The Indian income tax system provides two distinct mechanisms for taxpayers who pay rent for residential accommodation. The more widely known mechanism is the HRA exemption under Section 10(13A), available to salaried employees who receive House Rent Allowance as part of their compensation. The less widely known - but equally important - mechanism is Section 80GG of the Income Tax Act, 1961, which provides a deduction for individuals who pay rent but do not receive HRA.

Section 80GG serves a critical segment of the taxpaying population: self-employed professionals, freelancers, gig workers, small business owners, and salaried employees whose salary structure does not include HRA. For these taxpayers, Section 80GG is the only route to claiming a tax benefit on rent paid, and understanding its eligibility criteria, calculation method, and filing requirements is essential for optimizing their tax position.

This guide provides a comprehensive analysis of Section 80GG, including the eligibility framework, detailed calculation methodology with worked examples across different income and rent scenarios, the Form 10BA requirement, the interaction with the old and new tax regimes, comparisons with HRA exemption, documentation requirements, common mistakes that lead to disallowance, and the judicial interpretation of key provisions.

The Legislative Framework

Section 80GG - Text and Interpretation

Section 80GG is part of Chapter VI-A of the Income Tax Act, 1961, which deals with deductions from gross total income. The section was introduced to provide tax relief to individuals who pay rent but cannot claim the HRA exemption because their compensation structure does not include HRA.

The Essential Elements:

The deduction is available to an “assessee, being an individual” - this limits the benefit to individuals only. Companies, Hindu Undivided Families (HUFs), partnership firms, and other entities cannot claim Section 80GG. The individual must be paying rent “in respect of any furnished or unfurnished accommodation occupied by him for the purposes of his own residence.” The accommodation must be used as a residence - rent paid for commercial premises (office, shop, warehouse) does not qualify.

Rule 11B of the Income Tax Rules, 1962:

The calculation formula for the Section 80GG deduction is specified in Rule 11B, not in Section 80GG itself. Rule 11B provides that the deduction shall be the least of three computed amounts (discussed in detail in the calculation section below).

Historical Context

Section 80GG has been in the Income Tax Act for decades, but the deduction limit has been revised only once in recent history. Until March 31, 2016, the per-month limit was Rs 2,000 (Rs 24,000 per year). The Finance Act, 2016 raised this to Rs 5,000 per month (Rs 60,000 per year), effective from FY 2016-17. This was a significant increase that made the deduction more meaningful in the context of urban rents. However, even at Rs 60,000 per year, the deduction covers only a fraction of the rent paid by most urban tenants - a freelancer in Bengaluru paying Rs 20,000 per month in rent pays Rs 2,40,000 annually but can deduct only Rs 60,000.

Eligibility Criteria: A Detailed Analysis

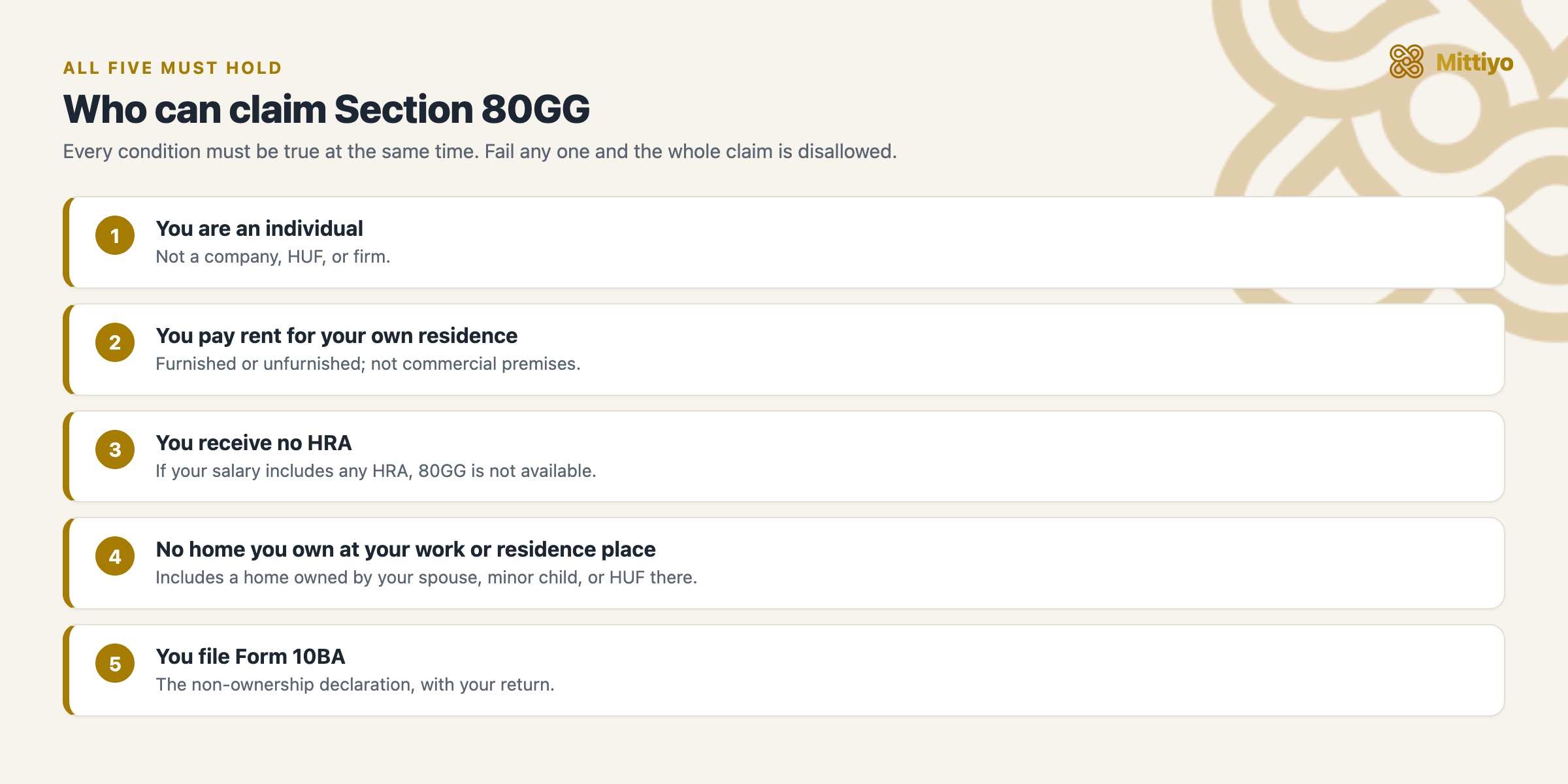

To claim the Section 80GG deduction, the individual must satisfy all of the following conditions simultaneously. Failure on any single condition disqualifies the entire claim.

All five conditions must be true at once.

All five conditions must be true at once.

Condition 1: The Assessee Must Be an Individual

Only individuals (natural persons) can claim Section 80GG. This excludes Hindu Undivided Families (HUFs), partnership firms, companies, LLPs, and trusts. A partner in a partnership firm who pays rent from personal income can claim 80GG in their individual capacity, provided all other conditions are met. However, the partnership firm itself cannot claim this deduction.

Condition 2: The Individual Must Pay Rent for Residential Accommodation

The rent must be paid for accommodation used as the individual’s residence. This includes rent for a house, apartment, flat, or any dwelling unit. The accommodation can be furnished or unfurnished. The key requirement is that the individual must actually be paying rent - notional rent or imputed rent does not qualify.

What qualifies as “rent”: Regular monthly payments to a landlord for the use of residential premises. Hostel fees, paying guest (PG) accommodation charges, and service apartment rentals can also qualify if the arrangement is residential in nature and there is a clear landlord-tenant or licensor-licensee relationship.

What does not qualify: Mortgage payments (you are buying, not renting), rent for commercial or business premises, rent for a second or vacation home (the accommodation must be your primary residence at the place of employment or business).

Condition 3: The Individual Must Not Receive HRA

This is the most critical condition and the one that most commonly disqualifies claims. If the individual’s employer pays House Rent Allowance (HRA) as a component of salary - even if the individual does not actually claim the HRA exemption under Section 10(13A) - Section 80GG is not available.

The nuance: The test is whether HRA is paid by the employer, not whether the employee claims the exemption. An employee who receives Rs 1 of HRA in their salary structure cannot claim 80GG, even if they do not claim the 10(13A) exemption on that Rs 1. Conversely, an employee whose salary does not include any HRA component can claim 80GG even if their salary is otherwise high.

Practical scenarios where 80GG is available:

- A self-employed doctor running a private clinic with no employer

- A freelance software consultant paid on a project basis with no salary structure

- A partner in a CA firm who draws a share of profit (not salary)

- A salaried employee of a small business whose offer letter and pay slip show no HRA component

- A retired person receiving pension (pension does not include HRA)

- A gig economy worker (Uber driver, food delivery rider, etc.) with no formal employment

Practical scenarios where 80GG is NOT available:

- A salaried employee receiving HRA of Rs 5,000 per month (even if not claiming 10(13A) exemption)

- An employee on a CTC structure where HRA is a component (even if the actual amount is minimal)

- An individual who receives HRA for part of the year (80GG is proportionally unavailable for those months)

Condition 4: Non-Ownership of Residential Property

This condition has three aspects, all of which must be satisfied:

4a. The individual must not own residential accommodation at the place of employment or business. If you are a freelancer working from Bengaluru and you own a flat in Bengaluru (even if you rent a different flat in Bengaluru), Section 80GG is not available. The ownership at the place of work completely disqualifies the deduction.

4b. The individual’s spouse must not own residential accommodation at the place of employment or business. If your spouse owns a house in the city where you work, you cannot claim 80GG.

4c. The individual’s minor child must not own residential accommodation at the place of employment or business. Property owned by minor children (which is effectively family property) also disqualifies.

4d. Any HUF of which the individual is a member must not own residential accommodation at these places. This is a broader test that covers property owned by the Hindu Undivided Family.

Important Interpretation - “At the Place of Employment”:

The non-ownership condition applies at the place of employment or business. If a freelancer works in Bengaluru and owns a house in their hometown (say, Lucknow), the ownership in Lucknow does not disqualify 80GG because Lucknow is not the place of employment. This interpretation has been confirmed in several ITAT (Income Tax Appellate Tribunal) decisions.

However, there is an additional limb: the individual must also not own property “at any other place, the particulars of which are specified in Form 10BA.” This effectively means that if you own property anywhere and do not declare it in Form 10BA, and the Assessing Officer discovers the ownership, the deduction may be disallowed. The practical approach is: if you own any residential property, consult a tax professional before claiming 80GG.

Agricultural Land: Ownership of agricultural land (which is not residential accommodation) does not affect 80GG eligibility. Similarly, ownership of commercial property (office, shop) does not disqualify the deduction - the condition pertains only to residential accommodation.

Condition 5: Filing of Form 10BA

Form 10BA is a mandatory declaration that must be filed along with the income tax return. The declaration states that the individual does not own residential accommodation at the place of employment or business. Without Form 10BA, the deduction can be disallowed even if all substantive conditions are met.

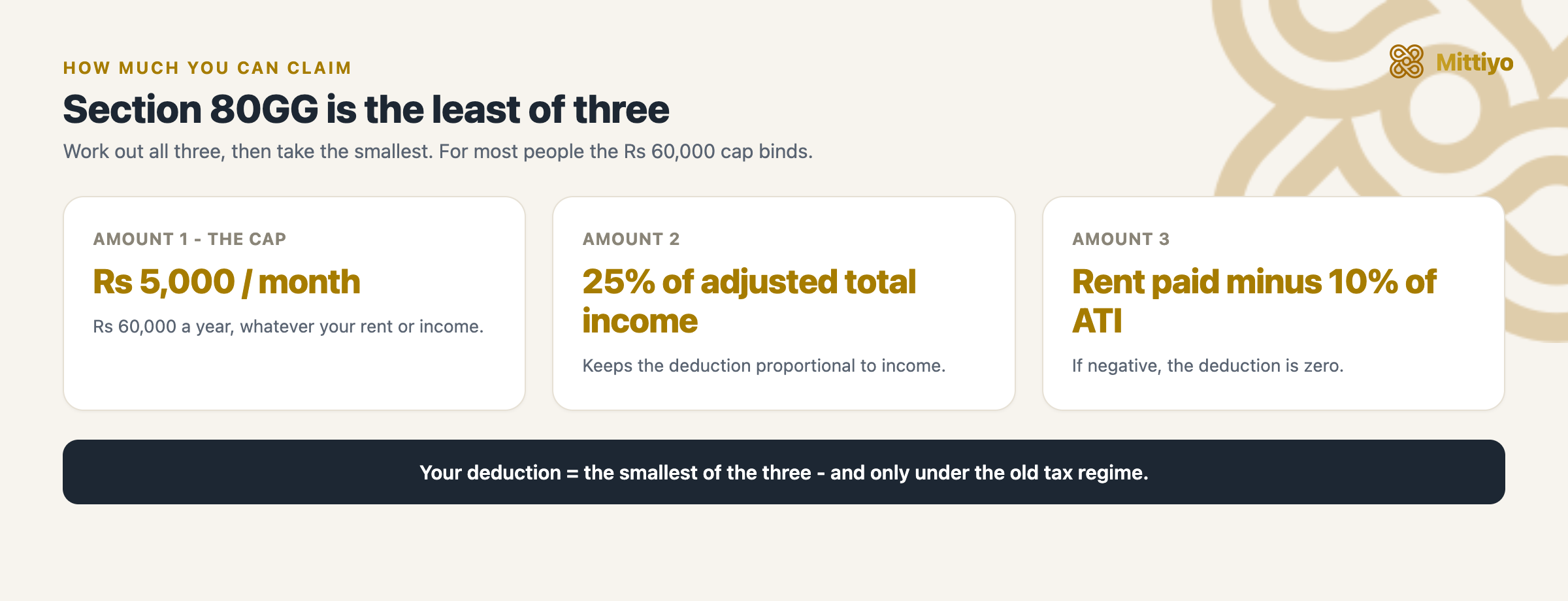

Calculation Methodology

The deduction under Section 80GG is computed under Rule 11B of the Income Tax Rules as the least of three amounts.

Your 80GG deduction is the smallest of these three.

Your 80GG deduction is the smallest of these three.

The Three Amounts

Amount 1: Rs 5,000 Per Month (Rs 60,000 Per Year)

This is the absolute cap. Regardless of how much rent you pay or how high your income is, the Section 80GG deduction cannot exceed Rs 60,000 per year. For part-year claims (for example, if you moved into the rented accommodation mid-year), the cap is proportionate - Rs 5,000 multiplied by the number of months of rental.

Amount 2: 25% of Adjusted Total Income

Adjusted Total Income (ATI) is defined as gross total income minus all deductions under Sections 80C through 80U except 80GG. In other words, compute your total income, apply all other Chapter VI-A deductions (80C, 80D, 80E, etc.), and 25% of the resulting figure is Amount 2.

The rationale for this limit is to ensure that the 80GG deduction is proportional to the taxpayer’s income. A very low-income individual should not get a deduction that exceeds a reasonable proportion of their income.

Amount 3: Actual Rent Paid Minus 10% of Adjusted Total Income

This is the “excess rent” computation. The logic is that you can deduct only the rent that exceeds 10% of your income - the first 10% is considered the individual’s “normal” housing expense that does not warrant a deduction.

Amount 3 = Total rent paid during the year - (10% x Adjusted Total Income)

If this amount is negative (i.e., the rent paid is less than 10% of ATI), the Amount 3 is zero, and therefore the overall deduction is zero. This means that individuals with high incomes relative to their rent cannot claim 80GG.

Worked Examples

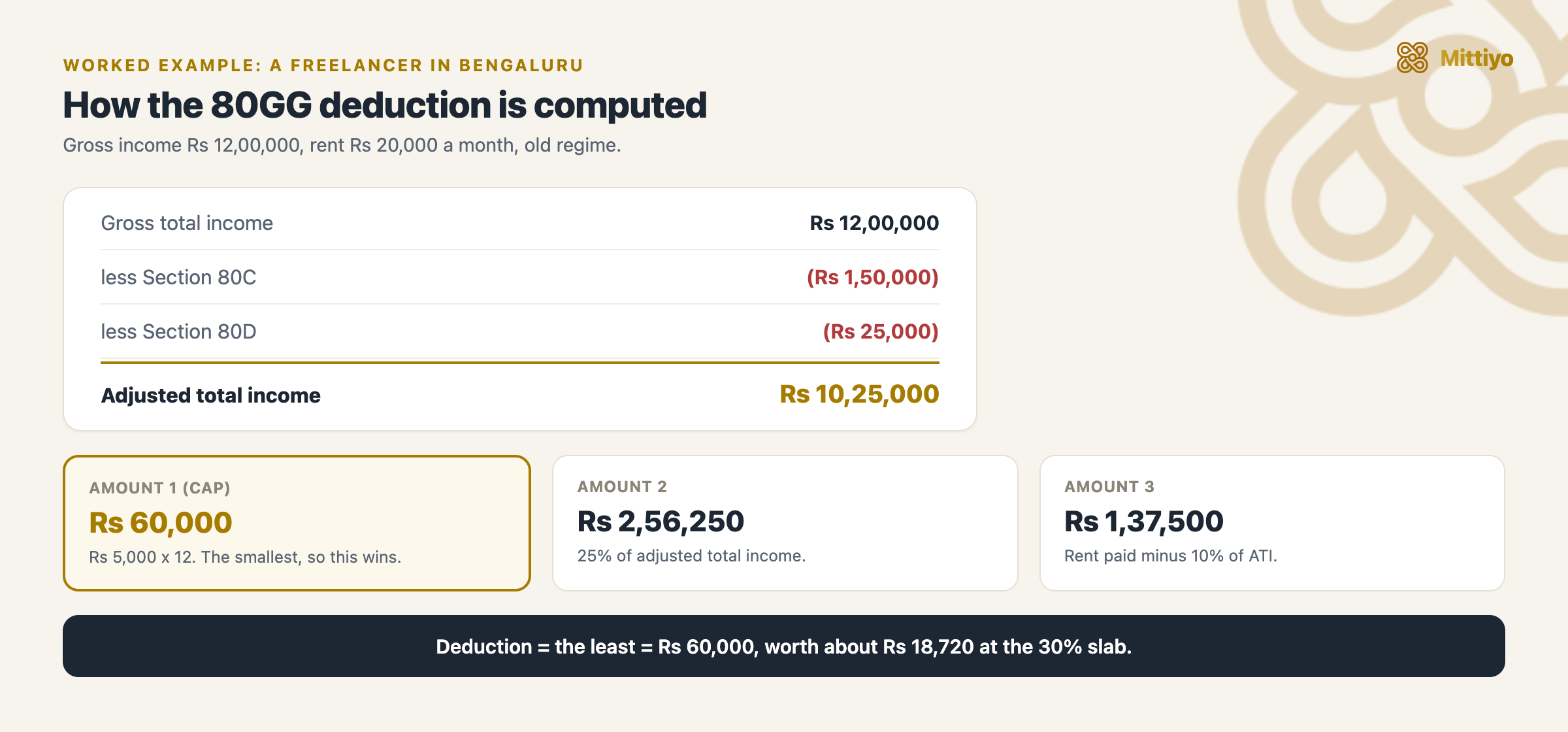

Example 1: Freelance Software Consultant in Bengaluru

The same example, visualised; the full numbers are in the table below.

The same example, visualised; the full numbers are in the table below.

| Detail | Amount |

|---|---|

| Gross total income | Rs 12,00,000 |

| Section 80C deduction (PPF, ELSS) | Rs 1,50,000 |

| Section 80D deduction (health insurance) | Rs 25,000 |

| Adjusted Total Income (ATI) | Rs 10,25,000 |

| Annual rent paid (Rs 20,000/month) | Rs 2,40,000 |

| Amount 1: Rs 5,000 x 12 | Rs 60,000 |

| Amount 2: 25% of Rs 10,25,000 | Rs 2,56,250 |

| Amount 3: Rs 2,40,000 - (10% x Rs 10,25,000) | Rs 1,37,500 |

| Deduction (least of three) | Rs 60,000 |

The binding constraint is Amount 1 (the Rs 60,000 cap). At the 30% tax bracket, this deduction saves Rs 18,720 in tax (including cess).

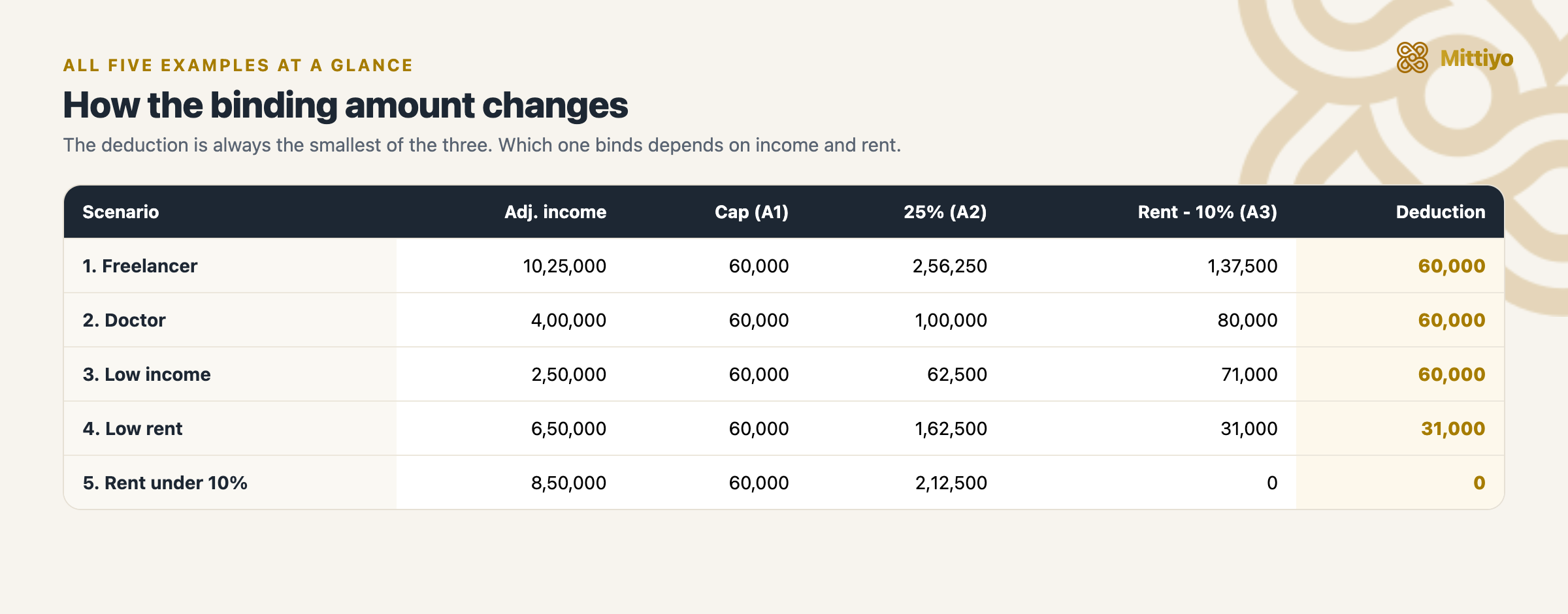

Example 2: Self-Employed Doctor with Moderate Income

| Detail | Amount |

|---|---|

| Gross total income | Rs 5,00,000 |

| Section 80C deduction | Rs 1,00,000 |

| Adjusted Total Income (ATI) | Rs 4,00,000 |

| Annual rent paid (Rs 10,000/month) | Rs 1,20,000 |

| Amount 1: Rs 5,000 x 12 | Rs 60,000 |

| Amount 2: 25% of Rs 4,00,000 | Rs 1,00,000 |

| Amount 3: Rs 1,20,000 - (10% x Rs 4,00,000) | Rs 80,000 |

| Deduction (least of three) | Rs 60,000 |

Again, Amount 1 is the binding constraint.

Example 3: Low-Income Freelancer

| Detail | Amount |

|---|---|

| Gross total income | Rs 3,00,000 |

| Section 80C deduction | Rs 50,000 |

| Adjusted Total Income (ATI) | Rs 2,50,000 |

| Annual rent paid (Rs 8,000/month) | Rs 96,000 |

| Amount 1: Rs 5,000 x 12 | Rs 60,000 |

| Amount 2: 25% of Rs 2,50,000 | Rs 62,500 |

| Amount 3: Rs 96,000 - (10% x Rs 2,50,000) | Rs 71,000 |

| Deduction (least of three) | Rs 60,000 |

Example 4: Scenario Where Amount 3 Is the Binding Constraint

| Detail | Amount |

|---|---|

| Gross total income | Rs 8,00,000 |

| Section 80C deduction | Rs 1,50,000 |

| Adjusted Total Income (ATI) | Rs 6,50,000 |

| Annual rent paid (Rs 8,000/month) | Rs 96,000 |

| Amount 1: Rs 5,000 x 12 | Rs 60,000 |

| Amount 2: 25% of Rs 6,50,000 | Rs 1,62,500 |

| Amount 3: Rs 96,000 - (10% x Rs 6,50,000) | Rs 31,000 |

| Deduction (least of three) | Rs 31,000 |

Here, the rent paid is relatively low compared to income, so Amount 3 becomes the binding constraint.

Example 5: Scenario Where Deduction Is Zero

| Detail | Amount |

|---|---|

| Gross total income | Rs 10,00,000 |

| Section 80C deduction | Rs 1,50,000 |

| Adjusted Total Income (ATI) | Rs 8,50,000 |

| Annual rent paid (Rs 5,000/month) | Rs 60,000 |

| Amount 1: Rs 5,000 x 12 | Rs 60,000 |

| Amount 2: 25% of Rs 8,50,000 | Rs 2,12,500 |

| Amount 3: Rs 60,000 - (10% x Rs 8,50,000) | Negative (Rs -25,000) = Rs 0 |

| Deduction (least of three) | Rs 0 |

When annual rent is less than 10% of ATI, no deduction is available under 80GG.

The five scenarios at a glance: the smallest of the three amounts always wins.

The five scenarios at a glance: the smallest of the three amounts always wins.

Form 10BA: The Mandatory Declaration

What Is Form 10BA?

Form 10BA is a prescribed declaration under Rule 11B, required to be furnished by any individual claiming a deduction under Section 80GG. The declaration confirms that the individual satisfies the ownership conditions - specifically, that neither the individual, their spouse, their minor child, nor any HUF of which they are a member owns residential accommodation at the place of employment, business, or ordinary residence.

How to File Form 10BA

Form 10BA is filed electronically through the Income Tax Department’s e-filing portal (incometax.gov.in).

Step-by-step process:

- Log in to the e-filing portal with your PAN and password.

- Navigate to e-File > Income Tax Forms > Form 10BA.

- Select the relevant assessment year.

- Fill in the required details: your name, PAN, address, the address of the rented premises, the landlord’s name and address, the landlord’s PAN (if available), the monthly rent amount, and the period for which rent was paid.

- Declare that you do not own residential accommodation at the specified places.

- Submit the form electronically. A receipt is generated as confirmation.

Timing: Form 10BA should be filed before or along with the income tax return for the relevant assessment year. Filing it after the ITR may create complications if the Assessing Officer reviews the claim.

Consequences of Not Filing Form 10BA

If Form 10BA is not filed, the Assessing Officer can disallow the Section 80GG deduction. Several ITAT decisions have upheld the disallowance of 80GG claims where Form 10BA was not filed, holding that it is a mandatory procedural requirement, not a mere formality.

However, some tribunals have taken a more liberal view, allowing the deduction where the substantive conditions were met and the failure to file Form 10BA was inadvertent. The safer course is to always file Form 10BA.

Tax Regime Consideration: Old vs. New

The Critical Distinction

Section 80GG is available ONLY under the old tax regime. Under the new tax regime introduced by Section 115BAC, all Chapter VI-A deductions (including Section 80GG) are unavailable, except for the employer’s contribution to NPS under Section 80CCD(2).

Since FY 2023-24 (Assessment Year 2024-25), the new tax regime under Section 115BAC is the default regime. Taxpayers who wish to use the old regime must actively opt for it. This means that Section 80GG is now available only to taxpayers who consciously choose the old tax regime.

Regime Comparison for Self-Employed Individuals

For self-employed individuals (who are the primary beneficiaries of 80GG), the regime choice involves comparing the tax liability under both regimes.

Old Regime Advantages:

- Access to Section 80GG (up to Rs 60,000)

- Access to Section 80C (up to Rs 1,50,000 for PPF, ELSS, etc.)

- Access to Section 80D (health insurance premium)

- Access to other Chapter VI-A deductions

- Standard deduction of Rs 50,000 (for salaried; not applicable to self-employed)

New Regime Advantages:

- Lower tax slab rates (particularly beneficial at higher income levels)

- Simpler compliance - no need to track and prove deductions

- Higher basic exemption limit (Rs 4,00,000 under the new regime for FY 2025-26)

- Tax rebate under Section 87A that makes income up to Rs 12,00,000 effectively tax-free (FY 2025-26), plus a Rs 75,000 standard deduction for salaried taxpayers

Break-even Analysis:

The regime choice depends on the total value of deductions available to the individual. As a general rule, if total Chapter VI-A deductions (including 80GG) plus any applicable exemptions exceed approximately Rs 2,00,000 to Rs 3,75,000 (depending on the income level), the old regime may be more beneficial. At lower total deductions, the new regime’s lower slab rates typically produce a lower tax liability.

A self-employed individual paying significant rent should compute their tax liability under both regimes before filing. The Income Tax Department’s online utility and most tax filing software provide a regime comparison tool.

Regime Choice Mechanics for Self-Employed

For self-employed individuals (without salary income), the regime choice is made at the time of filing the ITR. Unlike salaried individuals (who must inform their employer of the regime choice), self-employed individuals can choose the regime each year independently.

Form 10-IEA: Because the new regime is now the default, a self-employed individual with business or professional income who wants the old regime (to claim 80GG) must file Form 10-IEA before the ITR due date. This form replaced the older Form 10-IE from AY 2024-25. Taxpayers without business or professional income do not need the form; they simply select the old regime in the ITR itself. Note that for those with business income, switching back and forth between regimes is restricted, so make the choice deliberately.

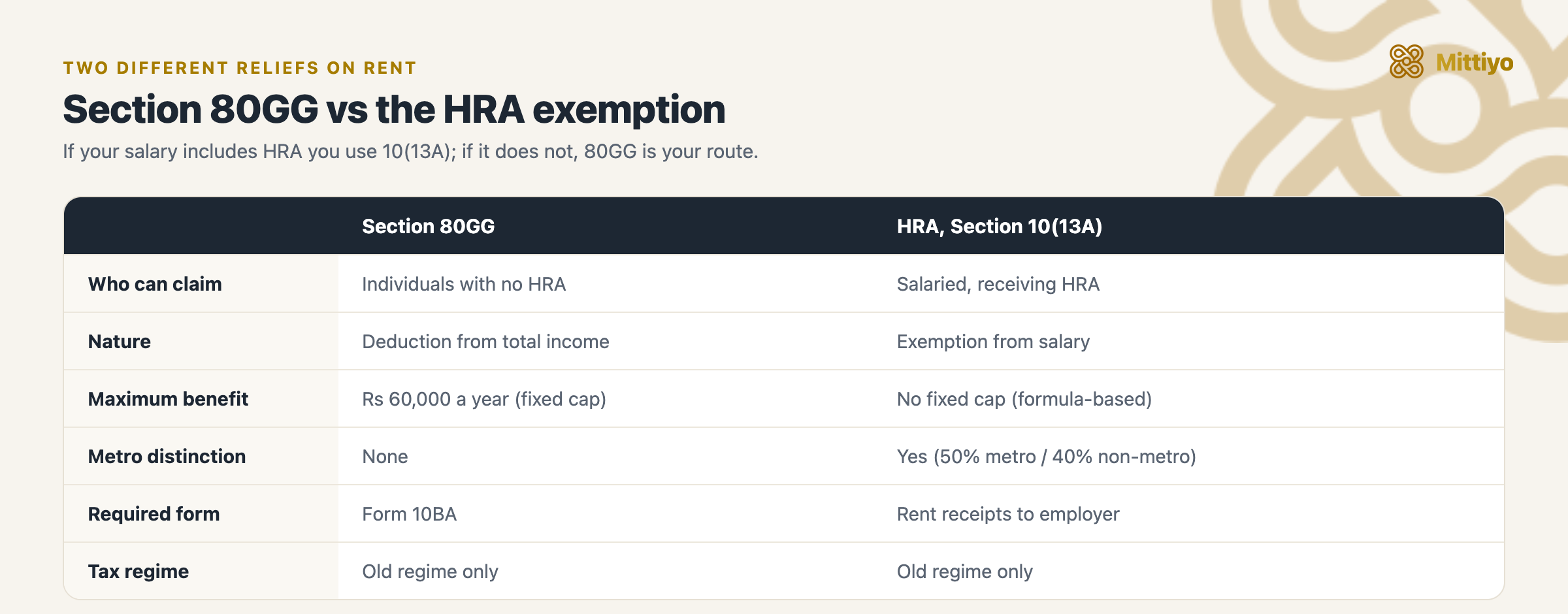

Section 80GG vs. Section 10(13A) HRA Exemption

Understanding the differences between these two provisions helps taxpayers identify which one applies to their situation and appreciate the relative advantages and limitations of each.

Section 80GG versus the HRA exemption, side by side.

Section 80GG versus the HRA exemption, side by side.

| Feature | Section 80GG | Section 10(13A) HRA Exemption |

|---|---|---|

| Who can claim | Individuals NOT receiving HRA | Salaried employees receiving HRA |

| Nature | Deduction from gross total income | Exemption from salary income |

| Maximum benefit | Rs 60,000 per year (fixed cap) | No fixed cap (formula-based, scales with salary and rent) |

| Metro distinction | None - same calculation everywhere | Yes - 50% of basic salary for metros, 40% for non-metros |

| Required form | Form 10BA (declaration of non-ownership) | Rent receipts and rental agreement submitted to employer |

| Property ownership | Must not own residential property at the place of employment | Can own property at other locations (not at the same city for maximum benefit) |

| Tax regime | Old regime only | Old regime only |

| Calculation inputs | Adjusted total income, rent paid | Basic salary, HRA received, rent paid, metro/non-metro |

Key Observation: The HRA exemption is significantly more generous than Section 80GG for most taxpayers. An employee in a metro city with a basic salary of Rs 40,000 per month and paying Rs 20,000 per month in rent could claim an HRA exemption of approximately Rs 1,80,000 per year. The same individual, if they did not receive HRA, could claim only Rs 60,000 under Section 80GG. This disparity reflects the historical policy design where Section 80GG was introduced as a limited safety net, not a full equivalence to HRA exemption.

Documentation and Record-Keeping

Documents to Maintain

1. Rent Receipts: Monthly receipts from the landlord confirming receipt of rent. Each receipt should include the tenant’s name, landlord’s name, property address, amount received, month of rent, date of receipt, and landlord’s signature. For rent amounts exceeding Rs 5,000 per month, a revenue stamp on the receipt was traditionally required, though this practice has diminished with digital payments.

2. Rental Agreement: A written rental agreement showing the parties, property address, rent amount, and tenure. The agreement corroborates the rent receipts and establishes the legitimacy of the rental arrangement.

3. Bank Statements: Bank transfer records (NEFT, IMPS, UPI) showing monthly rent payments. Bank transfers are the strongest proof of actual rent payment - they show the amount, date, and recipient. Cash payments, while valid, are harder to prove and may attract scrutiny.

4. Landlord’s PAN: If the total annual rent exceeds Rs 1,00,000, the tenant is required to report the landlord’s PAN in the income tax return. If the landlord does not have a PAN, a declaration to that effect from the landlord should be obtained.

5. Form 10BA: Filed electronically with the ITR. Keep a copy of the submission receipt.

6. Proof of Non-Ownership: While not required during filing, maintain property-related documents (or their absence) to demonstrate that you do not own residential property at the place of employment. If you do own property elsewhere, maintain records showing it is not at the place of employment or ordinary residence.

TDS on Rent Paid: Section 194-IB

An important compliance obligation for tenants paying rent exceeding Rs 50,000 per month: Section 194-IB requires the tenant to deduct TDS at the rate of 2 percent on the rent amount. The TDS must be deducted in the last month of the tenancy during the financial year (or the last month of the financial year if the tenancy continues beyond March).

Key Details:

- TDS rate: 2% (reduced from 5% by the Finance (No. 2) Act, 2024, effective from October 1, 2024)

- Applies when monthly rent exceeds Rs 50,000

- The tenant deducts TDS on the total rent paid during the year (or the applicable period)

- TDS is deposited using Form 26QC on the income tax e-filing portal (incometax.gov.in)

- A TDS certificate (Form 16C) is issued to the landlord

- The tenant does not need a TAN (Tax Deduction and Collection Account Number) for this purpose

Connection to 80GG: While TDS under 194-IB and the 80GG deduction are independent provisions, compliance with 194-IB demonstrates the legitimacy of the rent payment, which indirectly supports the 80GG claim. Non-compliance with 194-IB (when applicable) may attract penalties and also cast doubt on the rental arrangement’s genuineness.

Common Mistakes and Pitfalls

Mistake 1: Claiming Both 80GG and HRA

This is the most common error. If your salary includes an HRA component - even a minimal amount - you cannot claim 80GG. The test is receipt of HRA, not claim of HRA exemption. Check your pay slip carefully. If HRA is listed as a salary component (even at Rs 500 or Rs 1,000 per month), Section 80GG is not available.

Partial Year Scenario: If you changed jobs during the year and received HRA for 6 months (from the old employer) but not for the remaining 6 months (from the new employer or during a gap), you can claim 80GG only for the months when you did not receive HRA. The calculation should be proportional.

Mistake 2: Owning Property at the Place of Employment

If you own a flat in Bengaluru and also rent another flat in Bengaluru, you cannot claim 80GG. The non-ownership condition is specific to the place of employment or business. Owning property in another city does not automatically disqualify you, but the Form 10BA declaration must be accurate.

Mistake 3: Not Filing Form 10BA

The deduction can be disallowed purely on the procedural ground that Form 10BA was not filed. This is an easily avoidable mistake - file the form along with (or before) the ITR.

Mistake 4: Claiming Under the New Tax Regime

Section 80GG is not available under the new tax regime (Section 115BAC). If you have opted for the new regime (or defaulted into it), claiming 80GG will be disallowed upon processing or assessment. Verify your regime choice before claiming.

Mistake 5: Paying Rent to Spouse

Rent paid to your spouse is not eligible for the Section 80GG deduction. The Income Tax Department considers this a non-arm’s-length transaction - the payment circulates within the family unit without a genuine change in economic position. This principle has been upheld in multiple ITAT decisions.

Exception - Rent Paid to Parents: Rent paid to parents is eligible for 80GG, provided the parents actually own the property, the parents declare the rental income in their tax returns, and the arrangement is genuine (not a colorable device to claim the deduction). Several ITAT decisions have allowed 80GG claims where the taxpayer rented from their parents and the arrangement was genuine.

Mistake 6: Inadequate Documentation

Claims supported only by self-declarations or unsigned rent receipts are vulnerable to disallowance during assessment. Bank transfer records, signed rent receipts, the rental agreement, and the landlord’s PAN (if rent exceeds Rs 1,00,000 per year) collectively establish the legitimacy of the claim.

Mistake 7: Incorrect ATI Calculation

The Adjusted Total Income calculation requires excluding the 80GG deduction itself but including all other deductions. Errors in the ATI calculation cascade into the Amount 2 and Amount 3 computations, potentially resulting in an incorrect deduction amount.

Judicial Interpretations

Several Income Tax Appellate Tribunal (ITAT) and High Court decisions have clarified aspects of Section 80GG.

On Form 10BA Filing: In cases where the assessee failed to file Form 10BA but met all substantive conditions, some ITAT benches have allowed the deduction, holding that the substantive requirements take precedence over procedural formalities when there is no prejudice to revenue. However, this is not a settled position, and relying on it is risky.

On Property Ownership at Other Locations: The ITAT has consistently held that ownership of residential property at a location other than the place of employment does not disqualify 80GG, provided the property is not at a place where the assessee ordinarily resides.

On “Place of Employment” for Freelancers: For self-employed individuals who work from home or from multiple locations, the “place of employment” is interpreted as the place where the individual primarily carries on their profession or business. For a freelancer who works from home in Bengaluru, Bengaluru is the place of employment.

Key Takeaways

- Section 80GG provides a rent deduction for individuals who pay rent but do not receive HRA. The maximum deduction is Rs 60,000 per year (Rs 5,000 per month).

- The deduction is available to self-employed professionals, freelancers, gig workers, business owners, and salaried employees without HRA. Companies and HUFs cannot claim it.

- The deduction is the least of three amounts: Rs 5,000 per month, 25% of adjusted total income, and actual rent paid minus 10% of adjusted total income. For most taxpayers, the Rs 60,000 cap is the binding constraint.

- You must not own residential property at the place of employment or business. Ownership by spouse, minor child, or HUF also disqualifies.

- Form 10BA (declaration of non-ownership) is mandatory and must be filed electronically with the income tax return on the e-filing portal.

- Section 80GG is available only under the old tax regime. Under the new tax regime (Section 115BAC), this deduction is not available. Compute tax under both regimes before choosing.

- Rent paid to spouse is ineligible. Rent paid to parents is eligible if the parents own the property and declare the rental income.

- If monthly rent exceeds Rs 50,000, the tenant must deduct TDS at 2% under Section 194-IB and deposit it using Form 26QC.

- Maintain rent receipts, bank transfer records, the rental agreement, and the landlord’s PAN (if rent exceeds Rs 1,00,000) as documentation. Bank transfers are the strongest proof of payment.

- If you receive HRA even for part of the year, you cannot claim 80GG for those months. The test is receipt of HRA, not claim of HRA exemption.

Renting without HRA?

When rent is your own deduction to claim, paying a fair price matters even more. Before you commit to a place, see what residents say a building actually rents for, the deposit, the society, the infrastructure around it, on know.place, a map of honest, building-level rental reviews across India.

Explore know.placeThis guide is general information, not personalised tax advice; confirm your own position with a qualified chartered accountant or tax adviser.

Related guides: HRA exemption (if your salary includes HRA) · Rent receipts for tax · TDS on rent (Section 194-IB)

References

Unless noted, all section references are to the Income Tax Act, 1961.

- Section 80GG - deduction in respect of rents paid

- Income Tax Rules, 1962, Rule 11B - computation of the Section 80GG deduction

- Section 10(13A) - House Rent Allowance exemption

- Section 115BAC - new tax regime; Chapter VI-A deductions (including 80GG) unavailable

- Section 194-IB - TDS on rent paid by individuals and HUFs

- Sections 80C and 80D - other Chapter VI-A deductions referenced in the examples

- Finance Act, 2016 - Section 80GG limit raised from Rs 2,000 to Rs 5,000 per month

- Finance (No. 2) Act, 2024 - Section 194-IB TDS rate cut from 5% to 2%, effective 1 October 2024

- Form 10BA - declaration under Section 80GG (filed on the e-filing portal)

- Form 10-IEA - opt for the old regime (business or profession income); replaced Form 10-IE from AY 2024-25

- Form 26QC - TDS challan-cum-statement for rent under Section 194-IB