complete Analysis

The Legal Requirement

The requirement for revenue stamps on receipts originates from the Indian Stamp Act, 1899 and relevant state stamp legislation. Under these provisions, any receipt for an amount exceeding Rs 5,000 requires a revenue stamp of Re 1.

How to Apply the Revenue Stamp

- Procure revenue stamps: Available at Indian Post offices (head post offices and major sub-post offices) and authorized stamp vendors. Cost: Re 1 per stamp.

- Affix the stamp: Paste the revenue stamp on the receipt near the landlord’s signature area.

- Cancel the stamp: The landlord signs across the stamp - partially on the stamp and partially on the receipt paper. This “cancellation” prevents the stamp from being reused.

- One stamp per receipt: Each receipt requires its own revenue stamp. You cannot use one stamp for multiple receipts.

When a Revenue Stamp Is Required

| Monthly Rent | Revenue Stamp Required? |

|---|---|

| Rs 4,500 | No - below Rs 5,000 threshold |

| Rs 5,000 | No - the threshold is “exceeding Rs 5,000,” meaning the amount must be above Rs 5,000, not equal to it |

| Rs 5,001 or above | Yes - Re 1 revenue stamp required |

| Rs 25,000 | Yes |

| Rs 50,000 | Yes (same Re 1 stamp regardless of amount) |

Consequences of Missing Revenue Stamps

Under Section 35 of the Indian Stamp Act, 1899, an instrument (including a receipt) that is not duly stamped is inadmissible in evidence in any court or before any authority. This means:

- An unstamped receipt cannot be relied upon as proof of rent payment in legal proceedings

- An Assessing Officer during tax assessment can technically reject an unstamped receipt

- However, Section 35 also provides that the receipt can be admitted if the deficient stamp duty plus a penalty (up to 10 times the deficiency) is paid

In practice, the absence of a revenue stamp on a rent receipt is treated with varying degrees of strictness:

- Most employers accept receipts without revenue stamps (checking content rather than stamps)

- Assessing Officers during regular processing typically do not scrutinize revenue stamps

- During scrutiny assessment, however, the absence of stamps may be raised as a technical objection, particularly if the department is looking for grounds to disallow the HRA claim

Best practice: Always affix revenue stamps. The cost is negligible (Re 1 per month = Rs 12 per year), and the protection it provides is disproportionately valuable.

Revenue Stamps on Digital Receipts

The requirement for revenue stamps predates digital communication, and no CBDT circular or amendment has specifically addressed how the stamp requirement applies to electronic receipts. The practical position:

- Digital receipts (email, PDF, electronically generated) cannot physically bear revenue stamps - there is no medium to affix them to

- The Information Technology Act, 2000 (Sections 4 and 5) gives legal recognition to electronic records, but does not specifically address stamp duty on electronic receipts

- Most employers and tax authorities accept digital receipts without revenue stamps, provided they contain all other required information

- To mitigate risk, maintain digital receipts alongside bank transfer records - the bank statement serves as independent, unstampable proof of payment

PAN Requirement: Section 10(13A) and CBDT Circular 08/2013

The Rule

If your total annual rent exceeds Rs 1,00,000 (approximately Rs 8,333 per month), you must provide the landlord’s PAN to your employer when submitting HRA proof.

This requirement was introduced by CBDT Circular No. 08/2013, dated October 10, 2013, which directed employers to obtain the landlord’s PAN where annual rent exceeds Rs 1,00,000.

Why It Matters

The PAN requirement serves a dual purpose:

- It enables the Income Tax department to cross-reference HRA claims with the landlord’s income tax return - verifying that the landlord has declared the rental income

- It deters fictitious HRA claims - fabricated receipts from non-existent landlords cannot include a verifiable PAN

If the Landlord Does Not Have a PAN

Many individual landlords - particularly senior citizens or those with income below the taxable threshold - may not possess a PAN. In such cases:

- Obtain a Form 60 declaration from the landlord

- Form 60 is a prescribed format under Rule 114B of the Income Tax Rules for persons who do not have a PAN

- The declaration should include:

- Landlord’s full name and address

- Statement that the landlord does not possess a PAN

- Landlord’s Aadhaar number

- Estimated total income for the financial year

- Landlord’s signature

- Submit this declaration to your employer in lieu of the landlord’s PAN

TDS Implications Under Section 206AA

If the landlord does not provide a PAN and the tenant is required to deduct TDS under Section 194-IB (for monthly rent exceeding Rs 50,000), the TDS rate increases from 2% to 20% under Section 206AA of the Income Tax Act. This is a significant penalty - on monthly rent of Rs 60,000, TDS jumps from Rs 1,200 to Rs 12,000 per month.

This creates a strong practical incentive for both parties to ensure the landlord’s PAN is available and documented.

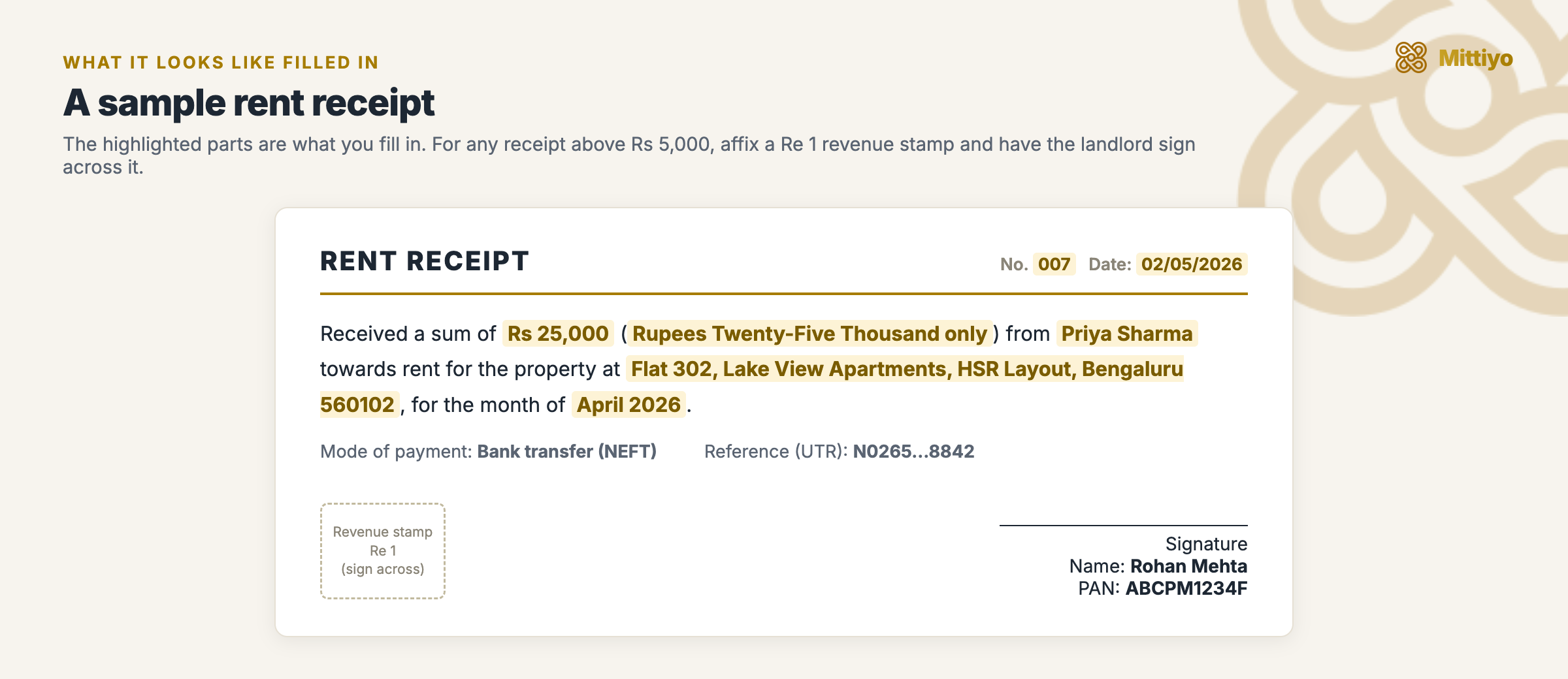

The Standard Rent Receipt Format

Physical Receipt Format

A filled example. The highlighted fields are what you complete each month; add the Re 1 revenue stamp on amounts above Rs 5,000.

A filled example. The highlighted fields are what you complete each month; add the Re 1 revenue stamp on amounts above Rs 5,000.

Key Format Notes

- Receipt number: Sequential numbering (001, 002, 003…) helps maintain a systematic record and demonstrates that receipts were generated periodically rather than in bulk at year-end

- Transaction reference: Including the UTR number (for NEFT/IMPS) or UPI reference number directly links the receipt to the bank transaction, creating an audit-proof chain of evidence

- PAN display: The landlord’s PAN should appear on the receipt only if the annual rent exceeds Rs 1 lakh. Including it below this threshold is not required but is not harmful

Digital Receipt Format

Digital receipts should contain all the same information as physical receipts, formatted as:

- An email from the landlord’s email address to the tenant, with all receipt details in the body or as a PDF attachment

- A PDF document with the landlord’s details, rent information, and either a scanned signature or a typed acknowledgment

- A digitally signed document using a digital signature certificate issued under the Information Technology Act, 2000

Important: A WhatsApp message from the landlord acknowledging receipt of rent (e.g., “Received Rs 25,000 for April 2025 rent for Flat 302, XYZ Apartments”) can serve as supplementary evidence but should not be the sole form of receipt. A proper formatted receipt (physical or email/PDF) is always preferable.

Digital Rent Receipts: Legal Validity and Practical Considerations

Legal Recognition

The Information Technology Act, 2000 provides the legal basis for the validity of digital records:

- Section 4: Legal recognition of electronic records - information shall not be denied legal effect solely on the ground that it is in electronic form

- Section 5: Legal recognition of electronic signatures - a signature shall not be denied legal effect solely on the ground that it is in electronic form

- Section 65B of the Indian Evidence Act, 1872 / Section 63 of the Bharatiya Sakshya Adhiniyam, 2023: Electronic records are admissible as evidence if accompanied by a certificate stating the manner in which the record was produced, the device involved, and the reliability of the system

These provisions collectively support the admissibility and validity of digital rent receipts for tax purposes.

Practical Advantages of Digital Receipts

- Automatic record-keeping: Email receipts create a timestamped, searchable archive

- No physical storage needed: Eliminates the risk of losing paper receipts

- Easy retrieval: Can be searched and retrieved for any period instantly

- Tamper-evident: Email timestamps and sender verification provide built-in authenticity markers

- No revenue stamp ambiguity: As discussed, the stamp requirement for digital receipts is unclear, and most authorities accept digital receipts without stamps

Practical Risks of Digital-Only Receipts

- Employer acceptance varies: Some employers - particularly older organizations or government employers - may insist on physical receipts

- Revenue stamp gap: If the Assessing Officer insists on stamped receipts during scrutiny, a digital-only receipt may be challenged

- Authentication concerns: A PDF receipt without a digital signature certificate is easier to fabricate than a physically signed receipt

Best Practice: The Dual-Record Approach

Maintain both digital receipts and bank transfer records:

- The digital receipt establishes: who paid, how much, for which property, for which period, and the landlord’s acknowledgment

- The bank transfer record (NEFT/IMPS/UPI statement) establishes: the exact amount, date, sender account, recipient account, and transaction reference

- Together, they form a mutually corroborating evidence chain that is extremely difficult to challenge during assessment

Rent Receipts vs Bank Transfer Records: The Critical Distinction

Why Bank Records Alone Are Insufficient

Many tenants assume that bank transfer records (NEFT, IMPS, UPI statements) are sufficient proof for HRA claims. They are not, because:

- No purpose specification: Bank statements show a transfer to a person/account but do not specify that the transfer was for “rent” - it could be a loan repayment, gift, or any other purpose

- No landlord acknowledgment: The bank statement shows money leaving your account but does not confirm the landlord received it as rent

- No property identification: Bank records do not specify which property the payment relates to

- No period specification: They do not indicate which month’s rent the payment covers

Why Receipts Alone Are Insufficient

Conversely, receipts without corresponding bank records create evidentiary gaps:

- No independent verification: The receipt is created by the landlord - a single-party document. Without a bank transfer, the only evidence of payment is the receipt itself

- Cash payment vulnerability: If the receipt claims cash payment, there is no external record to verify the transaction occurred

- Fabrication risk: In the context of HRA fraud, fabricated receipts from fictitious landlords are a known pattern. The Income Tax department specifically looks for bank records to corroborate receipts

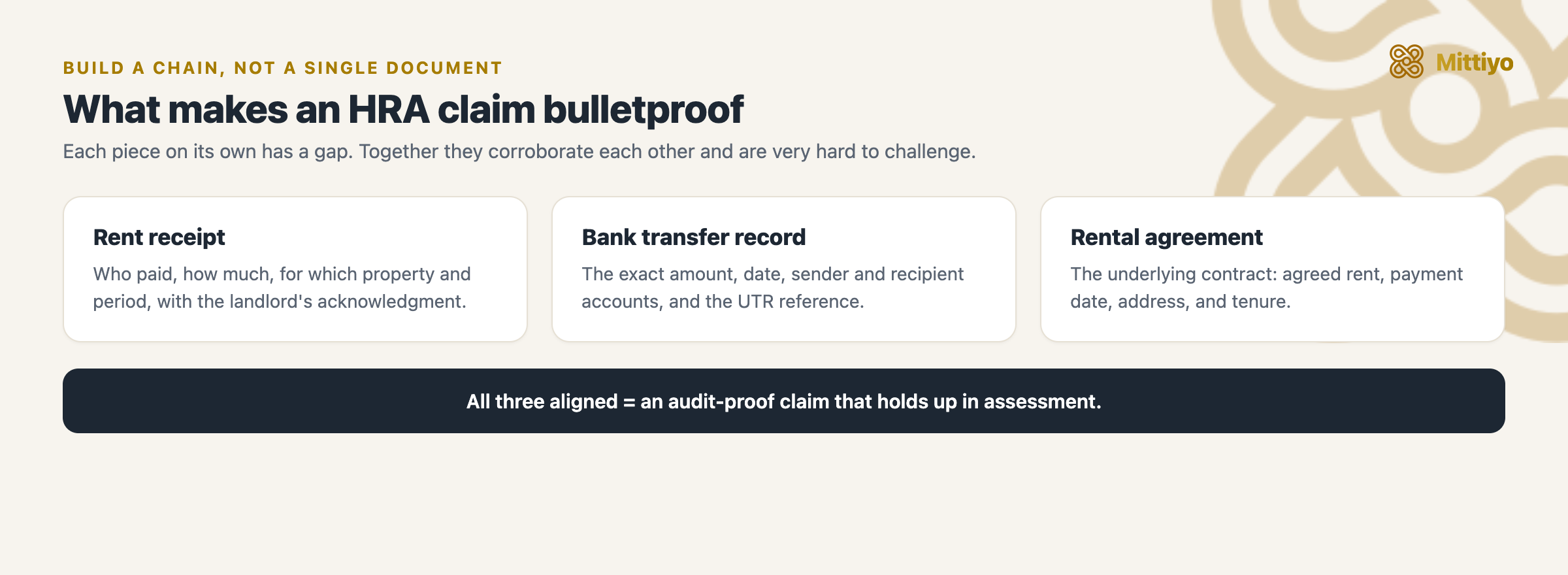

The Optimal Documentation Chain

For each month’s rent payment, the ideal documentation chain is:

- Bank transfer record: Shows the transfer from your account to the landlord’s account, with date, amount, and transaction reference

- Rent receipt: Issued by the landlord, referencing the same amount, date, period, and ideally the same transaction reference number

- Rental agreement: The underlying contract specifying the agreed rent amount, payment date, property address, and tenancy terms

When all three align, the HRA claim is effectively bulletproof during assessment.

Receipt, bank record, and agreement together make the claim hard to challenge.

Receipt, bank record, and agreement together make the claim hard to challenge.

Employer HRA Proof Submission: Complete Process

Timing

Most employers require HRA proof submission either:

- Quarterly: At the end of each quarter (June, September, December, March)

- Annually: In January-February for the financial year ending in March (this is more common)

- At year-end: During the “investment declaration proof” window, typically in February-March

Submit well before the employer’s deadline. Late submissions are often rejected outright, and the employer will compute tax on the full HRA amount without exemption.

Standard Submission Package

| Document | Quantity | Notes |

|---|---|---|

| Rent receipts | 12 (one per month) | Revenue stamps for amounts above Rs 5,000 |

| Rental agreement copy | 1 (certified copy) | Must cover the claim period |

| Landlord’s PAN copy | 1 | Required if annual rent > Rs 1 lakh |

| Form 60 declaration | 1 | Only if landlord does not have PAN |

| Bank statements (highlighted) | 1 set | Highlighting rent payment transactions |

| Declaration of tax regime | 1 | Confirming old regime (HRA available only under old regime) |

If Your Employer Rejects the Claim

If the employer rejects HRA proof (missing documents, format issues, deadline missed), the full HRA amount is taxed during the year. However, you can still claim the exemption when filing your income tax return:

- Include the HRA exemption under Section 10(13A) in your ITR

- The reduced tax liability will result in a refund of the excess tax deducted by the employer

- The Assessing Officer may request proof during processing - keep all documentation ready

- Note that claiming HRA exemption in the ITR (rather than through the employer) increases the likelihood of the return being selected for scrutiny assessment

TDS on Rent: The Section 194-IB Connection

While TDS on rent and rent receipts for HRA are technically separate provisions, they intersect in important ways:

When TDS Applies

Under Section 194-IB of the Income Tax Act, individuals and HUFs paying monthly rent exceeding Rs 50,000 must deduct TDS at 2% (rate effective from October 1, 2024, under the Finance (No. 2) Act, 2024).

The Process

- Deduct TDS: Deduct 2% from the rent payment. On monthly rent of Rs 60,000, TDS is Rs 1,200

- File Form 26QC: File the TDS return on the Income Tax e-filing portal (incometax.gov.in) within 30 days of the end of the month in which TDS is deducted

- Deposit TDS: Pay the TDS amount using the challan generated through Form 26QC

- Issue Form 16C: After filing Form 26QC, generate and provide Form 16C (TDS certificate) to the landlord

Impact on Rent Receipts

- The rent receipt should reflect the gross rent amount (before TDS deduction), not the net amount paid

- For example: if rent is Rs 60,000 and TDS of Rs 1,200 is deducted, the receipt should state Rs 60,000 as the rent amount

- The bank transfer will show Rs 58,800 (net amount), and the TDS of Rs 1,200 is deposited separately with the government

- Maintain Form 26QC acknowledgments and Form 16C copies as part of your documentation

PAN Interplay

- Form 26QC requires the landlord’s PAN - same PAN that is needed for HRA proof

- If the landlord does not provide PAN, TDS must be deducted at 20% (Section 206AA) instead of 2% - a significant penalty

- This creates a practical incentive to obtain the landlord’s PAN at the very beginning of the tenancy

Special Situations

Rent Paid to a Parent

If you pay rent to your parent and claim HRA exemption:

- The rent receipt must be from the parent (landlord) to you (tenant)

- The receipt should reference the rental agreement between you and the parent

- Payment must be through bank transfer - cash payments to parents for HRA purposes invite significant scrutiny

- The parent must include the rental income in their own income tax return

- If the parent’s total income (including rental income) is below the basic exemption limit, no tax is payable, but the income must still be disclosed

Multiple Landlords (Joint Ownership)

If the property is jointly owned by multiple persons:

- The rental agreement may be with all co-owners or with one co-owner authorized by others

- Rent receipts should ideally come from the person(s) named in the agreement

- PAN of the primary landlord (as per the agreement) is sufficient for HRA proof

Mid-Year Change of Accommodation

If you move from one rented accommodation to another during the financial year:

- Maintain separate sets of rent receipts for each property

- Each set should correspond to the relevant rental agreement

- Inform your employer of the change so that HRA exemption is calculated correctly for each period

- Provide both landlords’ PANs (if applicable)

Landlord Refuses to Provide Receipts

If your landlord refuses to issue rent receipts:

- First, request receipts in writing (email or WhatsApp) - this documents the refusal

- If the landlord still refuses, bank transfer records become your primary evidence

- Include a self-declaration along with bank statements when submitting to your employer

- The refusal to issue receipts may indicate tax evasion on the landlord’s part - while this is the landlord’s problem, it complicates your HRA claim

- Consider addressing this in the rental agreement itself - include a clause obligating the landlord to issue monthly rent receipts

Rent Below Rs 8,333/Month (Annual Rent Below Rs 1 Lakh)

If your annual rent is below Rs 1,00,000:

- Landlord’s PAN is not required for HRA proof

- Rent receipts are still required by most employers

- Revenue stamps are required on receipts above Rs 5,000 per month

- The HRA exemption formula still applies - the exemption may be small but is still valid

Common Mistakes and How to Avoid Them

1. Missing Revenue Stamps on Receipts Above Rs 5,000

The most common oversight. Revenue stamps cost Re 1 each and are available at any head post office. Buy a year’s supply (12 stamps) at once and affix them as each receipt is generated.

2. Not Collecting Landlord’s PAN for Annual Rent Above Rs 1 Lakh

Request the landlord’s PAN (or Form 60 declaration) at the time of executing the rental agreement - not when the employer’s HRA proof deadline is approaching. Chasing a landlord for their PAN in February is stressful and often unsuccessful.

3. Mismatch Between Receipt Amount and Agreement Amount

If your rental agreement states Rs 20,000 per month but your receipts show Rs 25,000 (to inflate HRA claims), the discrepancy between the agreement, receipts, and bank transfers will be immediately apparent during scrutiny assessment. Ensure all three amounts are consistent.

4. Round-Number Receipts Without Matching Bank Transfers

If you pay Rs 25,000 per month via bank transfer but your receipts show Rs 30,000, the mismatch between the bank statement (Rs 25,000 transfer) and the receipt (Rs 30,000) is a clear indication of inflation. The Assessing Officer will disallow the excess amount and may initiate penalty proceedings under Section 270A (underreporting - 50% of tax on underreported income).

5. Backdated Bulk Receipts

Generating all 12 monthly receipts at the end of the financial year (backdating them to each month) is extremely common but carries risks:

- Identical ink, paper, and handwriting across all receipts suggests bulk generation

- Revenue stamp lot numbers may indicate they were purchased together (not monthly)

- If the landlord’s signature varies across genuinely monthly receipts but is identical across bulk-generated receipts, this inconsistency can be detected

Best practice: Generate receipts monthly, as each rent payment is made.

6. Claiming HRA Under the New Tax Regime

HRA exemption under Section 10(13A) is not available under the new tax regime (Section 115BAC). If you have opted for the new regime (default from AY 2024-25), rent receipts will not help you claim HRA exemption. Verify your regime choice before preparing documentation.

7. Self-Generated Receipts Without Landlord Involvement

You cannot generate rent receipts yourself and sign them. The receipt must come from the landlord (or their authorized representative). Self-receipts are a clear indicator of fabrication.

8. Cash Payments Without Any Corroboration

Paying rent in cash and relying solely on receipts as proof is the weakest evidentiary position:

- No bank transfer record to independently verify the payment

- If the landlord denies receiving cash, you have no external proof

- During scrutiny, the Assessing Officer can cross-examine the landlord - if the landlord denies the receipts (or is unlocatable), the claim collapses

- Always prefer digital payments - even partial digital payment (e.g., Rs 20,000 via transfer + Rs 5,000 in cash) is stronger than full cash payment

9. Not Maintaining Receipts Beyond the Filing Year

Keep rent receipts and supporting documentation for at least 6 years after the end of the relevant assessment year. Under the Income Tax Act, assessment or reassessment proceedings can be initiated within this period (3 years under Section 149(1)(a), extendable to 10 years under Section 149(1)(b) for income escaping assessment exceeding Rs 50 lakh).

Key Takeaways

- Every rent receipt must include: tenant name, landlord name, property address, rent amount (figures and words), period, date, mode of payment, and landlord’s signature

- Revenue stamp (Re 1) is required for receipts above Rs 5,000 - affix and cancel with the landlord’s signature across the stamp. Cost is negligible; protection is significant

- Landlord’s PAN is mandatory if annual rent exceeds Rs 1 lakh - obtain Form 60 declaration if the landlord does not have a PAN

- Digital receipts are legally valid under the Information Technology Act, 2000 - maintain alongside bank transfer records for the strongest documentation

- Bank transfer records corroborate receipts but do not replace them; receipts specify purpose, property, and period while bank records verify the transaction

- Ensure consistency across all documents: agreement amount = receipt amount = bank transfer amount. Any mismatch invites scrutiny

- Generate receipts monthly rather than backdating a full year’s worth at year-end

- If monthly rent exceeds Rs 50,000, comply with TDS under Section 194-IB (2% deduction, Form 26QC, Form 16C)

- HRA exemption is available only under the old tax regime - verify your regime choice before preparing documentation

- Retain receipts and supporting documentation for at least 6 years after the assessment year

Paying rent you can actually stand behind?

HRA and 80GG claims hold up when the rent is genuine and matches the market. Before you sign your next place, see what residents say a building really rents for, the deposit, the society, the water and power reality, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: HRA exemption for salaried tenants · Section 80GG, if you do not receive HRA · TDS on rent (Section 194-IB)

References

- Income Tax Act, 1961 - Sections 10(13A) (HRA exemption), 80GG (rent deduction without HRA), 192 (TDS on salary), 194-IB (TDS on rent), 206AA (higher TDS without PAN), 115BAC (new regime), 149 (assessment time limits), 270A (penalty for underreporting)

- Income Tax Rules, 1962 - Rule 2A (HRA calculation), Rule 114B (Form 60 for persons without PAN)

- CBDT Circular No. 08/2013 (10 October 2013) - landlord’s PAN required where annual rent exceeds Rs 1 lakh

- Finance (No. 2) Act, 2024 - Section 194-IB TDS rate cut from 5% to 2% (effective 1 October 2024)

- Finance Act, 2023 - new tax regime made the default from AY 2024-25

- Indian Stamp Act, 1899 - Section 35 (admissibility of unstamped instruments), Section 40 (penalty); revenue-stamp requirement for receipts above Rs 5,000

- Information Technology Act, 2000 - Sections 4 and 5 (legal recognition of electronic records and signatures)

- Indian Evidence Act, 1872, Section 65B, now the Bharatiya Sakshya Adhiniyam, 2023, Section 63 - admissibility of electronic records (BSA in effect from 1 July 2024)

- Income Tax e-filing portal - Form 26QC filing and Form 16C generation