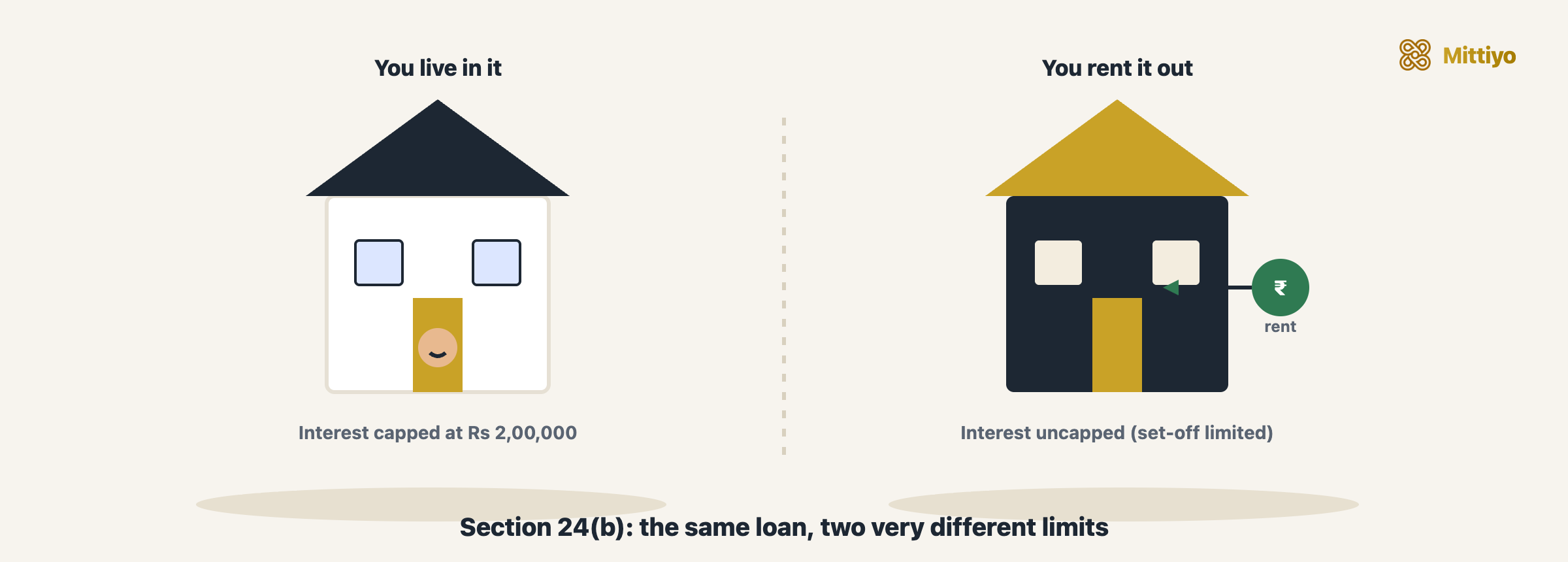

Of all the home loan tax benefits, the interest deduction under Section 24(b) is the largest and the most misunderstood. The confusion almost always comes down to one distinction: is the property self-occupied or let out? That single fact decides whether your deduction is capped at Rs 2,00,000 or effectively unlimited, and how much of it you can actually use this year.

There is also a second trap, the same one that catches HRA and most other deductions: the new tax regime, now the default, removes the self-occupied interest deduction entirely. This guide breaks down exactly how Section 24(b) works for each type of property, the set-off limit that quietly caps the let-out benefit, pre-construction interest, and what survives under each regime.

What Section 24(b) actually allows

Rental and home loan income are taxed under the head Income from House Property in the Income-tax Act, 1961. The taxable figure is built like this:

- Start with the property’s annual value (the rent it earns, or for a self-occupied home, nil).

- Subtract municipal taxes paid.

- Subtract a flat 30% standard deduction (let-out property only).

- Subtract the home loan interest under Section 24(b).

Section 24(b) is step 4. It lets you deduct the interest you pay on money borrowed to buy, build, repair, or reconstruct the property. (The principal repayment is a separate benefit, under Section 80C.) How much interest you can deduct is where self-occupied and let-out part ways.

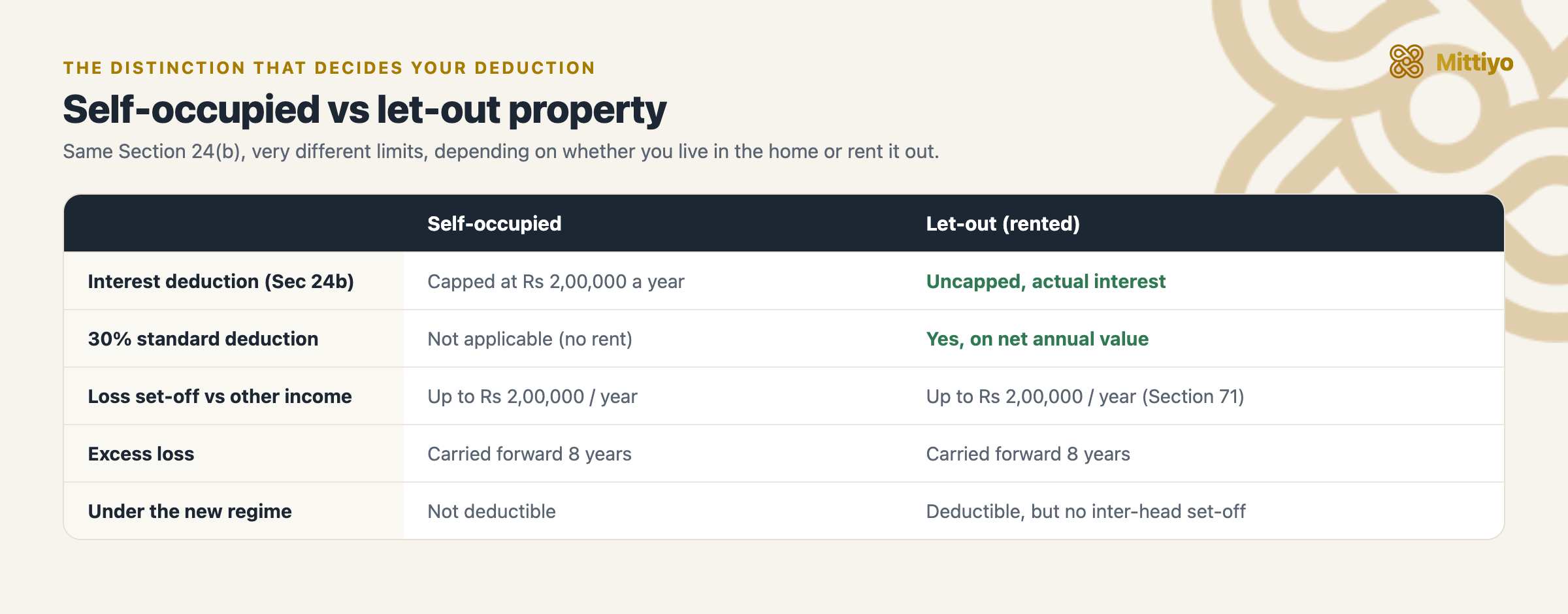

Self-occupied property: capped at Rs 2,00,000

If you live in the property yourself (or it is treated as self-occupied because you cannot occupy it for work reasons), the interest deduction is capped at Rs 2,00,000 per financial year.

Two conditions attach to the full Rs 2,00,000:

- The loan must be taken for purchase or construction (not merely repair, which is capped at Rs 30,000).

- The purchase or construction must be completed within five years from the end of the financial year in which the loan was taken. Miss that, and the cap drops to Rs 30,000.

Because a self-occupied property earns no rent, this interest creates a loss from house property of up to Rs 2,00,000, which you set off against your salary or other income, reducing your taxable income.

Let-out property: uncapped interest, but watch the set-off

The headline difference: self-occupied interest is capped at Rs 2,00,000; let-out interest is not, but the set-off against other income is.

The headline difference: self-occupied interest is capped at Rs 2,00,000; let-out interest is not, but the set-off against other income is.

If the property is let out, there is no cap on the interest you can deduct under Section 24(b). The full interest reduces your rental income, and frequently turns it into a loss (because interest in the early years usually exceeds the net rent).

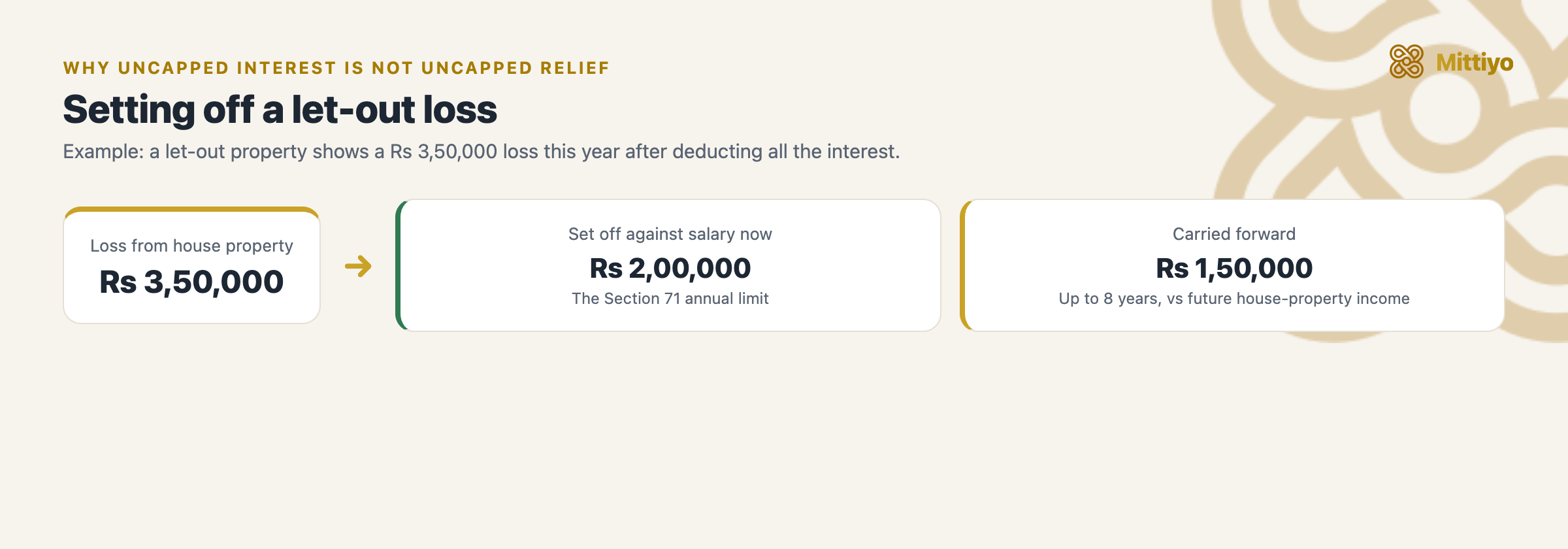

Here is the catch most people miss. While the interest deduction is uncapped, the loss from house property that you can set off against your other income (salary, business, etc.) in the same year is limited to Rs 2,00,000 under Section 71. Any loss beyond that is carried forward for up to eight years under Section 71B, and in those later years it can only be set off against income from house property.

Uncapped interest does not mean uncapped relief this year. The set-off against salary is limited to Rs 2,00,000 annually.

Uncapped interest does not mean uncapped relief this year. The set-off against salary is limited to Rs 2,00,000 annually.

So if your let-out property throws up a Rs 3,50,000 loss this year, you can set off Rs 2,00,000 against your salary now and carry the remaining Rs 1,50,000 forward.

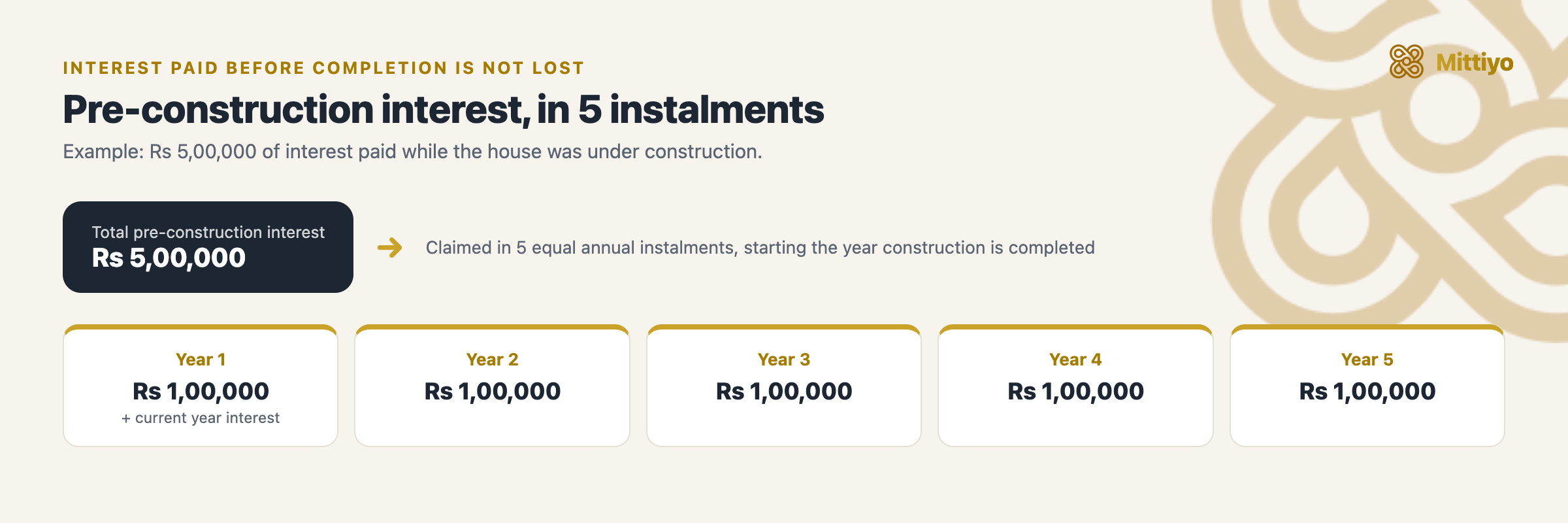

Pre-construction (prior-period) interest

Interest you pay before the property is completed does not disappear. It is accumulated and then deducted in five equal annual instalments, beginning in the financial year construction is completed.

Interest paid during construction is not lost, it is spread over five years from completion.

Interest paid during construction is not lost, it is spread over five years from completion.

For a self-occupied property, these instalments count within the Rs 2,00,000 annual cap, alongside the current year’s interest, so the cap often absorbs them entirely. For a let-out property, they add to the (uncapped) interest deduction.

Worked examples: self-occupied and let-out

The same loan produces very different numbers depending on how the property is used.

Self-occupied flat, interest of Rs 2,80,000 in the year:

| Step | Amount |

|---|---|

| Annual value (you live in it) | Nil |

| Interest under Section 24(b) | Rs 2,80,000 |

| Deductible (capped) | Rs 2,00,000 |

| Loss from house property set off against salary | Rs 2,00,000 |

| Tax saved (30% slab) | about Rs 62,400 |

The Rs 80,000 of interest above the cap gives no benefit at all. This is the ceiling that makes the self-occupied case simple, and limited.

Let-out flat, rent of Rs 3,60,000 and interest of Rs 5,00,000:

| Step | Amount |

|---|---|

| Gross annual rent | Rs 3,60,000 |

| Less: municipal taxes paid | Rs 10,000 |

| Net annual value | Rs 3,50,000 |

| Less: 30% standard deduction | Rs 1,05,000 |

| Less: interest under Section 24(b) (uncapped) | Rs 5,00,000 |

| Income (loss) from house property | (Rs 2,55,000) |

| Set off against salary this year (Section 71 limit) | Rs 2,00,000 |

| Carried forward (up to 8 years) | Rs 55,000 |

Here the full Rs 5,00,000 interest is deductible, but the loss it creates can only relieve Rs 2,00,000 of your other income this year; the remaining Rs 55,000 waits for future house-property income.

Joint home loans

If the loan is joint and the property is co-owned, each person who is both a co-owner and a co-borrower claims the interest in proportion to their share. A 50:50 couple on a self-occupied flat can therefore claim up to Rs 2,00,000 of interest each (up to Rs 4,00,000 between them), and up to Rs 1,50,000 of principal each under Section 80C. The split must follow the genuine ownership share, not one chosen to maximise the deduction.

The new regime changes everything

Everything above is the old regime position. Under the new tax regime, the default since FY 2023-24:

- Self-occupied interest: not deductible. The Rs 2,00,000 benefit is simply gone.

- Let-out interest: still deductible against that property’s rental income. But if it creates a loss from house property, that loss cannot be set off against your salary or other income, and cannot be carried forward to set off other heads.

- Section 80C principal: not available.

In short, if your home loan is on the home you live in, the interest deduction is worth claiming only under the old regime. Compute your tax both ways before you file, because the new regime’s lower slab rates and Rs 75,000 standard deduction can still win for some borrowers, especially those with small or nearly-paid-off loans.

Section 80EE and 80EEA: mostly history now

These sections once offered an additional interest deduction (Rs 50,000 under 80EE, up to Rs 1,50,000 under 80EEA) over and above Section 24(b), for first-time and affordable-housing buyers. Both have sunset: Section 80EEA applied only to loans sanctioned up to 31 March 2022, so no new loan qualifies, and neither is available under the new regime. For nearly every current borrower, Section 24(b) is the operative interest deduction.

Common mistakes to avoid

- Assuming let-out interest gives unlimited relief this year. The interest is uncapped, but the set-off against salary is limited to Rs 2,00,000 a year.

- Staying on the new regime and silently losing the self-occupied interest deduction.

- Forgetting pre-construction interest, which is claimable in five instalments from completion.

- Mixing up interest and principal. Interest is Section 24(b); principal is Section 80C. They have separate limits.

- Counting on Section 80EE/80EEA for a new loan, when those windows have closed.

Key takeaways

- Self-occupied: interest capped at Rs 2,00,000 a year (Rs 30,000 if the loan is for repair, or completion took over five years).

- Let-out: uncapped interest, but the loss set-off against other income is limited to Rs 2,00,000 a year, with the rest carried forward eight years.

- Pre-construction interest: five equal annual instalments from the year of completion.

- New regime: no self-occupied interest, no 80C; let-out interest survives but with no inter-head set-off. Compare both regimes before filing.

Buying a property to let out?

The rent it earns drives both your loan maths and your tax. See what residents say buildings in the area actually command, and how they rate the society, water, and upkeep, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: Rental income tax for landlords · HRA and home loan in the same year · Rent receipts for tax

References

- Income-tax Act, 1961, Section 24 (deductions from income from house property), Section 71 (set-off of loss from house property, limited to Rs 2,00,000), Section 71B (carry-forward), and Section 80C (principal repayment)

- Income tax e-filing portal (regime choice and return filing)

- Threshold limits under the Income-tax Act, Income Tax Department