Rental income from property is one of the most common income sources in India, yet many landlords either under-report it or miss out on legitimate deductions that could reduce their tax liability. The Income Tax Department has sophisticated cross-referencing mechanisms - tenant TDS filings, property registration records, bank deposit patterns - that make non-disclosure increasingly risky. This guide covers the complete tax treatment of rental income for individual landlords for FY 2025-26 (Assessment Year 2026-27), including the calculation methodology, available deductions, the interplay between old and new tax regimes, TDS obligations, and reporting requirements.

How Rental Income Is Classified

Under the Income Tax Act, 1961, rental income is taxed under Section 22 - Income from House Property. This head applies to:

- Rent from residential property

- Rent from commercial property (shops, offices, warehouses)

- Rental income from land appurtenant to a building (such as a parking lot attached to the building)

- Composite rent (where rent includes charges for use of building and furniture/equipment - though the equipment component may be taxed under “Income from Other Sources”)

Important classifications:

- Income from subletting (if you are a tenant who sublets) is taxed under Income from Other Sources, not House Property, because you do not own the property. The 30% standard deduction under Section 24(a) is not available on subletting income.

- Income from property used for own business is not taxed under House Property - it is considered part of business income.

- Rental income from property situated outside India is also taxable under this head for Indian tax residents, subject to relief for taxes paid abroad under Section 90/91.

Ownership Requirement

Only the owner of the property (or the deemed owner under Section 27) can declare income under “Income from House Property.” Ownership is determined by legal title, not merely possession. Co-owners must declare rental income in proportion to their ownership share.

Deemed ownership (Section 27): In certain cases, a person who is not the legal owner is treated as the deemed owner for tax purposes:

- An individual who transfers property to a spouse (other than for adequate consideration) or minor child - the transferor is the deemed owner

- The holder of an impartible estate

- A member of a co-operative society or company allotted a building or part thereof

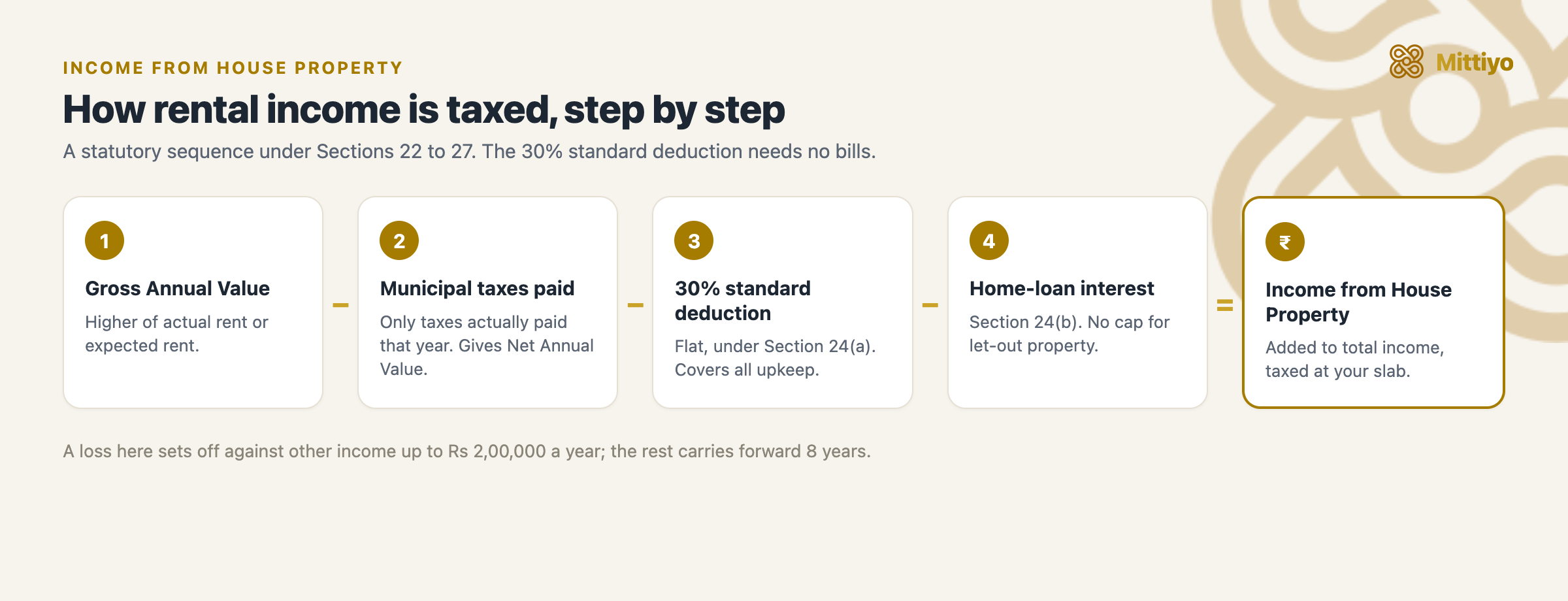

The Calculation Framework

The tax calculation follows a specific statutory sequence mandated by Sections 22-27 of the Income Tax Act:

From gross rent to taxable income from house property.

From gross rent to taxable income from house property.

Step 1: Gross Annual Value (GAV) - The Most Complex Step

The determination of GAV under Section 23 involves comparing multiple values:

| Component | What It Means | Source |

|---|---|---|

| Actual rent received/receivable | Rent actually collected from the tenant during the FY | Rent receipts, bank statements |

| Municipal rateable value | Value assessed by the municipal authority (BBMP in Bengaluru) | Property tax assessment order |

| Fair rent | Rent a similar property in the same locality would command | Market comparables |

| Standard rent | Rent fixed under the Rent Control Act (if applicable) | Rent Controller’s order |

The rule: GAV is the higher of actual rent received or the expected rent (which itself is the higher of municipal rateable value and fair rent, but capped at standard rent if applicable). However, if the property was vacant for part of the year and the actual rent received is lower than the expected rent due to vacancy, the actual rent received is taken as the GAV.

Practical simplification: For most Bengaluru landlords, the actual rent received exceeds the BBMP municipal valuation (which is typically much lower than market rent). In such cases, the actual rent received is the GAV. The comparison matters mainly when a property is let out at below-market rent (for example, to a relative at a nominal amount).

Step 2: Municipal Taxes

Only taxes actually paid during the financial year are deductible - not taxes due or outstanding. This follows the cash basis of accounting for this specific deduction.

Key points:

- BBMP property tax in Bengaluru is the primary municipal tax for most landlords

- Taxes paid in arrears are deductible in the year of actual payment

- The property owner (not the tenant) must have paid the tax - if the tenant pays the tax on behalf of the landlord, it is first treated as the landlord’s income (unreduced rent) and then allowed as a deduction

- SWM (Solid Waste Management) cess, if part of the BBMP tax bill, is also deductible

- Apartment maintenance charges paid to the apartment association are NOT municipal taxes and NOT deductible under this head

Step 3: Standard Deduction - 30% (Section 24(a))

This is a flat 30% deduction on the Net Annual Value (NAV = GAV minus municipal taxes). It is available irrespective of actual expenditure.

Important characteristics:

- No receipts or proof required - it is a statutory deduction

- It is meant to cover all expenses related to the property: repairs, maintenance, insurance, collection charges, painting, brokerage for tenant sourcing

- You cannot claim actual expenses in addition to the standard deduction - the 30% replaces actual expense claims

- Available under both old and new tax regimes for let-out property

- Not available for self-occupied property (since the NAV of self-occupied property is nil)

- Not available to the deemed owner of a property occupied by their employer

Step 4: Home Loan Interest (Section 24(b))

Interest on a loan taken for purchase, construction, repair, renovation, or reconstruction of the property is deductible:

| Property Type | Old Tax Regime | New Tax Regime (115BAC) |

|---|---|---|

| Let-out property | No upper limit | No upper limit |

| Self-occupied property | Up to Rs 2,00,000 | Not available |

| Self-occupied (pre-construction interest) | Deductible in 5 equal installments from year of completion | Not available |

Pre-construction interest: Interest paid during the construction period (from the date of borrowing to March 31 of the year preceding the year of completion) is deductible in 5 equal annual installments starting from the year the construction is completed.

Documentation: Obtain an interest certificate from the bank/NBFC showing the year-wise breakup of principal and interest. This is mandatory for claiming the deduction and is typically available on the lender’s online portal.

Worked Examples

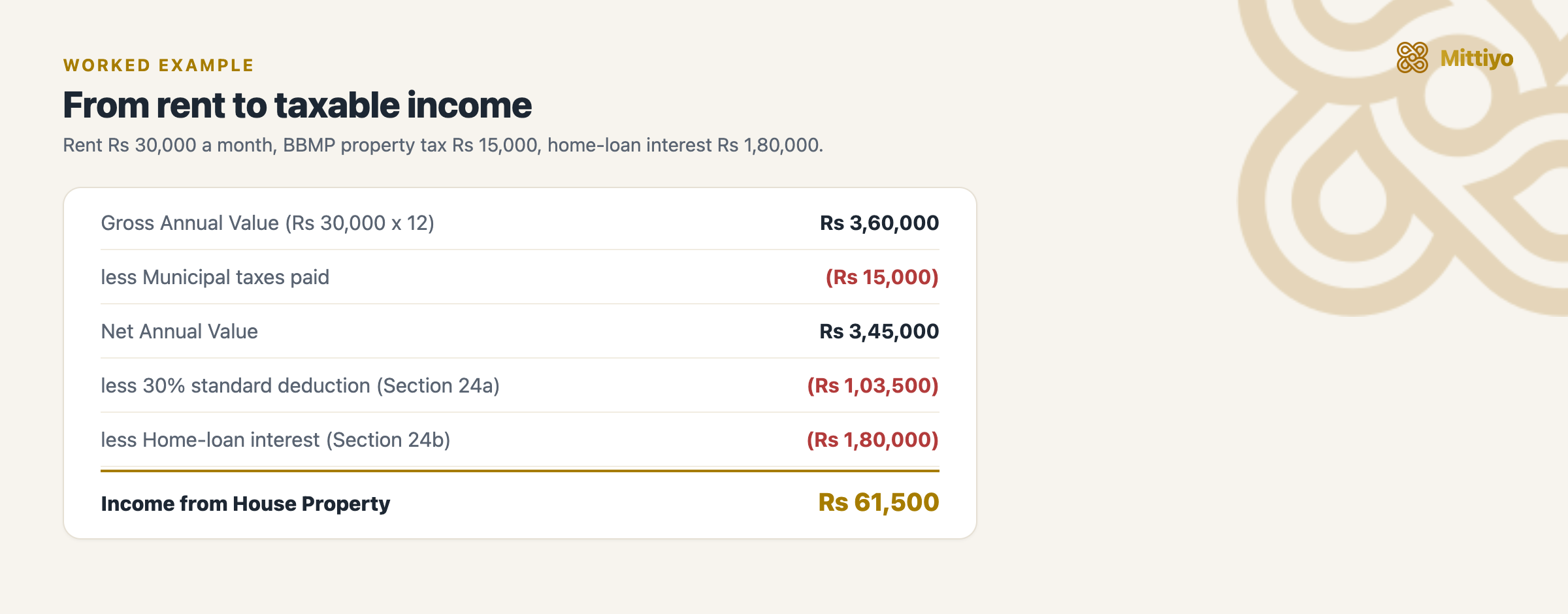

Example 1: Basic Rental Income Calculation

The calculation at a glance; the breakdown follows in the table.

The calculation at a glance; the breakdown follows in the table.

Property details:

- Monthly rent received: Rs 30,000

- BBMP property tax paid: Rs 15,000/year

- Home loan interest: Rs 1,80,000/year

| Component | Amount |

|---|---|

| Gross Annual Value (Rs 30,000 x 12) | Rs 3,60,000 |

| Less: Municipal taxes paid | (Rs 15,000) |

| Net Annual Value (NAV) | Rs 3,45,000 |

| Less: Standard deduction (30% of NAV) | (Rs 1,03,500) |

| Less: Home loan interest (Section 24(b)) | (Rs 1,80,000) |

| Income from House Property | Rs 61,500 |

This Rs 61,500 is added to the landlord’s total income and taxed at the applicable slab rate.

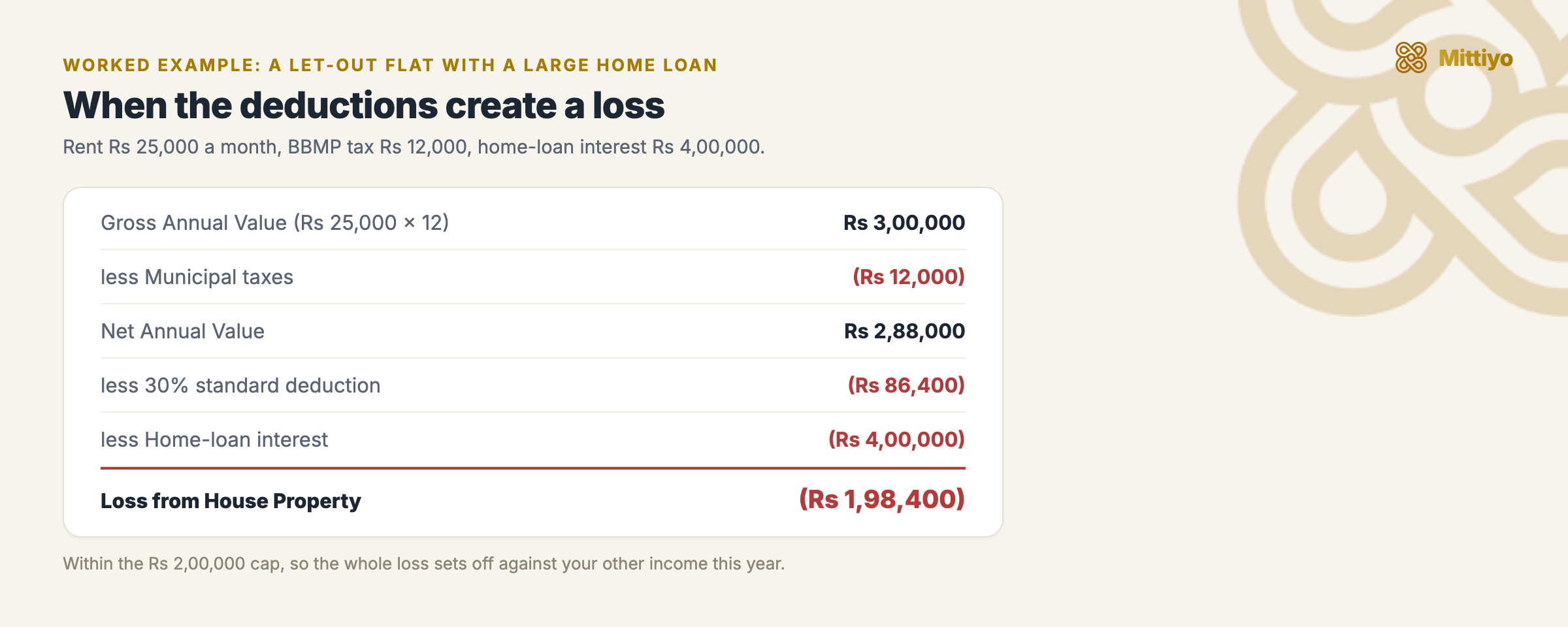

Example 2: Loss from House Property

A high loan turns house-property income into a deductible loss.

A high loan turns house-property income into a deductible loss.

Property details:

- Monthly rent received: Rs 25,000

- BBMP property tax paid: Rs 12,000/year

- Home loan interest: Rs 4,00,000/year (high-value property loan)

| Component | Amount |

|---|---|

| Gross Annual Value (Rs 25,000 x 12) | Rs 3,00,000 |

| Less: Municipal taxes paid | (Rs 12,000) |

| Net Annual Value (NAV) | Rs 2,88,000 |

| Less: Standard deduction (30% of NAV) | (Rs 86,400) |

| Less: Home loan interest (Section 24(b)) | (Rs 4,00,000) |

| Loss from House Property | (Rs 1,98,400) |

This loss of Rs 1,98,400 can be set off against other income (salary, business income) up to Rs 2,00,000 in the same financial year. Since the loss (Rs 1,98,400) is within the Rs 2,00,000 limit, the entire amount can be set off.

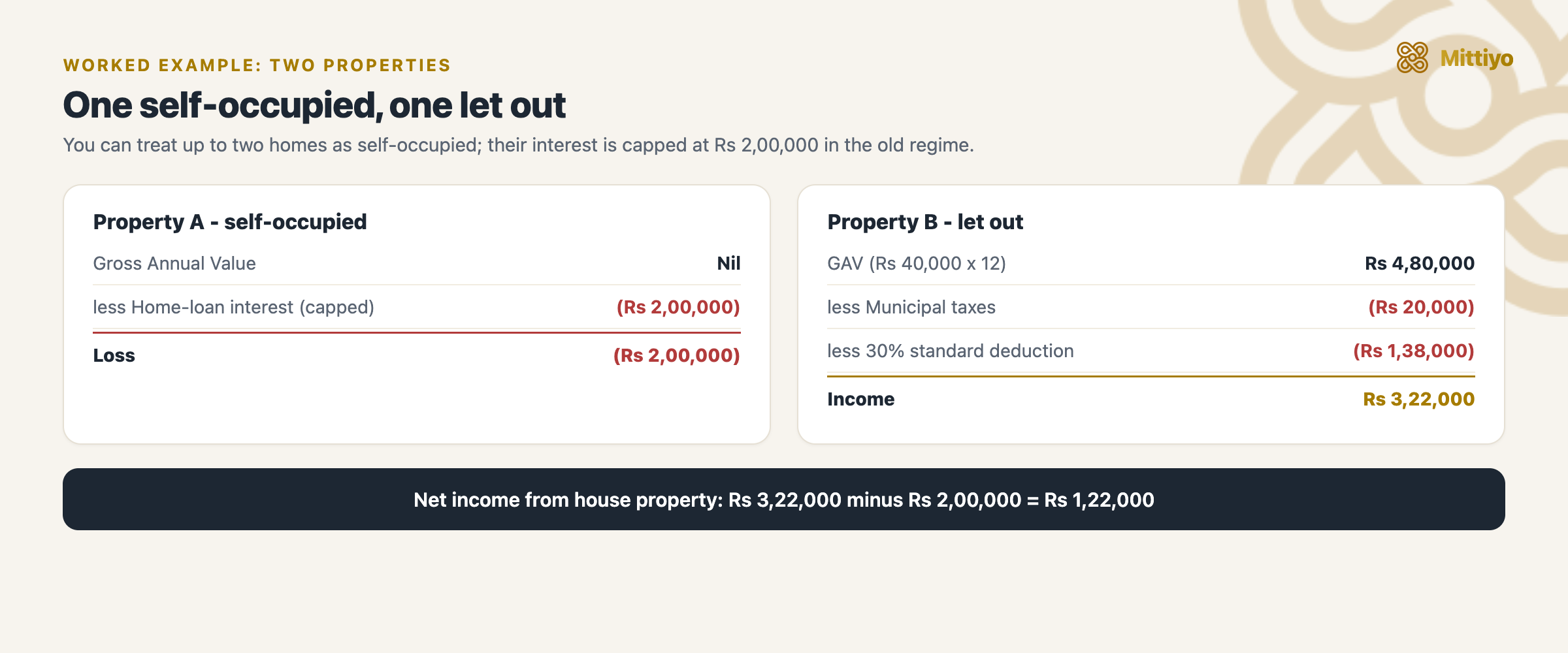

Example 3: Multiple Properties

A self-occupied loss offsets the let-out property’s income.

A self-occupied loss offsets the let-out property’s income.

Landlord owns two properties:

- Property A: Self-occupied (no rent, home loan interest Rs 2,50,000/year)

- Property B: Let out at Rs 40,000/month (no home loan)

Property A (Self-occupied):

| Component | Amount |

|---|---|

| GAV (self-occupied) | Nil |

| Less: Home loan interest (capped at Rs 2,00,000 for self-occupied) | (Rs 2,00,000) |

| Loss from Property A | (Rs 2,00,000) |

Property B (Let-out):

| Component | Amount |

|---|---|

| GAV (Rs 40,000 x 12) | Rs 4,80,000 |

| Less: Municipal taxes (say Rs 20,000) | (Rs 20,000) |

| NAV | Rs 4,60,000 |

| Less: Standard deduction (30%) | (Rs 1,38,000) |

| Income from Property B | Rs 3,22,000 |

Net Income from House Property: Rs 3,22,000 - Rs 2,00,000 = Rs 1,22,000

Multiple Properties - Special Rules

Old Regime

If you own more than one property, you can treat only one as self-occupied (GAV = Nil). All others are “deemed let-out” even if vacant - you must calculate and pay tax on the expected rental value. From AY 2020-21, you can treat up to two properties as self-occupied (GAV = Nil for both), but the aggregate interest deduction on self-occupied properties remains capped at Rs 2,00,000.

New Regime (Section 115BAC)

Under the new tax regime (default from FY 2023-24):

- You can treat up to two properties as self-occupied (GAV = Nil)

- No deduction under Section 24(b) for self-occupied property - home loan interest on self-occupied property is not deductible

- For let-out property: 30% standard deduction and municipal taxes continue to apply

- For let-out property: Section 24(b) interest deduction is available with no upper limit

Loss from House Property

If the total deductions (standard deduction + interest) exceed the Net Annual Value, the result is a loss from house property.

Set-off Rules (Section 71)

- Loss from house property can be set off against other income (salary, business, capital gains, other sources) up to Rs 2,00,000 in the same financial year

- This Rs 2,00,000 limit applies to the aggregate loss from house property - if you have losses from multiple properties, the combined set-off is capped at Rs 2,00,000

Carry Forward Rules (Section 71B)

- Any excess loss (beyond Rs 2,00,000) can be carried forward for up to 8 assessment years

- Carried forward loss can be set off only against income from house property in subsequent years - it cannot be set off against salary or business income

- To carry forward the loss, you must file the income tax return within the due date under Section 139(1)

Strategic Implications

For landlords with home loans on let-out property, the interest deduction (with no upper limit) can create substantial losses. These losses can reduce your total tax liability significantly. If you are considering buying an investment property with a loan, the tax benefit of the interest deduction should be factored into the investment analysis.

Unrealized Rent (Section 25A)

Under Section 25A, rent that a landlord could not realize from a tenant (bad debt) can be excluded from income if all of the following conditions are met:

- The tenancy is genuine (bona fide)

- The defaulting tenant has vacated the property, or the landlord has taken steps to compel the tenant to vacate

- The landlord has taken reasonable steps to institute legal proceedings for recovery or has satisfied the Assessing Officer that legal proceedings would be useless

- The unrealized rent has been written off in the landlord’s books of account

Recovery of unrealized rent: If rent previously excluded under Section 25A is subsequently recovered, it is taxable in the year of recovery under Section 25A(1), after deducting the 30% standard deduction.

Arrears of Rent (Section 25A)

Arrears of rent received in a year after the year in which they were due are taxable in the year of receipt. The 30% standard deduction is allowed on such arrears. This applies regardless of whether the landlord was the owner of the property in the year the arrears relate to.

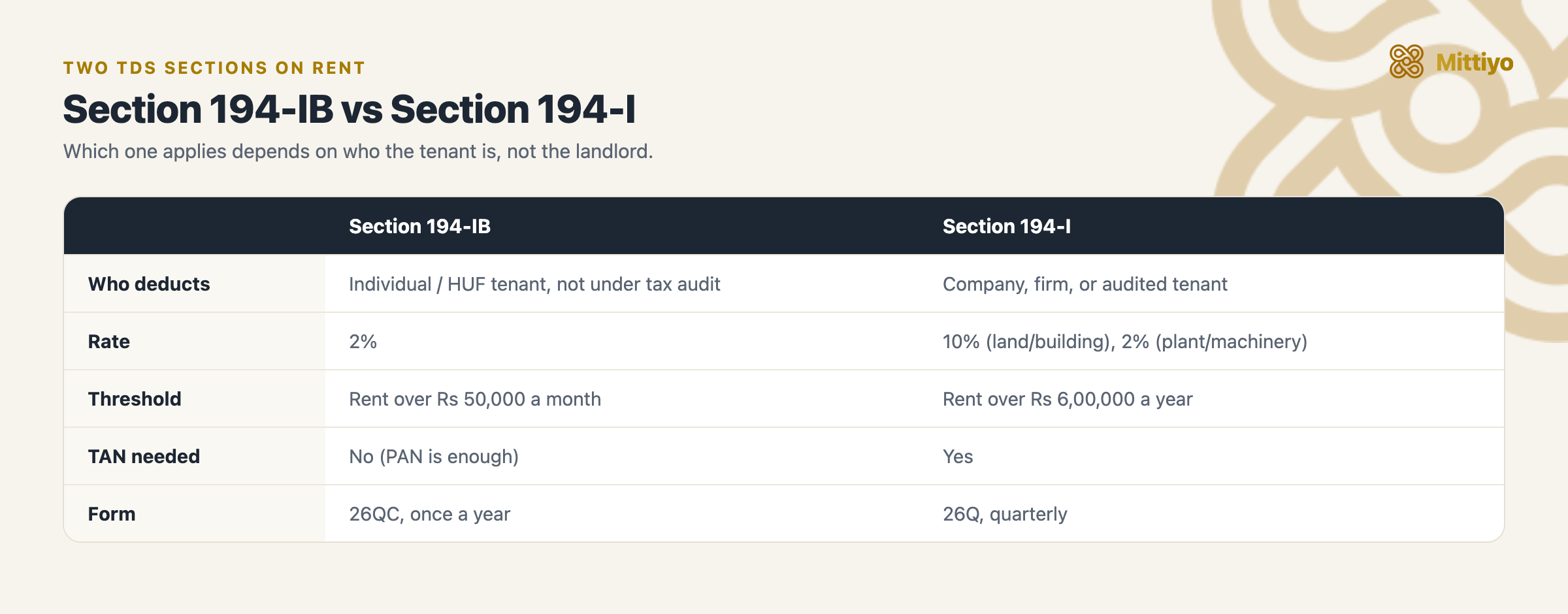

TDS on Rent (Section 194-IB)

Section 194-IB imposes a TDS obligation on tenants (not landlords) paying rent exceeding Rs 50,000 per month. While this is the tenant’s obligation, landlords should understand it because TDS impacts their tax credits.

| Factor | Details |

|---|---|

| Threshold | Monthly rent exceeding Rs 50,000 |

| TDS Rate | 2% (with effect from October 1, 2024; was 5% for the period up to September 30, 2024) |

| Who deducts | The tenant (individual or HUF, not subject to tax audit) |

| When to deduct | At the time of rent payment or credit to the landlord’s account |

| How to deposit | File Form 26QC on incometax.gov.in within 30 days of the end of the financial year or tenancy, whichever is earlier |

| Certificate | Tenant issues Form 16C to the landlord after TDS deposit |

| PAN requirement | Both tenant and landlord must have PAN |

| Non-compliance penalty | Interest at 1% per month for late deduction, 1.5% per month for late deposit |

Rate history: For FY 2025-26 the rate is a flat 2%. The cut happened mid-way through FY 2024-25: the Finance (No. 2) Act, 2024 reduced the rate from 5% to 2% effective October 1, 2024, so only that transitional year was split (5% to September 30, 2024, then 2%).

For landlords: Verify that TDS deducted by your tenant appears in your Form 26AS / AIS (Annual Information Statement) on the income tax portal. If it does not appear, follow up with the tenant to file Form 26QC. The TDS credit reduces your final tax liability.

Section 194-I: TDS by Business Tenants

If the tenant is a business entity (company, firm, or individual/HUF subject to tax audit), TDS on rent is governed by Section 194-I:

| Factor | Rent of Plant/Machinery/Equipment | Rent of Land/Building/Furniture |

|---|---|---|

| TDS Rate | 2% | 10% |

| Threshold | Aggregate rent exceeding Rs 6,00,000 in a financial year (raised from Rs 2,40,000 by the Finance Act, 2025, effective 1 April 2025) | Same |

Key difference: Section 194-I applies to business tenants and has a higher TDS rate (10% for land/building). Section 194-IB applies to individual/HUF tenants not subject to tax audit and has a lower rate (2% from October 2024).

Which TDS section applies depends on who the tenant is.

Which TDS section applies depends on who the tenant is.

Old Tax Regime vs New Tax Regime: Impact on Rental Income

What each regime allows on rental income.

What each regime allows on rental income.

| Feature | Old Regime | New Regime (115BAC) |

|---|---|---|

| 30% standard deduction (S.24(a)) | Available for let-out | Available for let-out |

| Municipal taxes deduction | Available | Available |

| Home loan interest - let-out (S.24(b)) | No limit | No limit |

| Home loan interest - self-occupied (S.24(b)) | Up to Rs 2,00,000 | Not available |

| Loss set-off against other income | Up to Rs 2,00,000 | Up to Rs 2,00,000 |

| Carry forward of loss | Up to 8 years | Up to 8 years |

Practical implication: If you have a self-occupied property with a significant home loan, the old regime is likely more beneficial due to the Rs 2,00,000 interest deduction on self-occupied property. If you have only let-out property with no home loan, both regimes are similar for house property income, and the choice depends on other deductions (80C, 80D, etc.).

Reporting Rental Income in ITR

| ITR Form | Who Should Use |

|---|---|

| ITR-1 (Sahaj) | Salaried individuals with one house property and total income up to Rs 50 lakh |

| ITR-2 | Individuals with more than one house property, or income exceeding Rs 50 lakh, or capital gains |

| ITR-3 | Individuals with business/professional income in addition to rental income |

| ITR-4 (Sugam) | Individuals with presumptive business income (Section 44AD/44ADA) and one house property |

Under “Income from House Property” in the ITR form:

- Enter the address of each let-out property

- Enter the tenant’s name and PAN (if available)

- Enter the annual rent received or receivable

- Enter municipal taxes actually paid during the year

- The form auto-calculates the standard deduction (30%)

- Enter home loan interest (if applicable), with lender details

- For self-occupied property, enter “self-occupied” and claim interest deduction (old regime)

- For deemed let-out property (vacant second property), estimate and enter expected rental value

Supporting documents to maintain (not to be uploaded, but to be available if requested during assessment):

- Rental agreement/deed

- Rent receipts or bank statements showing rent received

- Municipal tax payment receipts (BBMP)

- Home loan interest certificate from the bank

- Form 16C received from tenant (TDS certificate)

Common Mistakes Landlords Make

Not reporting rental income at all - The Income Tax Department cross-references TDS filings (Form 26QC by tenants), property registration records, stamp duty data, and bank deposits. With AIS (Annual Information Statement) now showing high-value transactions, non-reporting is easily detectable.

Claiming actual expenses instead of standard deduction - You cannot claim painting costs, repair bills, brokerage, or insurance premiums as separate deductions. The 30% standard deduction is meant to cover all such expenses. It is a flat deduction - even if your actual expenses are higher, you get only 30%.

Not claiming the standard deduction at all - Some landlords forget to claim the 30% standard deduction, leading to over-reporting of income.

Ignoring deemed let-out property - If you own a second property that is vacant, it must be shown as “deemed let-out” and taxed on the expected rental value. You cannot show it as self-occupied if you already have one (or two, from AY 2020-21) self-occupied properties.

Not maintaining rent receipts - Both landlord and tenant should maintain documentation. Bank transfers create automatic records; cash rent payments should always be accompanied by receipts.

Not reconciling Form 26AS / AIS - TDS deducted by your tenant should reflect in your Form 26AS and AIS. If it does not, you lose the tax credit. Check before filing your return.

Incorrect treatment of co-owned property - If a property is co-owned (for example, by husband and wife), each co-owner must declare rental income in proportion to their ownership share. The entire income cannot be shown in one person’s return.

Not claiming pre-construction interest - Interest paid during the construction period is deductible in 5 equal installments from the year of completion. Many landlords forget this deduction entirely.

Rental Income from NRI Landlords

If the landlord is a Non-Resident Indian (NRI), additional provisions apply:

- The tenant must deduct TDS at 30% (plus surcharge and cess) under Section 195 on rent paid to an NRI landlord - not at the lower rates under Section 194-I or 194-IB

- The NRI landlord can apply for a lower TDS certificate under Section 197 if the actual tax liability is lower

- The NRI landlord must file an Indian income tax return reporting the rental income

- DTAA (Double Tax Avoidance Agreement) provisions may apply if the NRI is a tax resident of a country with which India has a treaty

Key Takeaways

- Rental income is taxed under “Income from House Property” with a statutory 30% standard deduction - this replaces all actual expense claims

- Municipal taxes actually paid during the year and home loan interest are deductible on top of the standard deduction

- Loss from house property can be set off against other income up to Rs 2 lakh per year; excess losses carry forward for 8 years

- TDS at 2% (from October 1, 2024) applies when monthly rent exceeds Rs 50,000 - this is the tenant’s obligation, but landlords should verify it in their Form 26AS/AIS

- Under the new tax regime, home loan interest on self-occupied property is not deductible - compare both regimes before filing

- Report rental income in ITR-1 (single property, income up to Rs 50 lakh) or ITR-2 (multiple properties or higher income)

- Vacant second property is deemed let-out and taxable on expected rental value - this is a common area of non-compliance

- Co-owned property income must be split between co-owners in proportion to ownership shares

- Maintain rental agreements, rent receipts, bank statements, BBMP tax receipts, and loan interest certificates as supporting documentation

Setting the right rent for your property?

The income you report starts with the rent you charge, and tenants increasingly check before they sign. See what residents say buildings in your area actually command, and how they rate the society, water, and power, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: TDS on rent (Section 194-IB) · Rent receipts for tax · Security deposit rules in Karnataka

References

Unless noted, all section references are to the Income Tax Act, 1961.

- Sections 22-27 - Income from House Property

- Section 24(a) - 30% standard deduction

- Section 24(b) - interest on borrowed capital

- Section 23 - annual value determination

- Section 25A - unrealized rent and arrears

- Section 71 - set-off of loss from house property

- Section 71B - carry-forward of house-property loss

- Section 194-IB - TDS on rent by individuals/HUFs

- Section 194-I - TDS on rent by business entities

- Section 115BAC - new tax regime

- Section 27 - deemed ownership

- Section 195 - TDS on payments to NRIs

- Finance (No. 2) Act, 2024 - Section 194-IB rate cut from 5% to 2% (effective 1 October 2024); Finance Act, 2025 - Section 194-I threshold raised to Rs 6,00,000 (from 1 April 2025)

- CBDT Circular No. 01/2022 (7 February 2022) - guidelines on AIS and TIS

- CBDT Notification No. 26/2019 - Form 26QC and Form 16C for Section 194-IB compliance