Tax Deducted at Source (TDS) on rent is one of the most commonly overlooked tax compliance obligations for tenants in India. If your monthly rent exceeds Rs 50,000, you are legally required to deduct a portion of the rent as tax before paying your landlord and deposit it with the government. Failure to comply exposes you to interest charges, penalties, and the risk of being treated as an “assessee in default” by the Income Tax Department.

Despite the obligation being straightforward in principle, the practical details, calculating the correct amount, understanding rate changes, filing the right forms, handling NRI landlords, and navigating shared tenancy situations, create confusion. This guide provides a complete, step-by-step analysis of TDS on rent under Section 194-IB, the special rules for NRI landlords under Section 195, and the compliance process from deduction to certificate issuance.

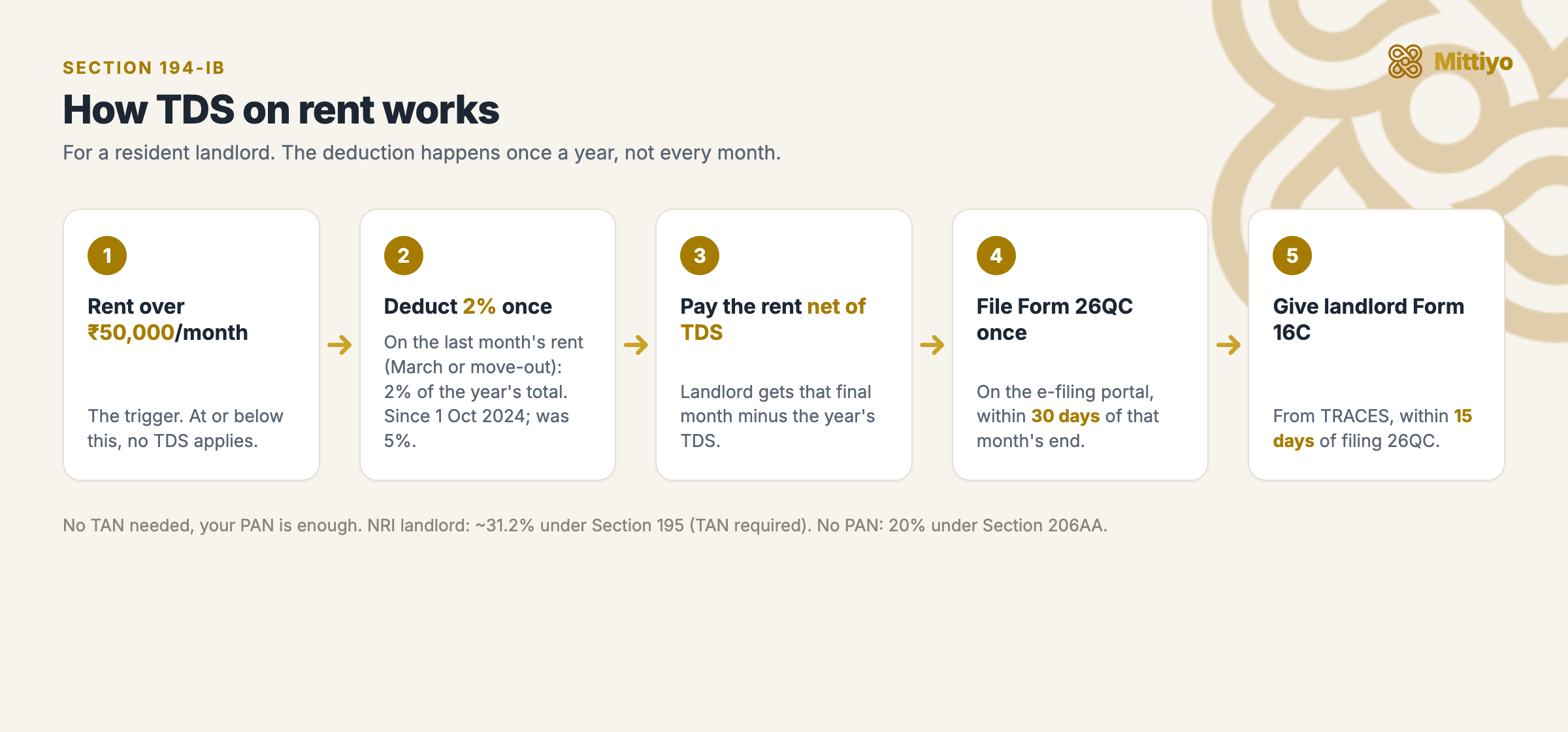

The end-to-end process for a resident landlord, at a glance.

The end-to-end process for a resident landlord, at a glance.

Understanding the Legal Framework

The Origin and Purpose of Section 194-IB

Section 194-IB was introduced by the Finance Act, 2017, effective from June 1, 2017. Before this provision, only companies, firms, and individuals/HUFs subject to tax audit were required to deduct TDS on rent (under Section 194-I). This meant that a large volume of rental transactions, involving individual tenants paying substantial rents in metro cities, escaped the TDS net entirely.

Section 194-IB was specifically designed to bring individual and HUF tenants into the TDS framework for high-value rentals, without imposing the full compliance burden of Section 194-I (which requires a TAN, quarterly returns, and more detailed reporting).

Who Must Deduct TDS on Rent?

The obligation under Section 194-IB applies to a specific category of tenants:

| Category of Tenant | Monthly Rent Threshold | TDS Required? | Applicable Section |

|---|---|---|---|

| Individual (not subject to tax audit) | > Rs 50,000 | Yes | 194-IB |

| HUF (not subject to tax audit) | > Rs 50,000 | Yes | 194-IB |

| Individual/HUF subject to tax audit | Any amount | Yes | 194-I (not 194-IB) |

| Company or firm | Any amount | Yes | 194-I |

| Individual | Rs 50,000 or less | No | Not applicable |

Key distinctions:

- Section 194-IB applies only to individuals and HUFs who are not required to get their accounts audited under Section 44AB

- If you are a salaried individual paying rent exceeding Rs 50,000 per month, Section 194-IB applies to you

- If you are a self-employed professional or business owner whose turnover exceeds the audit threshold, your TDS obligation falls under Section 194-I instead, which has different rates and compliance requirements

- The Rs 50,000 threshold is per month, not per annum

The TAN Exemption

One of the most significant features of Section 194-IB is that the tenant does not need to obtain a Tax Deduction Account Number (TAN) to comply. Under Section 194-I, deductors must obtain a TAN, file quarterly TDS returns (Form 27Q), and maintain detailed records. Section 194-IB eliminates this burden, the tenant’s PAN is sufficient for filing Form 26QC and depositing the TDS.

This exemption was a deliberate design choice. The government recognized that requiring individual tenants to obtain TANs and file quarterly returns would create a disproportionate compliance burden. The simplified process under Section 194-IB (annual filing via Form 26QC, PAN-based identification) achieves compliance with minimal administrative overhead.

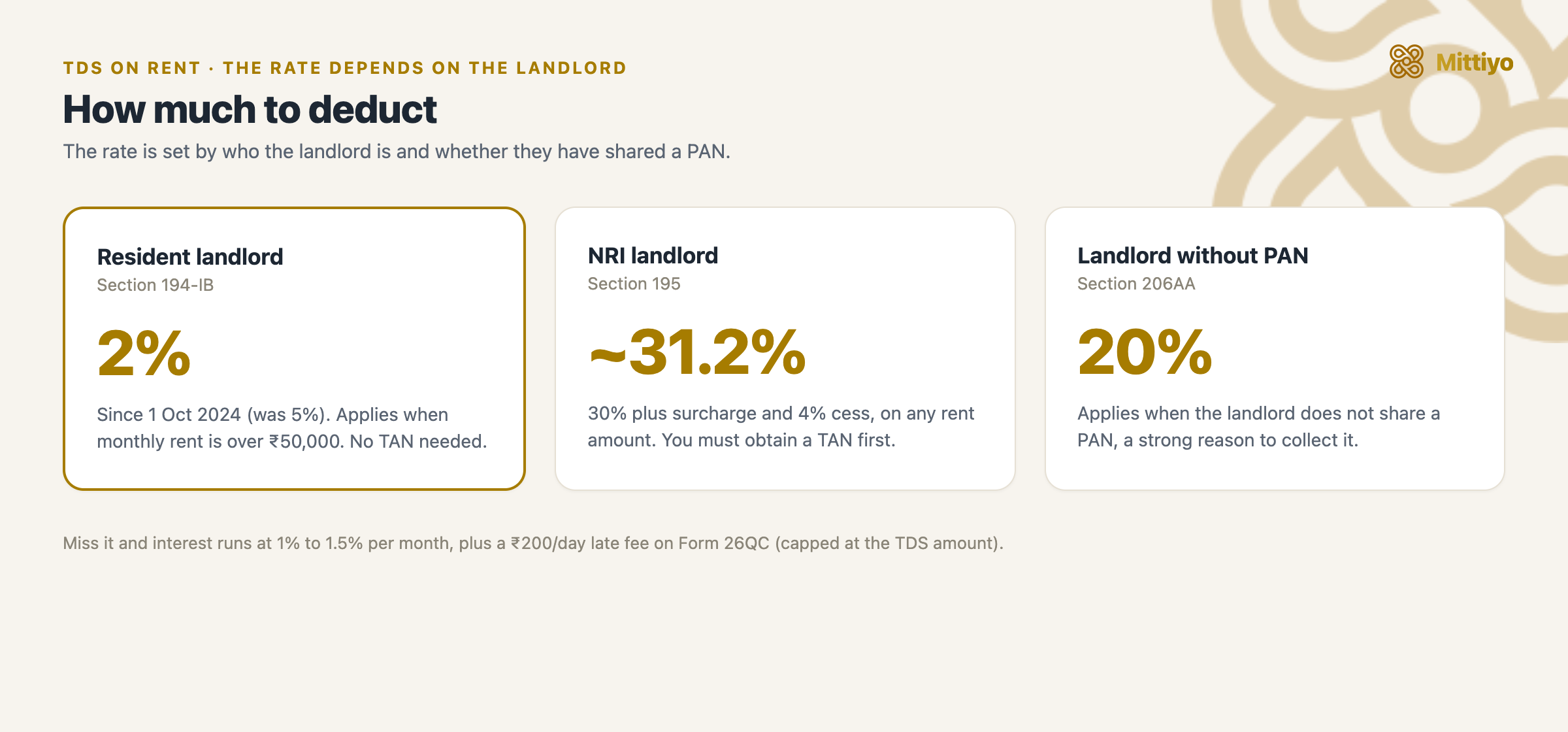

How Much TDS Do You Deduct on Rent? The Current Rate

The Finance (No. 2) Act, 2024 introduced a significant change to the TDS rate under Section 194-IB, reducing it from 5% to 2% with effect from October 1, 2024. This rate reduction was part of a broader rationalization of TDS rates across multiple sections.

The rate depends entirely on who the landlord is.

The rate depends entirely on who the landlord is.

| Landlord Type | TDS Rate | Effective Period | Legal Basis |

|---|---|---|---|

| Resident Indian | 2% | October 1, 2024 onwards | Finance (No. 2) Act, 2024 |

| Resident Indian | 5% | June 1, 2017 to September 30, 2024 | Original Section 194-IB |

| NRI landlord | ~31.2% | Current | Section 195 (30% + surcharge + 4% cess) |

Implications of the Rate Change

The rate is fixed by when you deduct, not by each month of the tenancy. Because Section 194-IB is deducted once, on the last month’s rent (explained below), the rate that applies is the one in force on that deduction date. A deduction made on or after October 1, 2024 is at 2%; one made before that date is at 5%.

For the financial year 2024-25 (the transitional year): there is no need to split the year into a 5% slice and a 2% slice. If your tenancy continued to March 2025, the deduction falls in March 2025, so the entire amount is at 2%. Only if you vacated before October 1, 2024, so the deduction fell in, say, September 2024, does the 5% rate apply to that deduction.

For FY 2025-26 (the year being filed this season) and FY 2026-27 (the current year): the rate is a flat 2% for resident landlords in both, on the same Rs 50,000-per-month threshold. The whole of each year falls after the October 2024 change, so there is no transitional split to worry about. Budget 2025 raised the threshold under Section 194-I (which covers companies and audited businesses) to Rs 6,00,000 a year, but left Section 194-IB for individual and HUF tenants untouched, so the 2% rate and the Rs 50,000-per-month trigger continue unchanged.

If you over-deducted at 5%: tenants who withheld 5% on a deduction made on or after October 1, 2024 have over-deducted. The excess can be corrected in the Form 26QC filing, or the landlord can claim it back when filing their ITR.

How to Calculate TDS: Detailed Examples

Example 1: Standard Case, Monthly Rent Rs 60,000 to Resident Landlord

Rent is Rs 60,000 a month for the full financial year. The TDS is 2% of the total rent for the year, and you deduct it once, from the final (March) payment, not a slice each month.

| Component | Calculation | Amount |

|---|---|---|

| Annual rent (12 months) | Rs 60,000 x 12 | Rs 7,20,000 |

| Total TDS at 2% | Rs 7,20,000 x 2% | Rs 14,400 |

| Rent paid in full, April to February | Rs 60,000 x 11 | Rs 6,60,000 |

| March rent paid to landlord | Rs 60,000 - Rs 14,400 | Rs 45,600 |

| Deposited with the government via Form 26QC | - | Rs 14,400 |

The single deduction of Rs 14,400 stays within the law’s cap, which limits it to one month’s rent (Section 194-IB(3)). At 2%, that cap is never reached.

Example 2: Shared Flat, Total Rent Rs 80,000, Two Tenants

This is one of the most commonly misunderstood scenarios. The TDS obligation depends on how the rental agreement is structured.

Scenario A, Single agreement, both tenants jointly liable: If the rental agreement is in both tenants’ names with a total rent of Rs 80,000/month, TDS applies because the total rent exceeds Rs 50,000. Each tenant deducts TDS on their share:

| Tenant | Rent Share | TDS at 2% | Pays Landlord |

|---|---|---|---|

| Tenant A | Rs 40,000 | Rs 800 | Rs 39,200 |

| Tenant B | Rs 40,000 | Rs 800 | Rs 39,200 |

| Total | Rs 80,000 | Rs 1,600 | Rs 78,400 |

Scenario B, Separate agreements, each below Rs 50,000: If each tenant has a separate agreement with the landlord for Rs 40,000/month, no TDS is required because each individual agreement is below the Rs 50,000 threshold. However, the Income Tax Department may scrutinize this arrangement if it appears to be structured solely to avoid TDS.

Scenario C, One tenant signs the agreement, sublets to the other: If Tenant A signs the agreement for Rs 80,000/month and collects Rs 40,000 from Tenant B informally, the TDS obligation falls entirely on Tenant A (who is the lessee under the agreement). Tenant A must deduct TDS at 2% on the full Rs 80,000.

Example 3: Monthly Rent Rs 75,000 to NRI Landlord

| Component | Calculation | Amount |

|---|---|---|

| Monthly rent | - | Rs 75,000 |

| TDS at 31.2% (Section 195) | Rs 75,000 x 31.2% | Rs 23,400 |

| Amount paid to landlord | Rs 75,000 - Rs 23,400 | Rs 51,600 |

| Annual TDS (12 months) | Rs 23,400 x 12 | Rs 2,80,800 |

Example 4: Landlord Without PAN, Section 206AA

When the landlord does not furnish a PAN, Section 206AA raises the rate to 20%. But the Section 194-IB cap still applies: the single deduction cannot exceed one month’s rent.

| Component | Calculation | Amount |

|---|---|---|

| Annual rent (12 months) | Rs 60,000 x 12 | Rs 7,20,000 |

| TDS at 20% (Section 206AA), before cap | Rs 7,20,000 x 20% | Rs 1,44,000 |

| Capped at one month’s rent (Section 194-IB(3)) | - | Rs 60,000 |

Because 20% of the annual rent (Rs 1,44,000) exceeds one month’s rent, the deduction is capped at Rs 60,000 and taken from the last month’s payment. Withholding almost a full month’s rent is a strong incentive for the landlord to share their PAN, which brings the rate back down to 2%.

Step-by-Step Compliance Process

Step 1: Determine Your Obligation

Before your first rent payment, determine:

- Is your monthly rent above Rs 50,000?

- Is your landlord a resident Indian or an NRI?

- Does the landlord have a PAN?

If the rent exceeds Rs 50,000 and the landlord is a resident Indian with PAN, Section 194-IB applies at 2%.

Step 2: Deduct TDS Once, on the Last Month’s Rent

This is the most misunderstood part of Section 194-IB. The Rs 50,000 test is applied per month, so people assume the deduction is monthly too. It is not. The monthly figure is only the trigger that decides whether you are covered; the deduction itself is annual.

Section 194-IB does not ask for a monthly deduction. You deduct the TDS once in the financial year, on the rent for the last month of the year (March), or the last month of the tenancy if you vacate earlier (Section 194-IB(2)). This is the opposite of Section 194-I, which businesses and audited landlords use, where TDS is deducted on every payment and a TAN and quarterly returns are required. The amount is the applicable rate applied to the total rent for the year (or for the months you occupied the property that year), and you withhold it from that final month’s payment.

For a full year at Rs 60,000 a month, that means paying the rent in full from April to February, then deducting Rs 14,400 (2% of Rs 7,20,000) from the March rent and paying the landlord the balance. The deduction can never exceed one month’s rent (Section 194-IB(3)), a cap that the 2% rate never reaches.

Timing: The deduction is triggered when the last month’s rent is credited or paid, whichever is earlier (Section 194-IB(2)). A practical habit is to set aside 2% each month so the single March deduction is not a surprise to either side, but the legal deduction and deposit happen once.

Documentation: Keep a record of:

- Date of rent payment

- Gross rent amount

- TDS amount deducted

- Net amount paid to landlord

- Mode of payment (bank transfer, UPI, cheque)

Step 3: File Form 26QC

Form 26QC is a combined challan-cum-statement specifically designed for TDS under Section 194-IB. It serves both as the tax payment instrument and the reporting form.

The Income Tax e-filing portal (incometax.gov.in), where Form 26QC is filed. Source: Income Tax Department, Government of India.

The Income Tax e-filing portal (incometax.gov.in), where Form 26QC is filed. Source: Income Tax Department, Government of India.

When to file: Form 26QC is filed once, within 30 days from the end of the month in which the TDS was deducted, that is, within 30 days of the end of March (or of the month you vacate). For a tenancy that runs the full year and ends in March, the due date is April 30.

How to file (step-by-step):

- Log in to the Income Tax e-filing portal at incometax.gov.in

- Navigate to e-File > e-Pay Tax

- Select Form 26QC (Payment of TDS on Rent of Property)

- Enter tenant details:

- PAN of the tenant (deductor)

- Name, address, email, and mobile number

- Category (individual or HUF)

- Enter landlord details:

- PAN of the landlord (deductee)

- Name and address

- Resident/NRI status

- Enter property and tenancy details:

- Address of the rented property

- Period of tenancy covered (start date to end date)

- Monthly rent amount

- Date of payment/credit

- Enter TDS details:

- Total rent paid during the period

- Total TDS deducted

- TDS rate applied (2% for resident, specify if different)

- Pay the TDS amount via net banking, debit card, or at authorized bank branches

- Submit and note the acknowledgment number

Common filing errors to avoid:

- Incorrect PAN of landlord (verify the PAN before filing, an incorrect PAN results in the TDS not being credited to the landlord’s account)

- Wrong assessment year selection

- Mismatch between the TDS amount calculated and the amount paid

- Filing for the wrong period

Step 4: Download and Issue Form 16C

After filing Form 26QC and paying the TDS, the next step is to generate and provide Form 16C to the landlord.

What is Form 16C? It is the TDS certificate issued by the tenant (deductor) to the landlord (deductee) as proof that TDS has been deducted and deposited with the government. The landlord uses Form 16C to claim credit for the TDS when filing their income tax return.

How to generate Form 16C:

- Register on the TRACES portal (tdscpc.gov.in) as a taxpayer (if not already registered)

- Log in to TRACES

- Navigate to Downloads > Form 16C

- Enter the acknowledgment number from Form 26QC filing

- Download Form 16C

- Verify the details (PAN, amount, period) for accuracy

- Provide to the landlord within 15 days of filing Form 26QC

Legal obligation: Providing Form 16C is not optional. Failure to issue Form 16C within the prescribed time attracts a penalty of Rs 100 per day under Section 272A(2)(g) of the Income Tax Act.

NRI Landlord: Special Rules Under Section 195

When your landlord is a Non-Resident Indian (NRI), the TDS framework shifts entirely from Section 194-IB to Section 195, with significantly different rates, procedures, and compliance requirements.

Why the Rules Differ for NRI Landlords

Section 195 applies to all payments made to non-residents that are chargeable to tax in India. Rental income from property situated in India is taxable in India regardless of the landlord’s residential status. Because the NRI may not file an Indian tax return or be easily reachable by Indian tax authorities, the TDS mechanism ensures tax collection at source with a higher withholding rate.

Key Differences: Resident vs NRI Landlord

| Factor | Resident Landlord (Section 194-IB) | NRI Landlord (Section 195) |

|---|---|---|

| TDS Rate | 2% | 30% + surcharge + 4% cess = ~31.2% |

| Rent Threshold | > Rs 50,000/month | Any amount (no threshold) |

| TAN Required | No (PAN sufficient) | Yes, tenant must obtain TAN |

| Filing Form | 26QC (annual/at termination) | 27Q (quarterly) |

| Filing Frequency | End of FY or end of tenancy | Every quarter |

| TDS Certificate | Form 16C | Form 16A |

| Lower rate possible? | No provision | Yes, LTDC from Assessing Officer |

| DTAA benefit available? | Not applicable | Yes, if applicable treaty exists |

Obtaining a TAN

If your landlord is an NRI, you must obtain a Tax Deduction Account Number (TAN) before the first TDS deduction. Apply online through the Protean (formerly NSDL) TIN portal using Form 49B. Processing typically takes 7-15 days and costs Rs 65 (plus GST).

Lower Tax Deduction Certificate (LTDC)

The ~31.2% TDS rate on NRI rental income can be very high, especially when the NRI landlord’s total Indian income (including rent) falls below the basic exemption limit or qualifies for relief under a Double Taxation Avoidance Agreement (DTAA).

How the LTDC works:

- The NRI landlord applies to the Assessing Officer under Section 197 for a certificate authorizing TDS at a lower rate (or nil rate)

- The Assessing Officer examines the NRI’s estimated total income, applicable deductions, and DTAA benefits

- If satisfied, the Assessing Officer issues a certificate specifying a lower TDS rate

- The tenant deducts TDS at the rate specified in the certificate instead of the standard ~31.2%

Practical tip: If your NRI landlord has obtained an LTDC, insist on seeing the original certificate and note the certificate number, the rate authorized, and the validity period. Deducting at a lower rate without a valid LTDC exposes you to liability for the shortfall plus interest.

DTAA Benefits

India has Double Taxation Avoidance Agreements with over 90 countries. Under these treaties, the NRI landlord may be entitled to a lower tax rate on rental income from India. Common treaty provisions include:

- Lower rates on immovable property income (though most DTAAs tax real property income in the country where the property is situated)

- Credit for Indian taxes paid against tax liability in the NRI’s country of residence

- Provisions for refund of excess TDS

The DTAA benefit does not automatically reduce the TDS rate. The NRI landlord must obtain an LTDC from the Assessing Officer to claim a lower rate at the withholding stage, or claim a refund when filing their Indian income tax return.

What Happens If You Do Not Deduct TDS on Rent?

The Income Tax Act imposes a graduated set of penalties for different types of TDS non-compliance:

| Violation | Consequence | Legal Basis |

|---|---|---|

| Not deducting TDS | Assessee in default, liable for TDS amount + interest at 1% per month | Sections 201(1) and 201(1A) |

| Deducting but not depositing | Interest at 1.5% per month from deduction date to deposit date | Section 201(1A)(ii) |

| Late filing of Form 26QC | Late fee of Rs 200 per day (Section 234E), capped at TDS amount | Section 234E |

| Not issuing Form 16C | Penalty of Rs 100 per day | Section 272A(2)(g) |

| Incorrect/short deduction | Interest at 1% per month on the shortfall amount | Section 201(1A)(i) |

| Failure to deduct (deliberate) | Penalty equal to the TDS amount not deducted | Section 271C |

The “Assessee in Default” Concept

When a tenant fails to deduct TDS as required, they are treated as an “assessee in default” under Section 201(1). This has significant consequences:

- The tenant becomes personally liable for the TDS amount (even though it was the landlord’s income)

- Interest accrues from the date the tax was deductible to the date of actual payment

- The Assessing Officer can raise a demand directly against the tenant

- The tenant’s own income tax assessment may be affected (scrutiny risk increases)

However, Section 201(1) provides a partial relief: if the tenant fails to deduct TDS but the landlord has included the rental income in their ITR and paid tax on it, the tenant is not treated as an assessee in default (though interest liability remains).

Common Mistakes and How to Avoid Them

Mistake 1: “My Rent Is Split Between Flatmates, So TDS Does Not Apply”

Incorrect. The TDS obligation is determined by the total rent for the property under the agreement, not by the per-person share. If the agreement specifies a monthly rent of Rs 80,000 and two flatmates each pay Rs 40,000, the total rent exceeds Rs 50,000 and TDS applies. The obligation falls on whoever is the lessee(s) under the agreement.

Mistake 2: Deducting TDS at the Old 5% Rate

Common after the October 2024 rate change. The rate for resident landlords is now 2%. Applying the old 5% rate results in over-deduction. While the landlord can claim a refund, it creates unnecessary cash flow impact and administrative work.

Mistake 3: Not Obtaining TAN for NRI Landlord

Critical error. Section 195 requires a TAN. You cannot file Form 27Q (the quarterly TDS return for NRI payments) without a TAN. Filing Form 26QC instead of 27Q for an NRI landlord is incorrect and may result in the TDS not being credited to the landlord’s account.

Mistake 4: Forgetting to Issue Form 16C

Common oversight. The TDS certificate is not just a formality; it is the landlord’s proof that tax has been withheld and deposited. Without Form 16C, the landlord may face difficulty claiming TDS credit in their ITR, which can lead to disputes with the tenant.

Mistake 5: Deducting TDS on the Security Deposit

Incorrect. Section 194-IB applies to “rent”: the periodic payment for the use of the property. The security deposit is not rent; it is a refundable advance. TDS should not be deducted on the security deposit amount.

Mistake 6: Not Deducting TDS Because the Landlord Objected

The landlord’s objection does not eliminate your legal obligation. Some landlords prefer to receive the full rent and claim they will pay tax directly. While the landlord’s objection is understandable (TDS affects their cash flow), your obligation under Section 194-IB is independent of the landlord’s preferences. Explain the legal requirement and provide Form 16C so they can claim the credit.

Mistake 7: Ignoring TDS When Paying Rent in Cash

TDS applies regardless of the mode of payment. Whether you pay rent by bank transfer, UPI, cheque, or cash, the TDS obligation remains if the monthly rent exceeds Rs 50,000. Note that cash payments exceeding Rs 2 lakh are separately restricted under Section 269ST.

HRA and TDS: The Interaction

Many salaried tenants who deduct TDS under Section 194-IB also claim House Rent Allowance (HRA) exemption under Section 10(13A). These are separate tax provisions with separate compliance requirements:

| Provision | Purpose | Requirement |

|---|---|---|

| Section 194-IB (TDS) | Tax withholding on rent paid to landlord | Deduct 2% TDS if rent > Rs 50,000/month |

| Section 10(13A) (HRA) | Exemption on HRA component of salary | Provide landlord’s PAN to employer if rent > Rs 1,00,000/year |

| Section 80GG | Deduction for rent paid (for non-HRA recipients) | Rent paid minus 10% of total income, subject to caps |

Important: Claiming HRA exemption does not substitute for TDS compliance, and vice versa. You must comply with both provisions independently. The PAN provided to your employer for HRA purposes should match the PAN used for Form 26QC filing.

Key Takeaways

- TDS at 2% is mandatory for individual/HUF tenants paying monthly rent exceeding Rs 50,000 to resident landlords (rate effective October 1, 2024, reduced from 5%).

- No TAN is required for Section 194-IB compliance; your PAN is sufficient. File Form 26QC on incometax.gov.in and issue Form 16C within 15 days.

- For NRI landlords, TDS at approximately 31.2% applies on any rent amount under Section 195. TAN is mandatory, and quarterly filing of Form 27Q is required.

- If the landlord does not furnish their PAN, deduct TDS at 20% under Section 206AA instead of the standard 2%.

- TDS applies only to rent, not to the security deposit. The obligation is determined by the total rent under the agreement, not individual shares in a shared tenancy.

- Non-compliance consequences include interest at 1-1.5% per month, late filing fees of Rs 200/day (capped at TDS amount), and potential “assessee in default” status.

- NRI landlords can reduce the TDS burden by obtaining a Lower Tax Deduction Certificate from the Assessing Officer under Section 197.

- Maintain monthly records of TDS deductions and keep copies of Form 26QC acknowledgments and Form 16C for at least 6 years (the period for which income tax records must be preserved).

References

- Income Tax Act, 1961, Section 194-IB (TDS on rent by individuals/HUFs). Inserted by Finance Act, 2017. Available at: incometaxindia.gov.in.

- Finance (No. 2) Act, 2024, Amendment reducing Section 194-IB TDS rate from 5% to 2% effective October 1, 2024. Ministry of Finance, Government of India.

- Income Tax Act, 1961, Section 195 (TDS on payments to non-residents). Governs TDS on rent to NRI landlords.

- Income Tax Act, 1961, Section 206AA (higher TDS rate when PAN not furnished). Mandates 20% TDS in the absence of PAN.

- Income Tax Act, 1961, Section 201 (consequences of failure to deduct or pay TDS). Defines “assessee in default” status and interest liability.

- Income Tax Act, 1961, Section 234E (fee for late filing of TDS statements). Rs 200 per day, capped at TDS amount.

- Income Tax Act, 1961, Section 272A(2)(g) (penalty for failure to issue TDS certificate). Rs 100 per day.

- Income Tax Act, 1961, Section 271C (penalty for failure to deduct TDS). Penalty up to the amount of TDS not deducted.

- Income Tax Act, 1961, Section 197 (certificate for lower deduction). Enables NRI landlords to obtain LTDC from Assessing Officer.

- CBDT Circular No. 5/2017 dated June 2, 2017, Guidelines on implementation of Section 194-IB. Central Board of Direct Taxes.

- Income Tax e-filing portal, incometax.gov.in. For Form 26QC filing.

- TRACES portal, tdscpc.gov.in. For Form 16C download and verification.